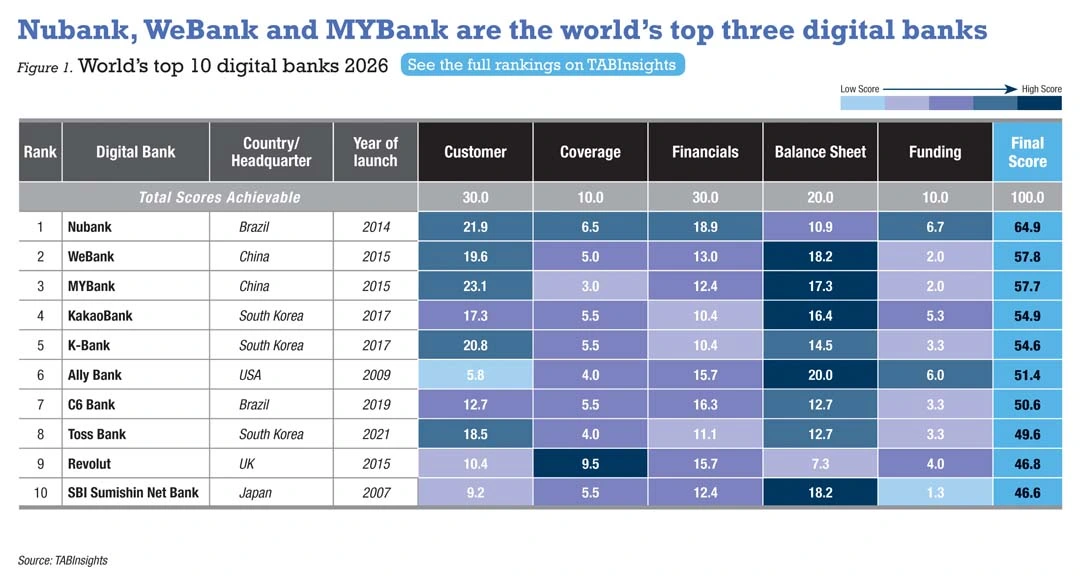

Nubank retains the top spot in the 2026 TABInsights World’s Top 100 Digital Banks Ranking, with diversified offerings, strong customer engagement and robust financial performance. China’s WeBank and MYBank rank second and third, while South Korea’s KakaoBank and K-Bank complete the top tier.

