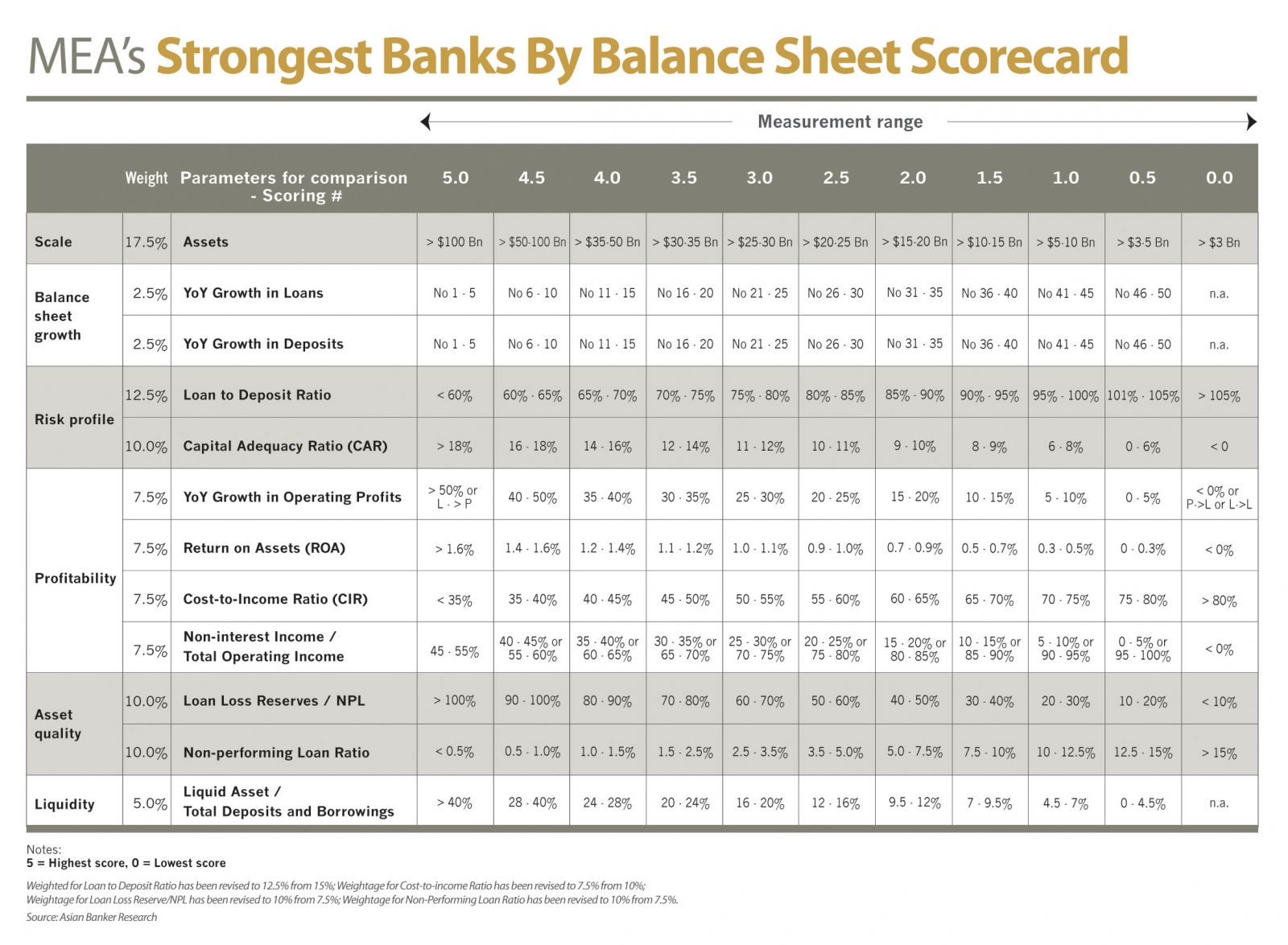

The Middle East and Africa 100 2015 (MEA 100) is an evaluation of the 50 largest banks in the Middle East and the 50 largest banks in Africa for the financial year 2014. While the countries covered are the same as last year, the annual strongest banks ranking is split into two separate lists this year, one focusing on banks in the Middle East, and the other on banks in Africa.

In the largest banks list, half of the top 10 banks were from South Africa, which was unchanged from last year’s evaluation. South Africa-based Standard Bank Group remains the largest bank by assets. Barclays Africa Group was squeezed out of the top five by National Bank of Abu Dhabi, which has replaced Emirates NBD as the largest bank by assets in UAE. With the growth rate of 15.7%, the assets of National Bank of Abu Dhabi stood at $102 billion in 2014.

South Africa recorded the highest market share of banks’ combined assets (20%), followed by UAE (19%) and Saudi Arabia (17%). In terms of net profits, however, South Africa’s share was only 15.2% as compared to 21.9% for UAE and 21.3% for Saudi Arabia.

Middle East banks generally well capitalised

When it comes to the annual ranking of strongest banks, Banque Saudi Fransi in Saudi Arabia held the top position. The top 10 positions were dominated by banks in Saudi Arabia and UAE. On an asset-weighted basis, banks from Saudi Arabia had the highest average strength score at 3.88 out of 5, while UAE was placed second with the average score of 3.54, followed by Jordan (3.41), Qatar (3.34), Kuwait (3.25), Bahrain (3.16), Lebanon (3.06) and Oman (2.97).

Based on the financial results of these 50 banks in the Middle East, banks are well-capitalised, with the weighted-average capital adequacy ratio at 16.8% in 2014.

Overall, the banking industry maintained double-digit operating profit growth in 2014 at 18%. Banks in Saudi Arabia had the highest average return on assets in the region, at 2.1%, while the return on assets in Lebanon was the lowest (1%). Qatar recorded the average cost-to-income ratio of 28.6% as compared to 50.5% in Lebanon.

African banks see profit growth from expansion within the continent

Commercial International Bank in Egypt is the strongest among the 50 African banks on our list. The average strength score of banks in Egypt was 3.26 out of 5, which was the highest among the four nations covered, while Kenya had the lowest average strength score at 2.53.

Despite general weak economic growth in South Africa in 2014, banks managed to report a 14.9% growth in operating profit and a 12.9% growth in net profit, partly due to expansion into the rest of Africa. Africa has seen the rise of pan-African banks, which originate mainly from South Africa, Nigeria and Kenya and are expanding across the region. The rapid expansion of these pan-African banks has helped financial services development and economic integration in the region. However, the potential risks stemming from the increasing pan-African business also underscore the need for stronger supervision.

Banks in Africa continue to report strong balance sheet growth, with the exception of South Africa, which recorded single-digit growth in both loans and deposits in 2014. The weighted-average loan growth in Kenya and Nigeria was 21.5% and 27.7% respectively in 2014. Egypt reported a lower loan growth at 12.9%, but its average deposits growth was stronger than that of Kenya and Nigeria.

Conclusion

The financial performance of the banking sectors in the Middle East and Africa continues to be variable. Growth in Middle East banking sector is expected to moderate in the next two years if oil prices remain low. Although the banking sector as a whole is unlikely to be affected greatly in the near future, some countries show greater vulnerability.

.png)

.webp)