Financial regulators in many Asia Pacific countries have already begun their digital banking – also known as neo, virtual, and challenger banking – licence journeys. Australia, Hong Kong, China, India, Japan, South Korea and Taiwan have framed their own virtual banking regulations and issued digital banking licenses. The Monetary Authority of Singapore (MAS) is reviewing applications, while Malaysia and Thailand are at the inception stage of drafting their digital banking frameworks.

However, the COVID-19 pandemic has inevitably resulted in economic instability and has also affected the deployment of virtual banking. While it is unclear how long the pandemic will last, regulators seek to prevent another systemic risk buildup similar to the global financial crisis of 2008.

Digital banking has taken relative importance amid social distancing measures. The use of online and mobile banking has increased and challenges from fintechs and bigtechs have emerged, prompting various lenders to enhance their digital offerings. These circumstances have made it necessary to review the current status of digital banking licences in Hong Kong, Singapore and Malaysia.

Hong Kong

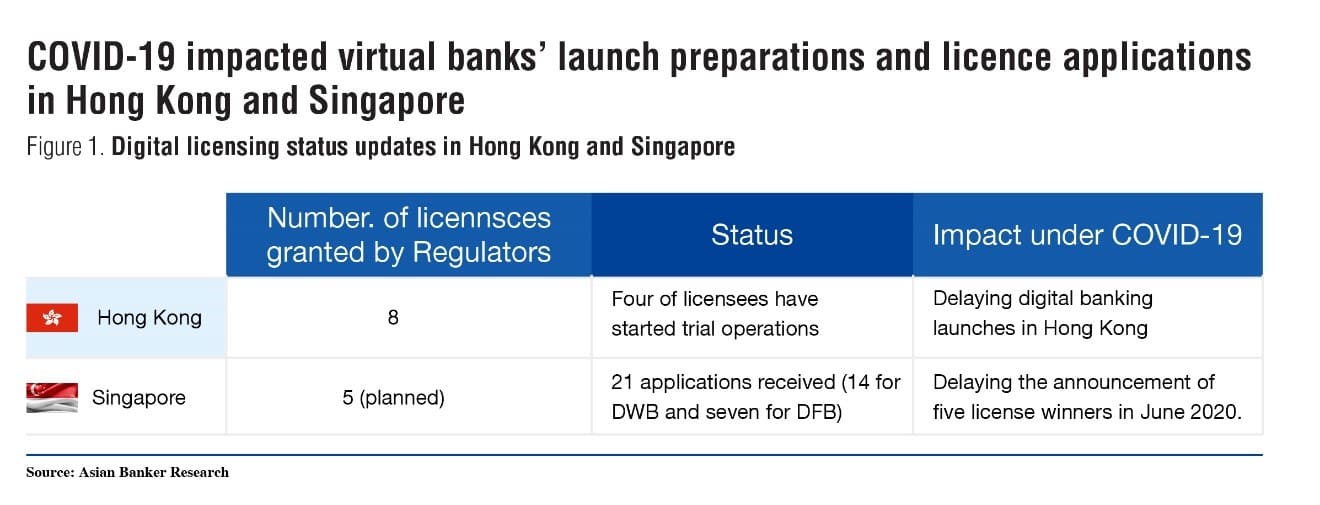

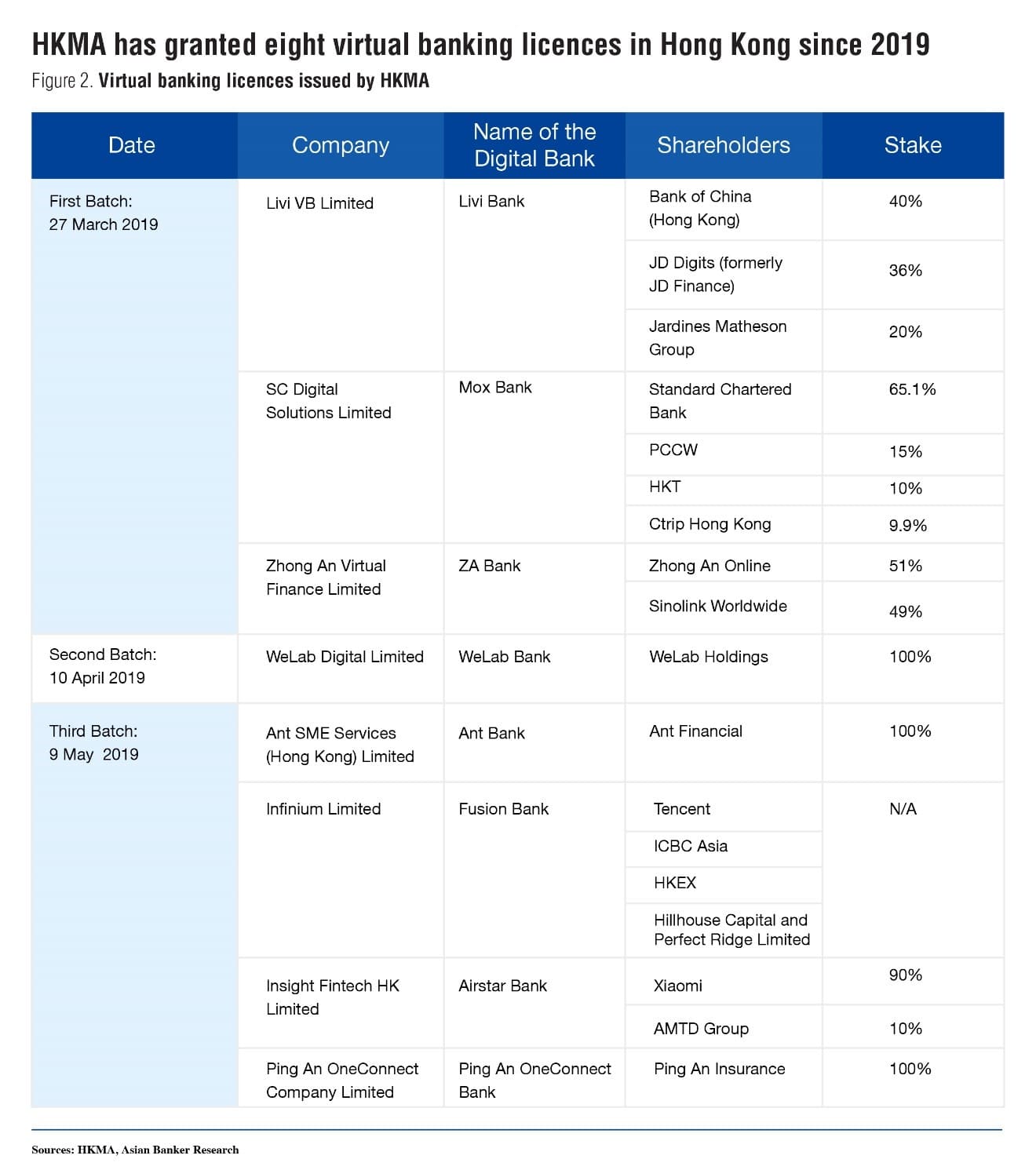

The Hong Kong Monetary Authority (HKMA) has issued eight virtual bank licences since March 2019 to various local banks, fintech, insurance companies and bigtech companies. The launch of virtual banks is said to be one of the key components of HKMA’s Smart Banking initiatives.

These virtual banks are expected to open within the next six to nine months, but the pandemic has affected such plans. Some of the approved virtual banks have failed to launch within the indicated time period.

Only ZA Bank has officially begun operations following a three-month trial in March 2020. ZA Bank launched a new product called ZA Savings Go, which offers high-interest-rate and introduced the first 30-minute personal loan pledge in Hong Kong, with $1.3 (HKD 10) for each minute delayed capped at $64.5 (HKD $500).

Four virtual banks – Airstar Bank, Ant Bank, WeLab Bank and Mox Bank – are piloting operations in the HKMA’s Fintech Supervisory Sandbox. Virtual banks commenced pilot operations to serve around 2000 customers with a range of digital-only services offering easy account opening, fixed deposits and savings accounts and other round-the-clock services. One innovative product to come out of this was the issuance of a numberless debit card from WeLab and Mastercard.

Ping An OneConnect Bank, Fusion Bank and Livi Bank have not disclosed planned launch dates.

The current rollout of virtual banks appears to be well-received. HKMA will continue to assess customer feedback, market acceptance and the impact on the banking system. Presently, the Hong Kong regulator is not considering issuing additional licences to more virtual bank players.

Singapore

As a financial hub in APAC, the Monetary Authority of Singapore (MAS) opened its door to digital banking and established a strong digital licence framework since August 2019.