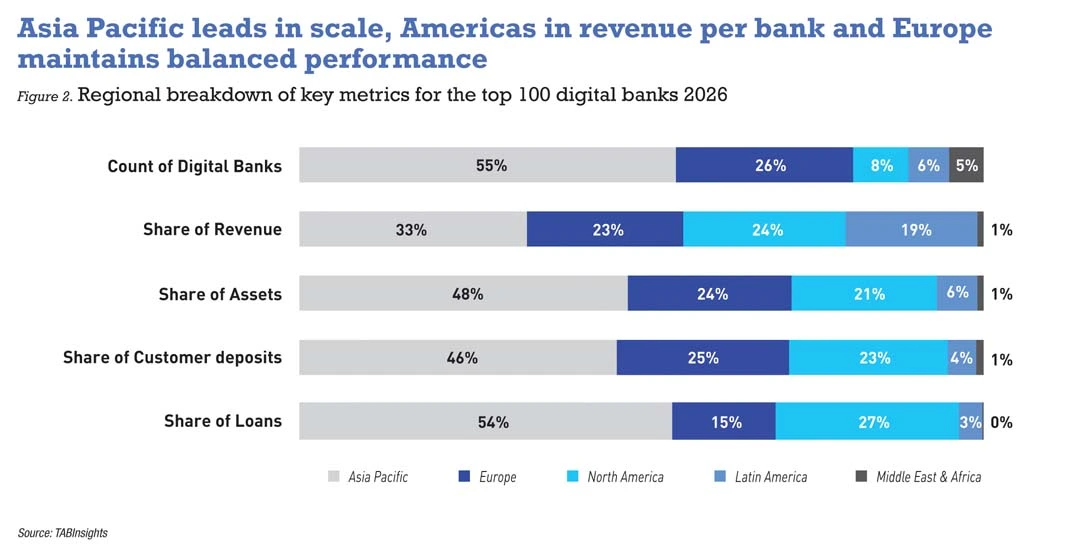

The 100 digital banks collectively held $1.4 trillion in assets, $1.1 trillion in deposits and $0.7 trillion in loans, generating approximately $60 billion in revenue by the financial year (FY) 2024. Among them, 55 are headquartered in Asia Pacific, 26 in Europe, eight in North America, six in Latin America and five in the Middle East and Africa.

Digital banks are entering a more structured phase after years of rapid expansion. While headline growth has moderated from early surges, profitability is improving, though returns remain uneven. Strategies are shifting toward greater monetisation of existing users, with stronger focus on retention, revenue-generating customers and broader product offerings across lending, wealth management and insurance. Disciplined balance-sheet management, revenue diversification and operational efficiency are becoming increasingly important to long-term competitiveness.

Top digital banks strengthen advantage through scale and profitability

Nubank retained its position as the leading digital bank, followed by WeBank, MYBank and KakaoBank. The top 10 banks reported asset sizes ranging from $13 billion to $181 billion for the FY2024 and all achieved full-year profitability, offering an average of 8.9 core products compared with 7.2 for the top 100. Six of them were also in the top 10 last year. Leading digital banks leverage scale, brand recognition, funding advantages and operational depth to reinforce their positions, widening the gap with mid-tier peers.

K Bank, C6 Bank, Revolut and SBI Sumishin Net Bank entered the top 10 with expanded operations, diversified revenue streams and improved profitability. ING was excluded under tightened criteria as ranking standards for digital banks were stricter, and T-Bank dropped out following integration with Rosbank.

Nubank has sustained rapid growth while deepening customer engagement. Its customer base grew from 94 million in FY2023 to 114 million in FY2024 and 131 million in FY2025, covering over 60% of Brazil’s adult population. The bank is pursuing international growth and diversifying its product portfolio. In FY2024, it expanded into higher-income segments and introduced secured lending, strengthening revenue potential and portfolio resilience. The acquisition of Hyperplane, a Silicon Valley data intelligence company, enhanced Nubank’s capabilities in data-driven personalisation, credit decisioning and operational efficiency.

Financially, Nubank maintained its growth trajectory while strengthening results. Pre-tax return on equity (ROE) rose from 27.2% in FY2023 to 39.8% in FY2024, supported by a low-cost operating model, with the monthly average cost to serve per active customer remaining at $0.8. Nubank maintained disciplined credit risk management by shifting credit cards toward lower-risk customers, increasing secured lending and improving risk profiling for unsecured loans. Despite non-performing loan ratios staying relatively high, risk-adjusted net interest margin held at a strong 9.5% in the fourth quarter of FY2024.

WeBank delivered solid performance in FY2024 despite a challenging external environment. Its retail customer base grew by 25?million to 424?million, while approximately 6?million micro, small, and medium enterprises (MSMEs) applied for loans. Corporate lending has surpassed consumer lending, driven by MSME growth. This strategic shift aims to optimise the portfolio, manage risk and rebalance profitability, affecting short-term earnings but enhancing long-term resilience. Combined with net interest margin compression and tighter regulation that reduced platform fee income, these factors led pre-tax ROE to decline from 30% to 23.5%, remaining at a robust level.

WeBank continued to reinforce its technological infrastructure and digital capabilities, supporting high-volume, low-cost operations, with peak daily transaction volumes exceeding 1.4 billion. Technology investments remained high and technology personnel comprised at least 50% of total staff, emphasising in-house expertise. The establishment of WeBank Technology Services in Hong Kong enables the bank to leverage its technological expertise for international finance solutions, supporting global expansion and innovation.

