Overall, the banking sector registered stronger growth in small business lending in the last two years. Governments have implemented various policies to encourage more credit supply for small businesses that play a pivotal role in economic growth and employment creation. The weighted average of growth in banks’ small business lending in the eight Asia Pacific markets, namely Australia, China, India, Indonesia, Malaysia, South Korea, Taiwan, and Thailand, stood at 15.4% in 2021.

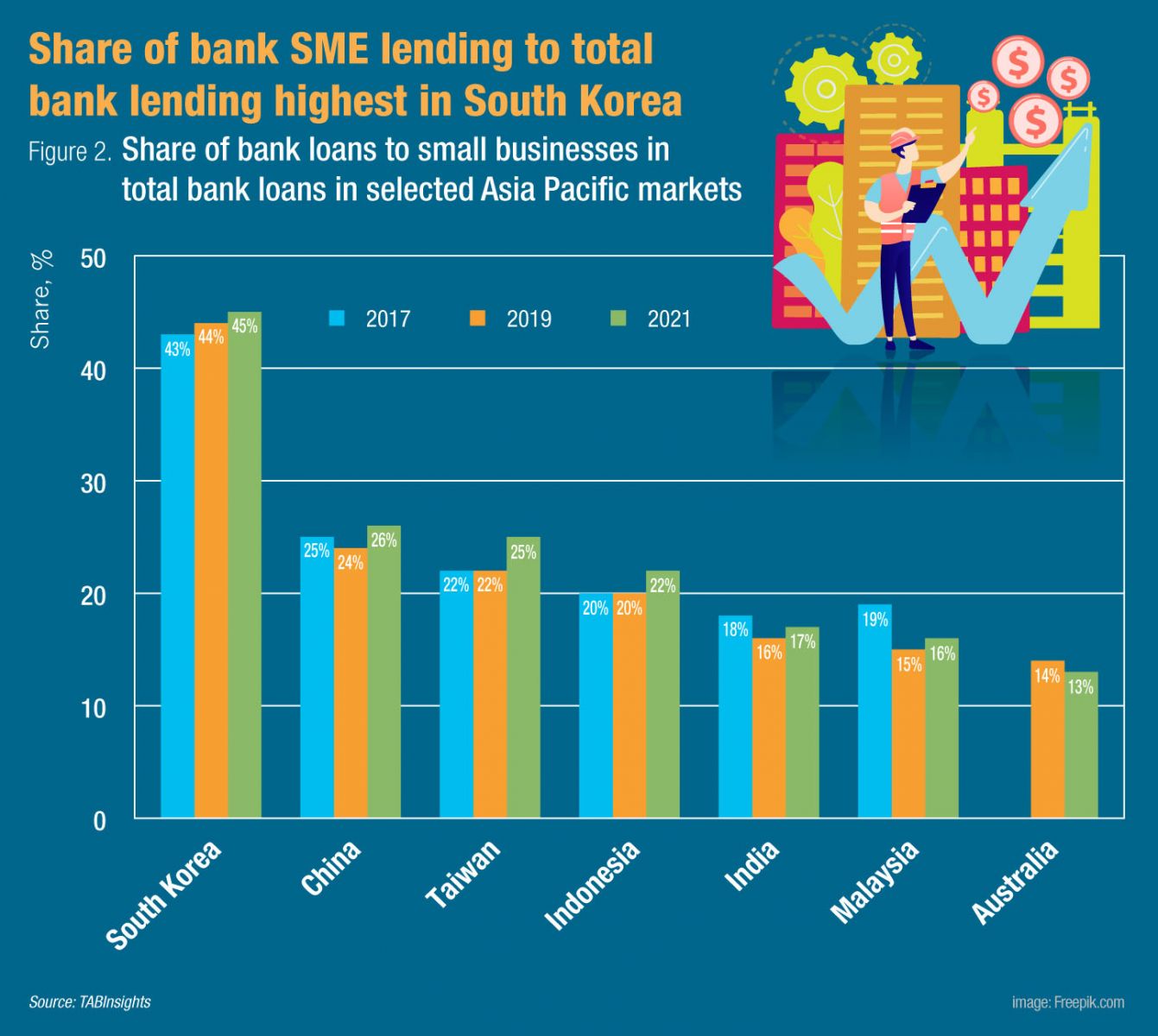

Among these markets, China posted the strongest growth in bank loans to small businesses between 2017 and 2021, at a compound annual growth rate (CAGR) of 12.9%, followed by Taiwan at 9.3%, and South Korea at 8.9%. The share of lending to small businesses to total bank lending increased in China, Indonesia, South Korea and Taiwan, while Australia, India and Malaysia saw a drop in the share of small business loans.

