Fintechs have become a catalyst for innovation in the financial services industry. Their entry resulted in a rapid change in the operating models of financial institutions forcing them to adopt emerging technologies with speed. These companies targeted the inefficiencies in the financial service sector from the start, bringing in new services and experiences to customers but they lack the market reach that banks have the advantage of. As new fintech innovations promise to change and improve the customer experience, institutions seek solutions that best meet their business objective while optimising their resource requirements and time to market. The strategic approach has changed rapidly, earlier considered as competitors and disrupters, fintechs are now increasingly considered as enablers and partners by banks.

Fintech strategy of banks

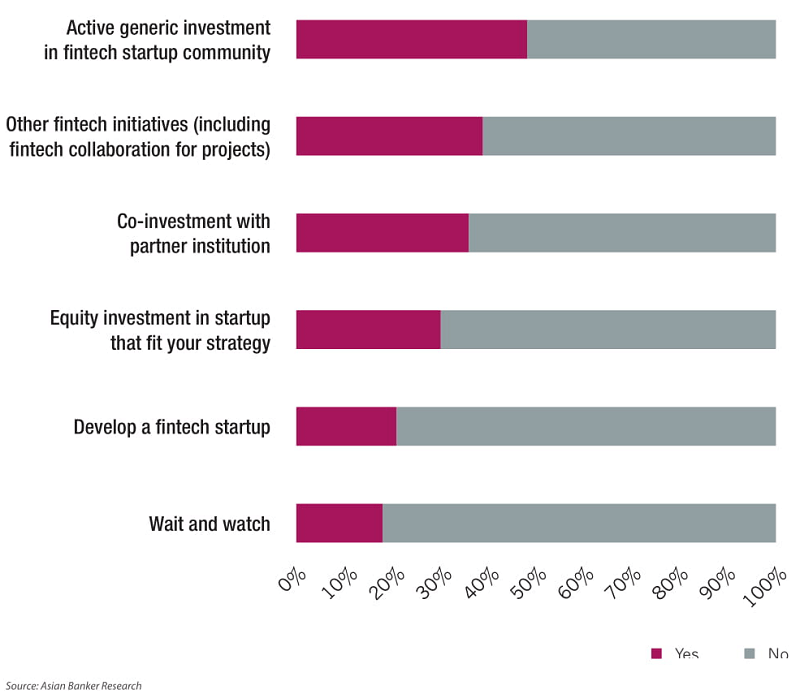

A survey conducted by The Asian Banker across 33 financial institutions in Asia Pacific and Middle East showed that a significant high 82% of banks surveyed have a strategic fintech approach in place while only 18% of banks said that they are in a ‘wait and watch’ mode. The fintech strategies vary among institutions. A significant 48% of surveyed banks said that they are making active generic investments in fintech towards developing the community, these include initiatives like setting up innovation labs, co-creating space, conducting hackathons among others. 30% of the companies surveyed have made active equity investment in start-ups that fit their strategy while 36% said that they are making active co-investment with partner institutions. A smaller 21% of banks said that they are developing a fintech start-up. A significant 39% of institutions said that they are taking other fintech initiatives, including collaboration with fintechs for specific technologies.

The strategic approaches to fintech and innovation vary

Banks continually evaluate evolving technology trends to assess the change they need to bring within their institutions and their service capabilities. Fintechs bring new challenges and opportunities and the diversity among fintechs with different business models makes the next few years difficult for incumbent players.

The competition is not only from fintechs but also from the “big tech” giants making foray into financial sector. “Each one of these competitors has their own strengths, fintech have better customer experience, use lean IT with faster solutions and diversity of ideas that cannot be replicated in an innovation lab in a bank. Banks have existing set of customers, the trust of the customers, know how to navigate regulation. The combination of banks and fintech will produce a convergent institution that will be better equipped to compete with pure technology platforms like Amazon, Alibaba, Google etc,” remarked Justo Ortiz, Chairman, UnionBank of Philippines.

UnionBank formed a fintech business group a couple of years back which is driving the bank towards its digital vision while building its culture. Talking about the transformation in the bank, Ortiz pointed out: “This is a huge mindset and cultural change operating in a vertical, combined and control organisation and is beginning to evolve into a horizontal collaborative organisation both inside and outside.”

There is notable change in the way banks now perceive and embrace fintech. The need to provide faster and innovative solutions with speed is driving them towards fintech. Rather than develop solutions in-house from scratch, banks now look to build a fintech ecosystem that facilitates them to meet their objectives faster.