MYBank showed robust expansion in FY2024, with its MSME customer base increasing substantially to 68.5 million. In FY2024, the bank significantly expanded its transaction banking services, combining account services, wealth management and payment solutions to create a second growth engine alongside its core credit business. This broadened its revenue base and enhanced engagement with small businesses. Revenue increased 14%, with net interest income up 6% and net fee income rising 47%, leading the cost-to-income ratio (CIR) to edge down to 27.4%. Pre-tax ROE fell to 11.8% due to higher provisions for credit impairments.

KakaoBank reached 24.9 million customers by the end of FY2024, with 18.9 million monthly active users, maintaining high engagement despite slower growth in a market approaching saturation. Net profit rose 24% year-on-year to a record level, supported by stronger non-interest income. Fee and platform revenue accounted for roughly one-third of operating income, representing a more diversified, platform-based earnings structure. The bank expanded platform services and introduced new products, while pursuing international initiatives in Southeast Asia, including an equity investment in Indonesian digital bank Superbank and a joint venture with Thailand’s SCBX to launch a digital bank.

Structured growth replaces scale-driven growth

Following a period of rapid formation and scale-driven expansion, the sector is entering a more structurally disciplined phase characterised by quality-led growth. While headline growth rates have moderated from early-stage surges, expansion remains structurally robust. The top 100 digital banks saw approximately 13% growth in their customer base, with median growth in FY2024 reaching 21.6% for assets, 26.2% for deposits, 22.3% for loans and 24.8% for revenue.

The sector is shifting from acquisition-led scaling toward growth aligned with capital strength and risk management. Balance-sheet expansion aligns with funding stability, with deposits growing in line with user expansion and loan exposures rising on the balance sheet.

Digital banks are increasingly focusing on higher user retention and engagement, capturing a larger share of revenue-generating customers, and offering more diversified products. They are shifting toward generating more value from existing customers rather than purely expanding scale.

While average revenue per user has not yet shown broad growth in FY2024, it is expected to become an increasingly critical performance metric.

Regional divergence is becoming more pronounced. Latin America and parts of Southeast Asia continue to post elevated growth, supported by lower penetration and smaller starting bases, while North America and Europe exhibit slower expansion as market penetration deepens and competition intensifies, with growth increasingly dependent on monetisation rather than onboarding.

Leading digital banks command materially larger balance sheets and customer bases than mid- and lower-tier peers, underscoring the potential for further growth and differentiation within the sector.

Profitability is rising, but returns remain structurally uneven

Overall profitability improved across the sector. Among the 100 digital banks included in the 2026 ranking, 57 reported full-year profits in FY2023, rising to 62 in FY2024. Of the 62 profitable institutions, 47% were headquartered in Asia Pacific, 32% in Europe and 11% in North America. Several banks, including C6 Bank, Klarna Bank, Maya Bank, Tandem Bank and Toss Bank, reached break-even in FY2024, supported by stronger revenue generation and disciplined cost management.

Despite improvements in profitability, returns across the sector remain uneven. Leading institutions reported notably high ROE figures, for example Revolut at 52.7%, Nubank at 39.8%, SBI Sumishin Net Bank at 26% and WeBank at 23.5%. However, overall returns remain moderate. The median pre-tax ROE among the top 100 digital banks stood at just 6.9% in FY2024, and only 13 institutions exceeded 20%.

Net interest income remains the dominant revenue source as institutions expand on-balance-sheet lending and capture margins directly. While this improves revenue scale, it also increases capital requirements and risk-weighted asset intensity. Among the top 20 digital banks, non-interest income accounted for only 24% of total revenue on average. Strengthening fee-based income and broadening revenue streams remain key development priorities.

Competitive advantage is increasingly linked to revenue mix and efficiency

Revenue performance remains closely linked to user and asset growth, with scale continuing to underpin financial outcomes. However, banks are increasingly balancing new customer acquisition with efforts to generate greater value from existing users, while enhancing returns through diversified revenue streams and improved operational efficiency.

