- A more challenging operating environment that has impacted profits is forcing banks to trim their cost structures and invest in technology.

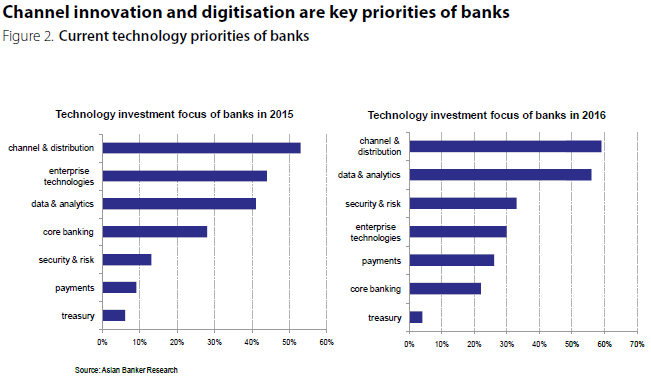

- More than 55% of surveyed banks are focused on improving their channel capabilities, particularly mobile banking.

- Data and analytics is a strong priority for banks with more than 50% surveyed banks preparing new initiatives to advance their analytical insight capabilities.

The banking industry today is facing an unparalleled level and pace of change in technology development. Banks are updating their systems and processes to meet changing customer expectations amid increasing competition from bank and nonbank players.

Disruption has been rapid and pervasive in the industry. Fintech innovation is forcing banks to accelerate their digital initiatives and to rapidly invest in technology for better customer experience, agility in products and services development, and improved efficiency. There is now a paradigm shift in the thought processes of incumbent organisations towards faster technology adoption.

The Asian Banker surveyed 35 financial institutions in Asia Pacific to get a better look at their recent technology priorities. Mobile banking, data analytics, security, and cloud computing are some of the main priorities of banks for technology investments.

Key trends in technology investments

A more challenging operating environment that has impacted profits is forcing banks to trim their cost structures. However, investing in banking technologies remains significant although it strongly varies across banks based on their capabilities, needs, and strategic priorities. Furthermore, the competitive market and operational priorities play significant roles in the banks’ strategic investment decisions.

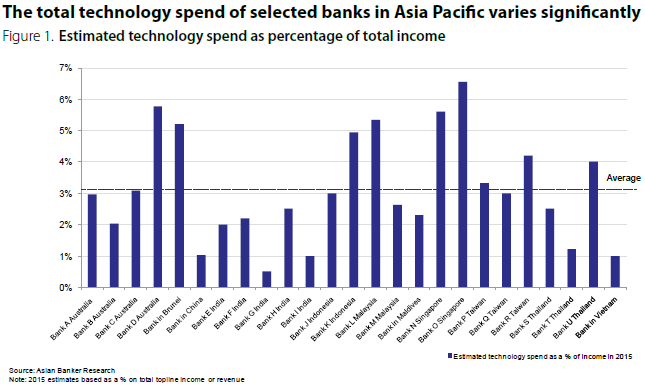

Banks do not generally disclose the details of their technology spending, especially between operating expenditure and capital investments. However, an average of 3.1% of the surveyed banks’ total income was spent on technology in 2015, which includes their operating and capital technology expenditures (Figure 1).

The survey also revealed that digital transformation remains a key priority. Channel enablement – through mobile banking for improved customer experience and service – is the most common area for technology development and investment. Data analytics, security, and cloud technologies are other initiatives that banks prioritise in 2016 (Figure 2).

Enhancing mobile and customer

Channel experience and innovation are aggressively being explored by most banks in the region. More than 55% of banks are focused on improving their channel capabilities, particularly mobile banking and other self-service channels. The explosive growth of smartphone technologies brought strategic change in the ways banks target their customers. In addition, digitising customer interaction and experience remains a key priority in 2016. Some of the notable examples are near field communication- (NFC) based mobile payments, real-time peer-to-peer payments, and personal finance management applications. Service differentiation and unparalleled convenience of transactions form the key foundations for these innovations across the globe.

UOB Singapore, for example, launched its integrated app ‘UOB Mighty’, which focuses on customers transactional and lifestyle needs, and contactless payments with tokenised security through host

card emulation (HCE). Likewise, Australia’s ANZ goMoney uses HCE technology to replicate the contactless card chip for NFC payments (credit or debit card purchases) in android phones.

Banks are facing increased competition from emerging new players and fintechs, forcing them to innovate. For example, Moven’s debit account provides customers with instant transaction and status notifications through a smartphone app. This helps customers monitor their spending patterns against average behaviour and real-time spending insights.

Banks are also actively investing in peer-to-peer transfers through mobile banking as well as developing an ecosystem around payments and retail purchases through mobile phones. China Merchants Bank, for example, introduced services using global positioning system (GPS), voice recognition, and payments by QR codes. It also established value added services such as instant loan

approvals, daily lifestyle related payment features, inquiry of outlet queuing situations, and mobile-based NFC payments.