“Earlier we used to consider fintech as disrupters of the financial industry but now in recent years they are considered as opportunities. Either banks now buy them out or partner with them,” said Zuzar Tinwalla, chief information officer, Standard Chartered Bank India.

The approaches vary. Several leading banks across the globe are actively investing in fintech either through venture capital funds or directly into the equities of selected fintech companies. Some banks have taken measures as accelerator programmes and incubators towards investing in development of promising fintech companies and building industry engagement. Many other banks seek to identify the right fintech with emerging technology innovations as partner for specific projects according to their operational and business requirements. The ecosystem is evolving as industry witnesses increased collaboration leveraging API technologies as they open their systems to facilitate faster integration with new solutions.

The approaches of banks are often multidimensional and incorporate more than one strategic approach.

UnionBank for instance has two transition strategies driving this change. “Transformation ‘A’ is focusing on the existing bank and taking it towards a relevant digital bank, defined by our sustainability goal of going paperless, with customer experience that have been spoilt by the technology companies. Transformation ‘B’, run by a different set of people and capitalised separately, is doing emerging technologies, building on the transformation blueprint,” explained Ortiz

The bank is putting its bet on blockchain. UnionBank is spearheading a challenging “island-to-island” (i2i) project in Philippines which focuses on financial inclusion prosperity using blockchain as the interconnecting ecosystem by linking rural banks with major financial networks through collaborative approach so that they can become more relevant to their customers. Ortiz shared that it currently has a pilot with 6 banks and over 80 other banks are interested to join. Besides this, the bank is also exploring use of blockchain for non-mission critical systems within the bank such as manuals and circulars, loyalty programmes on credit cards etc.

82% of financial institutions surveyed now have a strategic approach to engage with fintechs but their investment strategies vary

Figure 1. Survey results on fintech strategies of banks

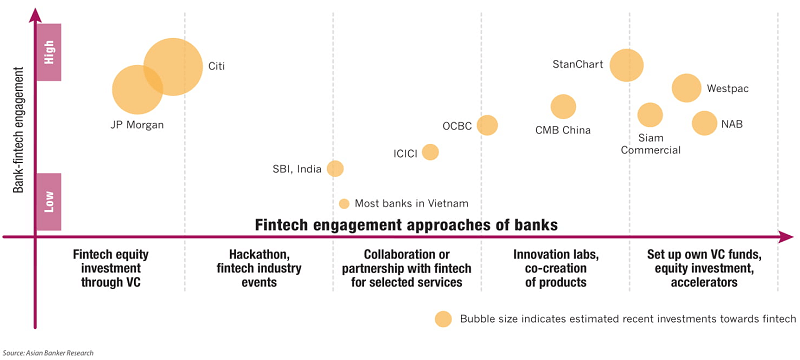

Banks are increasingly collaborating with fintechs but with different strategies and varying investment outlay

Figure 2. Bank fintech engagement strategies

“One thing is clear that status quo is decaying and it is just matter of time. That’s why the idea of collaborative common and how that as an epigenetic marker in our DNA is how we prefer to deal with people - peer to peer, face to face,” he opined.

The bank is exploring a combination of emerging technologies while enabling its people to adapt to these, driving the change through minimum value propositions and process of iterating and moving into co-creative process with different stakeholders. “We have around 400 new ideas that are local solutions to local problems, relevant that basically address the holy grail of how to make customers happy using emerging technologies for example AI. These ideas came through crowd sourcing,” commented Ortiz.

StanChart also has two pronged strategy planned.

“Firstly we have partnered with fintechs to provide banking solutions to our clients, for example, we have partnered with Ripple for blockchain, another partner is Mosaik in India. Secondly, we have set up SC venture in Bengaluru for investing in fintech, it is a separate subsidiary which will only work on innovation, futuristic trends that are impacting the banking industry and set up solution that not only our bank but other FIs can also leverage upon,” said Tinwalla.

StanChart has also launched an eXellerator lab in Singapore and London and also plans to build these in Dubai and Africa. These labs provide a platform to co-create solutions with clients, build stronger engagement with the local fintech community and drive innovation across the bank.

“The combination of banks and fintech will produce a convergent institution that will be better equipped to compete with pure technology platforms like Amazon, Alibaba, Google”

Several banks are actively seeking project specific fintech partners where they find an operational and technology fit for a business requirement. Through API frameworks they can facilitate faster integration with fintech solutions and are also building sandbox which can facilitate pilot testing on new technologies. DBS for instance launched API platform with 150 open API and 50 live partners.