Digital banks are expanding their product offerings, with lending, wealth management, and insurance increasingly integrated to enhance customer retention and diversify revenue streams. Product breadth is gradually rising, with the top 100 banks offering an average of 7.2 core products, up from 6.8 in last year’s ranking.

Operational efficiency is a key driver of competitive advantage. The median CIR decreased from 57.6% in FY2022 to 53.1% in FY2024, with improved operating leverage. In FY2024, seven banks reported CIRs below 30%, with another 11 recording ratios between 30% and 40%. Personnel efficiency remains a structural advantage, as high user-per-employee ratios demonstrate the scalability of digital operating models and support stronger leverage.

Asia Pacific holds the largest structural presence

Across the top 100 digital banks, Asia Pacific leads both in number and market share, with 55 banks holding 48% of total assets, 46% of deposits, 54% of loans, and 33% of revenue. Revenue per bank is relatively low, with intense competition and modest profit margins. The region’s strong presence is supported by large, tech-savvy populations, favourable regulatory frameworks in major markets, and emerging Southeast Asian countries driving new user growth.

Europe features 26 digital banks and shows balanced performance across metrics, supported by mature customer financial literacy, stable adoption and robust regulatory frameworks. Product innovation targets niche segments, with success relying on operational efficiency and the ability to offer specialised services.

In North America, eight digital banks generate 24% of total revenue, 21% of assets, 23% of deposits and 27% of loans. In these mature and saturated markets, the emphasis is on optimisation rather than expansion, with strong competition from established banks, stringent regulatory oversight and advanced fintech adoption.

Latin America holds only 6% of total assets but contributes 19% of total revenue. Rapid smartphone penetration and supportive regulatory frameworks support digital banks’ expansion and financial inclusion.

The Middle East and Africa have limited representation among the top 100, with low shares of revenue, assets, deposits and loans. Expansion will depend on investment in customer education, product diversification, and scalable technology platforms.