MAS plans to issue five digital bank licences, with two digital full bank (DFB) licences and three digital wholesale bank (DWB) licences. A DFB licence allows a licensee to serve the retail segment and receive deposits from customers, while a DWB licence covers small and medium enterprises (SMEs) and non-retail segments.

For DFBs, successful licensees would first operate within a restricted phase before being allowed official, unrestricted operations. The differences between the two stages of a DFB are in the restrictions of offering complex investment products and deposit caps.

As of 31 December 2019, MAS has received 21 applications for digital bank licences – seven for DFB and 14 for DWB licences.

Digital bank licensees would compete directly with traditional incumbent banks in retail and SME banking with products that do not need face-to-face interaction. Both local and overseas players have joined the digital bank licence competition, including Ant Financial, Razer Fintech and ride-hailing giant Grab and telecommunications services provider Singtel.

%20outbreak01_Artboard%207%20copy(2).jpg)

MAS initially planned to announce the application results in June 2020 and licensees were expected to start their business operations by mid-2021. However, the pandemic has forced the regulator to extend the assessment of applications to the second half of the year. MAS said the delay would “allow the digital bank licence applicants to dedicate their resources and attention towards managing the immediate impact of the COVID-19 pandemic on their businesses.”

Malaysia

At the end of 2019, Bank Negara Malaysia (BNM) issued an Exposure Draft on Licensing Framework for Digital Banks. The regulator showed interest in granting five new digital bank licences in 2021 and it is keen on licensing qualified applicants who can establish digital banks that conduct either a conventional or Islamic banking business. The aim of the rollout for digital banks is to offset the market gaps and to provide financial products and services to the underserved and unserved segments.

Licence applications will only start after the issuance of the framework, but applicants will have to wait for now. Due to COVID-19, BNM has followed MAS and postponed its finalisation of the policy document on digital banking licensing framework to end of June 2020 or possibly beyond.

Amid Malaysia’s movement control order (MCO), there was an increase in the creation of online SME banking accounts for money transfer instead of depositing cheques at physical branches. As BNM extends its digital banking framework deadlines, how applicants utilise this phase matters during both the MCO and the post COVID-19 periods.

Countries such as Malaysia and Thailand, which haven’t begun the process of licence applications just yet, might have more time to prepare under the pandemic. For licensed banks, the crisis period would be a good test for service efficiency, customer experience and system architecture. With the markets under various stages of their planned digital banking licence rollout, it is likely that 2020 will usher in a new era of virtual banks in the Asia Pacific.

.png)

.webp)