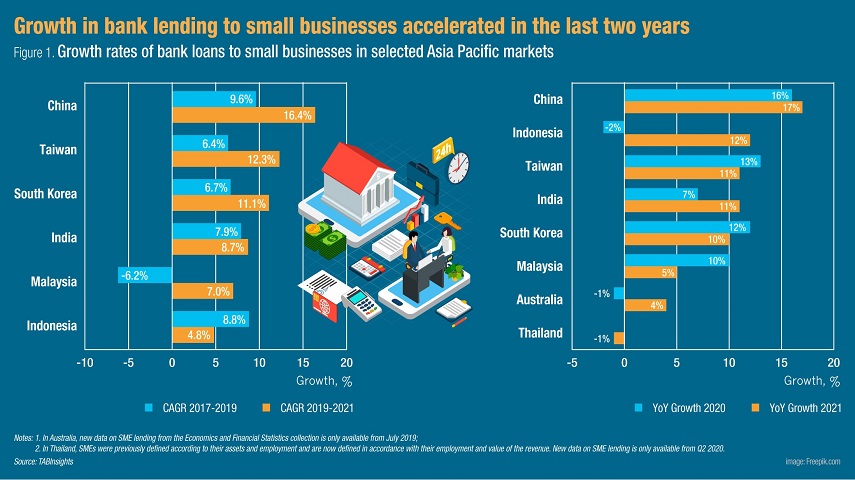

China recorded the strongest growth in bank lending to small businesses

China, Taiwan and South Korea witnessed double-digit annual growth in bank lending to small businesses over the past two years. China registered a CAGR of 16.4% in banking institutions’ lending to micro and small enterprises (MSEs) during the period from 2019 to 2021, stronger than the 9.6% recorded between 2017 and 2019. Banks’ MSE loans as a share of total bank loans went up to 24.5% in 2020 and 25.7% in 2021, following the decline from 25.2% in 2017 to 23.9% in 2019. Loans to small and medium enterprises (SMEs) in Taiwan increased by a CAGR of 6.4% from 2017 to 2019 and 12.3% from 2019 to 2021, reaching $316 billion at the end of 2021. The share of banks’ SME loans in total bank loans in Taiwan increased gradually from 21.6% in 2017 to 24.9% in 2021.

The outstanding MSE lending across the Chinese banking sector totalled $7.8 trillion in 2021. Inclusive MSE loans with a single bank’s credit line to the qualified borrower not exceeding $1.6 million (RMB10 million) accounted for 38% of the total MSE lending in 2021, rising from 32% in 2019. China’s push for greater financial inclusion has led to the 31% and 25% surge in inclusive MSE loans in 2020 and 2021, respectively. Large state-owned banks in China have all achieved the inclusive MSE loan growth target set by the government, with the annual growth rates above 30%.

It’s expected that small business loans in China will maintain the current growth momentum. The loan support policies for MSEs have been extended until June 2023, and the People’s Bank of China will provide funds to local banking institutions equivalent to 1% of the increase in their inclusive MSE loan balance from the start of 2022 to June 2023. In addition, the $63 billion (RMB 400 billion) relending quota for inclusive MSE loans can be given on a rolling basis and the quota can also be increased when necessary.

South Korea had a much higher share of small business loans

Outstanding SME loans in South Korea rose from $612 billion in 2017 to $772 billion in 2021. During the same period, the share of bank SME loans to total bank loans in South Korea experienced a gradual increase from 43.5% to 45%, more than double the share of bank lending to small businesses in markets such as Australia, India, Indonesia, Malaysia and Thailand.

The establishment of Industrial Bank of Korea (IBK) by the South Korean government in 1961 has improved the access to credit for SMEs in the country. In 2021, SME loans made up 80.5% of IBK’s total loans, compared to 78.5% in 2017 and 76.6% in 2013. It held the largest market share of SME lending in South Korea, at 22% in 2021, followed by Kookmin Bank (13.5%), Shinhan Bank (12.7%), KEB Hana Bank (11.6%) and Woori Bank (11.2%). The market share of Kookmin Bank fell from 13.8% in 2019 to 13.5% in 2021, while the other four banks all gained market share. In addition, the new rules on loan to deposit ratio implemented by South Korea’s Financial Services Commission have encouraged banks to cut consumer loans and lend more to businesses instead.

Similarly, the Taiwan government set up Taiwan Business Bank to provide financing assistance and guidance to SMEs. The bank had the third-largest market share in SME loans, at 8.1% at the end of 2021, while First Commercial Bank and Taiwan Cooperative Bank are the top two players, with the larger market share of 9.9% and 9.4%, respectively.

Indonesia experienced weaker small business loan growth

Indonesia posted a CAGR of 4.8% in bank lending to micro, small and medium enterprises (MSMEs) between 2019 and 2021, compared to 8.8% during the period from 2017 to 2019. Despite the government support for MSMEs through the national economic recovery programme, banks’ MSME lending contracted by 1.8% in 2020, from $84.3 billion in 2019 to $81.6 billion in 2020. However, the share of banks’ MSME lending to total bank lending was up slightly from 20.2% in 2019 to 20.3% in 2020, as total bank lending also dropped. Loan demand weakened amid the uncertainty and banks were also more conservative with their lending due to asset quality concerns. Gross non-performing loan (NPL) ratio of bank loans to non-financial institutions and to individuals were 1.75% and 1.18% in 2021, respectively, while gross NPL ratio of MSME lending was much higher at 9.29%.

Bank MSME loans in Indonesia experienced strong growth of 12% in 2021, and thus the share of banks’ MSME lending rose to 21.6% in 2021. The new regulation Bank Indonesia issued in August 2021 have boosted banks’ exposure to small businesses. Banks are required to allocate at least 20% of their loans to MSMEs by June 2022, and the mandatory ratio will be raised gradually to 25% by June 2023 and 30% by June 2024. Apart from direct lending to MSMEs, banks are allowed to meet the requirements by buying government bonds or asset-backed securities issued for inclusive financing or channelling loans via other banks or non-bank financial firms.

Despite the measure taken to support small businesses, the proportion of small business loans shrank in Australia, India and Malaysia. In Australia, SME loans fell by 1.2% in 2020 and grew by only 3.5% in 2021, partially due to sluggish loan demand from SMEs. The share of SME loans to total bank loans in Malaysia was lower from 19% in 2017 to 15% in 2019, as banks’ SME loans fell by 6.2% annually. In the last two years, banks’ SME loans in Malaysia grew at a CAGR of 7%, and therefore the share went up to 15.9%. Similarly, the share of MSME lending dropped from 18.1% in 2017 to 15.8% in 2018 in India, and the share increased to 16.8% in 2021, which is still less than that in 2017.

.png)

.webp)