China and South Korea anchor Asia Pacific market

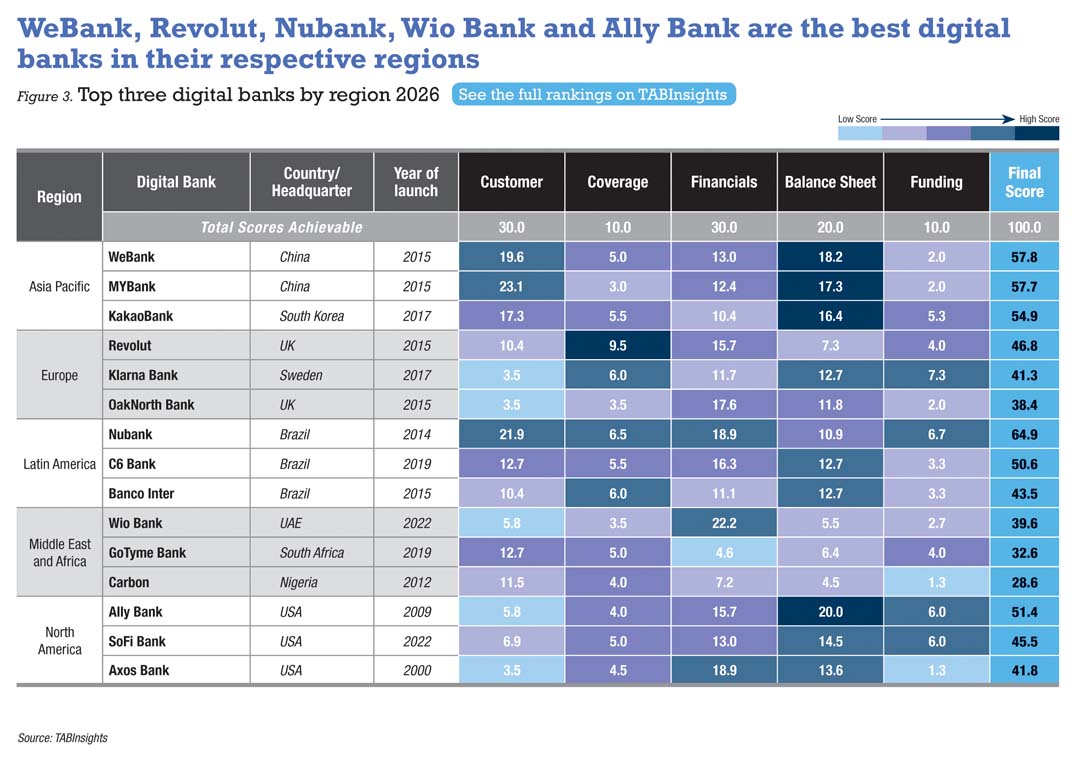

The top 10 banks in Asia Pacific remain stable from last year, with four from China, three from South Korea, two from Japan and one from Indonesia. WeBank ranks as the best bank in the region, followed by MYBank, KakaoBank, K-Bank and Toss Bank, reflecting the dominant positions of China and South Korea in the region’s digital banks sector. Top banks in each market include Judo Bank in Australia, WeLab Bank in Hong Kong, Airtel Payments Bank in India, SeaBank in Indonesia, SBI Sumishin Net Bank in Japan, Maya Bank in the Philippines, Trust Bank in Singapore, O-Bank in Taiwan and TNEX in Vietnam.

China’s digital banks remain highly concentrated, with WeBank and MYBank as the two largest institutions. As of FY2024, WeBank reported assets of $89 billion and MYBank $65 billion, far exceeding peers in the ranking. Other banks range from $6 billion to $19 billion, including XW Bank, aiBank, Z-Bank, Su Merchants Bank, Yillion Bank and KCB Bank. This scale gap results from the benefits of large technology ecosystems, broader customer reach and greater access to funding.

Profitability and efficiency metrics varied significantly. WeBank delivered the highest pre-tax ROE at 23.5%, followed by Z-Bank at 12.8%, XW Bank at 12.2%, MYBank at 11.8% and aiBank at 10.2%. Differences were closely linked to loan pricing power, funding costs, portfolio composition between consumer and small and medium enterprise (SME) lending, and disciplined risk management in credit underwriting and provisioning. Cost efficiency was strongest at XW Bank with a CIR of 21%, compared with 25% for KCB Bank and 27% for MYBank. Ecosystem strength, tight cost control and disciplined risk management remain central to sustaining returns across China’s digital banks.

South Korea’s KakaoBank, K-Bank, and Toss Bank delivered strong performances in FY2024, illustrating the maturity and competitive depth of the country’s digital banks. KakaoBank remains the largest digital bank, with the widest customer base and the highest revenue and ROE among the three. K-Bank achieved rapid customer growth along with a significant improvement in profitability. Toss Bank reported its first annual profit in FY2024, marking its move into sustained profitability.

K-Bank grew its customer base from 9.5 million in FY2023 to 12.7 million in FY2024, supported by partnerships within the digital asset and fintech ecosystem, while its pre-tax ROE rose from 0.8% to 6.9%, driven by robust revenue growth and lower loan loss provisions, although still lower than 9.3% for KakaoBank. Toss Bank expanded its customers from 8.9 million to 11.8 million and achieved a significant milestone by reporting its first annual profit in FY2024, with pre-tax ROE improving from -1.7% to 2.8%, marking a successful turnaround and growth trajectory.

WeLab Bank became Hong Kong’s leading digital bank, growing through innovative products and cross-industry collaborations. The bank reached its first breakeven in December 2024, with a CIR of 86%. In 2024, the online lending platform WeLend became its wholly-owned subsidiary, creating synergy in customer acquisition, risk management and funding.