Branch automation has also emerged as a priority to improve straight-through processing and customer experience. More digitised and self-service enabled branches are being introduced to redefine the models of ‘branch outlet’. There is an increased deployment of electronic kiosks with virtual teller machines providing counter services to customers via live video conferencing. These are enabling banks extend their services beyond the traditional working hours while keeping costs under check. For example, Shinhan Bank has started replacing its branches with fully automated NFC and biometrics-enabled digital kiosks for immediate account opening, instant passbook and cards processing, and other banking transactions.

Social engagement is also becoming a priority for banks who invest in services provided through social media channels. These channels are used to disseminate information that are relevant to the banking and lifestyle needs of customers and to provide an avenue for query resolution. Selected banks in India like ICICI Bank and Axis Bank have already initiated Facebook and Twitter-based banking services. Bank of China (Hong Kong), on the other hand, has launched an innovative enquiry service through WeChat, which includes a smart ‘robot’ customer service feature that analyses text inputs and provides relevant pre-set answers.

Advanced insights through data and analytics

Banks are generating vast volumes of data from digital and social media channels that they can effectively utilise to expand their analyticsbased insights and understanding of their customers. In fact, more than 50% of surveyed banks are preparing new initiatives to advance their data and analytics capabilities.

Leading banks are planning to develop their data and analytics ecosystems to provide the right information at the right time, generate higher sales, and provide differentiated customer experience. Banks are also experimenting with locational intelligence to better track and target customers.

However, to effectively use these analytical insights, a strong data foundation within a bank is needed. Many banks have data residing in operational silos, which serve as a challenge in getting integrated analytic insights. Selected banks are also investing in new enterprise data warehouses, a significant investment that consumes time but provide valuable benefits such as faster decision making, improved efficiency, faster response time, and better business processes.

Furthermore, enabling data insights for effective contextual marketing remains a key objective. Access to real-time information and insights into customer behaviour and recommendations has been effective in targeted precision marketing of customers. Another emerging enabler for the analysis of extensive unstructured big data is cognitive computing. This is being used to derive personalised engagement strategies and recommendations for the customers. ANZ has expanded the use of cognitive computing in global areas like advisory, risk, and back office automation. DBS, on the other hand, is in the process of implementing cognitive computing for its wealth management business.

Heightened cyber security and risk concerns

Regulators and financial institutions are grappling with the threat brought about by different forms of cyber fraud and attack. Security concerns are now creeping up decision makers’ priority list as digital services proliferate. Fast and nimble fraudsters seem to always be a step ahead of banks in exploiting loopholes in technology systems and processes to perpetrate crimes. Banks have realised that they cannot manage these threats through a single solution. Instead, there is a need for increased multi-layered solutions for intrusion protection, system recovery, analytics insight, strong monitoring, and customer education. In fact, over 30% of the surveyed banks are planning to invest in security risk management in 2016.

Using biometrics such as finger print, veins, heartbeat, voice, and iris for authentication are also being explored. For example, Citibank has already implemented voice biometrics while Shinhan Bank in South Korea and CTBC Bank in Taiwan have introduced vein biometrics in self-service banking kiosks. The government of India has also started an initiative towards biometric-enabled unique identification cards, prompting many banks to explore finger print enabled transactions.

In addition, regulators such as the Monetary Authority of Singapore (MAS) are pushing banks to build a robust technology risk management framework, with focus on disaster recovery, system availability, and business continuity. Strong risk monitoring and analytics solutions are being placed. Banks are also investing in targeted initiatives such as distributed denial of service (DDoS) solutions to have an effective early warning against online attacks.

Increased outsourcing and the introduction of application programming interface (API) banking are pushing banks to invest on centralised security control of information assets exposed through APIs, ensure availability of services, and secure interfaces with technology partners.

Infrastructure modernisation and cloud adoption

Banks are strongly focused on converting legacy infrastructure to modern systems and architecture for better efficiency and agility. Over 40% of the surveyed banks have invested in enterprise technologies including back-end infrastructure. Banks are also looking for enhanced storage capacity aside from better servers, networks, and legacy platforms. In addition, cloud computing has become a key component in the long-term strategies of bank looking for greater agility at lower costs. Regulatory and security concerns continue to impede the expansion of cloud computing in critical functions that include customer data, especially through public clouds. Nonetheless, there has been a growth in cloud computing initiatives for selected functions through private and hybrid clouds in shared environment.

The current business agenda of most banks in Asia Pacific is driven by technology and digital transformation. The entry of technology companies in financial services has accelerated the innovations in digitisation and channel capabilities, which have changed customer expectations. These changes are forcing banks to revisit their existing technology systems and models. As emerging competition accelerates, technology innovation within the banking community is likely to gather pace.

.png)

.webp)