As regulations like Revised Payment Service Directive (PSD2) emerge, banks across Europe are now required to open their data, providing greater level playing field to fintechs. Through increased data access and APIs, banks and fintech together can build new services to improve customer experience however banks will need to manage the data security and privacy issues.

Some banks across the Asia Pacific region have also set up innovation centres, many of which focus on engaging, identifying and promoting new technologies. Among the progressive banks the focus is increasingly now on building innovation culture, not just top down but across all level of employees, agility in processes and ability to think and act like fintech. One of the key focuses of innovation labs is often also to develop the institution’s ability to enhance staff skill set, to train employees to bring agility in processes and to apprise them of developments in ongoing digital transformation.

OCBC Bank for instance focuses on fintech companies that can meet the bank’s unique business need. It has set up ‘The Open Vault’ (TOV) innovation centre that collates various problem statements from across the operations of the bank and hunts for the best fintech companies to run experiments with. The experiments are accelerated over a 12 week period and tested through its data sandbox and solutions were then commercialised and implemented. Earlier this year it also developed a lab focused of developments in artificial intelligence.

Fernn Lim, head of culture and fintech acceleration at TOV, OCBC shared that unlike traditional accelerators, OCBC does not take any equity in the start-ups, rather its unique value proposition is its commitment to commercialise with them.

Commonwealth Bank of Australia has labs in Sydney and London. Its focus has been on facilitating new innovations and technology partnerships at its innovation labs either for the bank’s customers directly or for customers of its business clients. It implemented over 70 projects including many co-creation activities with universities, technology companies and corporates to address customer challenges. It organised several hackathons in areas on quantum computing, blockchain etc and industry events, including cities of the future and the future of transport and think-tank events.

Among other examples, DBS Asia X (DAX) provides co-working space for 100 people and also provides workshops, talks and learning resources to promote innovation. China Merchants Bank also developed fintech innovation incubator platform that is providing incubator support and develops new fintechs through sandbox approach.

Rising investments in fintech

“Firstly, we have partnered with fintechs to provide banking solutions to our clients. Secondly, we have set up SC venture in Bengaluru for investing in fintechs”

Noting the potential growth opportunities, several banks have increased their investments in fintech, which may be structured or unstructured. Banks aim to gain from early access to the technology and a first mover advantage. However there remains uncertainty with regards to returns on the capital investments made.

Some banks have set up venture funds to take equity positions, for instance Siam Commercial Bank has set up fintech investment arm Digital Venture with $100 million capital, one of the largest in Thailand.

Westpac reportedly set up ‘Reinventure’ fund which has already made 20 investments in companies from two funds. It recently committed another $50 million taking the total commitment to $150 million to the fund that target to explore opportunities in the fast-growing Asian fintech market and blockchain technology.

On the other hand, UOB in Singapore established a joint venture with SGInnovate to set up ‘Finlab’ which provides mentorship to a wide spectrum of startups. It has run two acceleration cycles in the past and the third cycle is this year. UOB along with Temasek has also set up InnoVen Capital, debt financing venture through which it provides debt funding to start-ups in China, India and South East Asia.

The investment in fintechs by leading banks in the industry is growing rapidly for strategic gains and in expectations of higher returns in future. According to CB Insights, top 11 US banks by assets participated in a total of 49 equity rounds to fintech start-ups in 2018 till now. This compares to 19 in 2017 and 33 in 2016. Overall globally greater investments are flowing into the fintech sector. The venture capital backed global fintech deals in the first three quarters of 2018 is estimated to be $32.6 billion by CB Insights, this has already surpassed the $17.9 billion raised in 2017 and $19 billion in 2016.

Outlook

With their ability to improve services, costs, efficiencies and rapid time to market, fintech have increasingly become more relevant to banks. The focus increases as institutions aim to enable their customer services with emerging technologies like artificial intelligence, machine learning and blockchain. For fintech companies these partnerships will enable greater funding, market reach and scale leading to a win-win situation. The bank collaborations with fintech ecosystem will need to further escalate if they have to compete effectively against technology giants that are making foray into financial sector and to provide the relevant and personalised customer experience.

Successful engagement with fintech requires banks to also redesign their own internal processes from the traditional long procurement processes to fast track embedding of new solutions with speed. In addition, they will also need to bring a change in their traditional culture towards embracing greater innovation and customer centricity and ability to think more like technology companies.

.png)

.webp)