Maya Bank rose to become the top digital bank in the Philippines, achieving full-year profitability in FY2024 just two and a half years after launch. Its ecosystem-led model drove strong customer engagement, growing the customer base from 3.1 million to 5.4 million and raising the loan-to-deposit ratio (LDR) from 13% to 44%. Revenue tripled, CIR improved to 49%, and pre-tax ROE reached 12.5%.

Trust Bank became Singapore’s top digital bank, expanding its customer base to over one million, with more than 70% acquired via referrals. Deposits and loans rose sharply, while revenue increased 148% without a proportional rise in operating costs.

Revolut, Klarna and OakNorth lead a diversified European market

The top 10 digital banks in Europe include two from the UK, two from France, two from the Netherlands, and one each from Germany, Norway, Spain and Sweden. Revolut ranks as the leading digital bank in Europe, followed by Klarna Bank and OakNorth Bank. Revolut excels in customer scale and market coverage, Klarna Bank shows strong balance sheet metrics and OakNorth Bank demonstrates operational efficiency.

In FY2024, Revolut’s global user base reached 52.5 million, a 38% year-on-year increase, with the number of customers using it as their main bank growing 59%. Product offerings expanded in FY2024, including instant access savings in seven new countries, Flexible Cash Funds in over 30 countries, alongside loans, credit cards, and buy now, pay later services across 11 countries. Digital mortgage products were launched in Lithuania, with further rollouts planned in additional European markets in 2026.

This growth and product diversification supported its solid financial performance. In FY2024, its pre-tax profit increased 149%, supported by disciplined cost management and revenue growth across multiple business lines. Total assets reached $32 billion, with 62% held as cash and equivalents, resulting in a LDR of only 4%. Customer loans rose 86% year-on-year, primarily unsecured personal loans.

Klarna Bank achieved profitability in FY2024 for the first time in several years, achieving a pre-tax ROE of 1.5%. The bank enhanced efficiency through cost management and targeted AI investments, reducing its CIR from 96% in FY2023 to 78% in FY2024.

OakNorth Bank specialises in lending to lower mid-market businesses, delivering strong performance through rigorous credit underwriting, a focused strategy and disciplined operations. The bank began operations in the US in mid-FY2023 and had provided $685 million in loans to fast-growing entrepreneurial businesses by the end of FY2024. Its pre-tax profits increased by 15% year-on-year, with a pre-tax ROE of 22.6%. Its CIR rose slightly from 28% in 2023 to 31% in 2024, while remaining the lowest among digital banks in the region.

Ally Bank, SoFi Bank and Axos Bank lead North America

Ally Bank remains the top digital bank in North America, followed by SoFi Bank and Axos Bank. Ally Bank leads in balance sheet scale and revenue, although profitability faced pressure from portfolio repositioning. SoFi Bank grew faster, while Axos Bank achieved the highest profitability metrics among peers.

In FY2024, Ally Bank reported a 3% decline in revenue and a 10% drop in pre-tax profit. The weaker revenue base reduced operating leverage, and higher credit loss provisions further weighed on earnings. Its pre-tax ROE declined from 26.2% in FY2022 to 15.6% in FY2023, and further to 13.8% in FY2024. To sharpen its strategic focus, Ally streamlined operations, divesting its credit card business and ceasing new mortgage originations.

SoFi Bank expanded membership and strengthened its balance sheet, with deposits growing 38% to $26 billion in FY2024. Revenue reached $2.2 billion, higher than Axos Bank at $1.1 billion but still well below Ally Bank at $8.6 billion. Axos Bank improved profitability, with a CIR easing from 43% to 42%, compared with 53% for Ally Bank and 69% for SoFi Bank. Its pre-tax ROE increased to 30.3%, up from 29.6% the previous year, higher than SoFi Bank at 16.3% and Ally Bank at 13.8%.

Nubank dominates Latin America

The top three digital banks in Latin America are all based in Brazil. Nubank continues to lead in scale and performance, with a customer base of 114.2 million at the end of FY2024. C6 Bank surpasses Banco Inter to rank second, with 35 million customers, while Banco Inter held 36.1 million. C6 Bank’s rapid profitability turnaround and focus on secured lending contrast with Banco Inter’s ecosystem-driven model and diversified income base. This illustrates two distinct strategies in Brazil’s competitive digital banks market. Both banks improved profitability in FY2024, but C6 Bank reported a lower CIR and higher ROE than Banco Inter.

In FY2024, C6 Bank delivered its first full-year profit since its founding in FY2019, marking a clear shift from expansion to sustained profitability. This turnaround was driven by broader adoption of its products and services, stronger monetisation of its client base and improved cost discipline. It was further supported by JPMorgan’s increased stake and a strategic focus on secured lending and diversified revenue streams. Its loan portfolio expanded 32% year on year, with secured lending accounting for more than three quarters of total loans, improving asset quality. Payroll-deductible and vehicle loans led growth. Revenue tripled due to business expansion and cross-selling, while operating expenses declined slightly.

Banco Inter’s dynamic growth and accelerated launch of new products continue to attract users, with the activity ratio rising to 57% and international accounts expanding to 3.9 million. The bank has diversified revenue sources, with approximately 41% from securities transactions, 29% from net interest income and 25% from fees and commissions, providing flexibility to respond to macroeconomic changes. Its loan portfolio was well-diversified, with credit cards making up about 33% of the portfolio, mortgages accounting for 32%, personal loans representing 23% and small business loans accounting for 11%.

Wio Bank and GoTyme Bank lead early-stage expansion in Middle East and Africa

In the Middle East, Wio Bank, launched in September 2022, remains the leading digital bank. In FY2024, it grew its retail and SME customer base to over 140,000 and 90,000, respectively. Revenue tripled, supported by a revenue mix of 55% net interest income and 45% non-interest income. The bank reported a CIR of 44% and a pre-tax ROE of 21.6%, up from just 0.1% in FY2023. Its cloud-native model, targeted customer acquisition and diverse revenue streams, supported by a favourable regulatory environment, contributed to its early profitability.

In Africa, GoTyme Bank, formerly TymeBank, remains the leading digital bank, followed by Nigeria’s Carbon and South Africa’s Discovery Bank. GoTyme Bank leads in customer scale and rapid progress toward profitability while Discovery Bank focuses on higher customer value and a diversified revenue base, demonstrating two distinct models shaped by target segments and monetisation strategies.

GoTyme Bank focuses on scale and low-cost mass-market strategies. It grew its customer base by 30% year-on-year to 9.6 million in FY2024 and to approximately 12 million by late 2025. Growth was supported by simplified onboarding, retail partnerships and expansion in deposits and small-ticket lending. These factors contributed to strong balance-sheet growth and improved operating leverage. Revenue per user remained modest at around $9 in FY2024 and sustaining profitability will depend on increasing customer engagement, deeper product usage and prudent credit expansion.

Discovery Bank targets higher-income clients within the Discovery ecosystem, with its customer base reaching about one million by FY2024. Deposits and loans grew steadily while asset quality remained stable under a conservative lending strategy. Revenue growth was strong, driven by fee income and ecosystem-linked services, with revenue per user higher at $12 in FY2024. Ongoing investment in technology and customer acquisition has delayed full profitability.

The 2026 World’s Top 100 Digital Banks Ranking indicates a sector of digital banks moving from rapid expansion toward structured, quality-led growth. Markets vary in maturity and dynamics. Customer engagement, product breadth and profitability are increasingly important for competitive advantage. Leading digital banks combine scale, diversified revenue streams, operational efficiency and disciplined balance-sheet management to strengthen long-term resilience.

View the full World’s Best Digital Banks Ranking here

Download the full Databook of the World's Top 100 Digital Banks.

.png)

.webp)