- US remains the top destination for fintech investment

- APAC fintech funding nosedives in 2023

- Valuations get a reality check

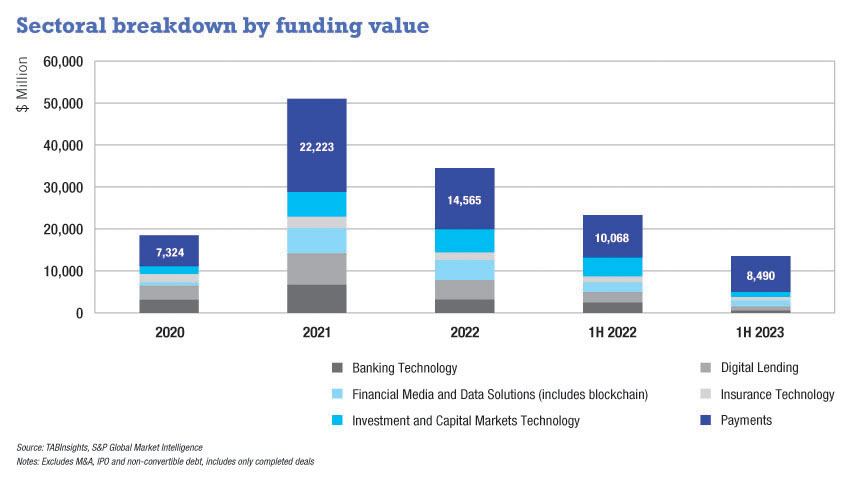

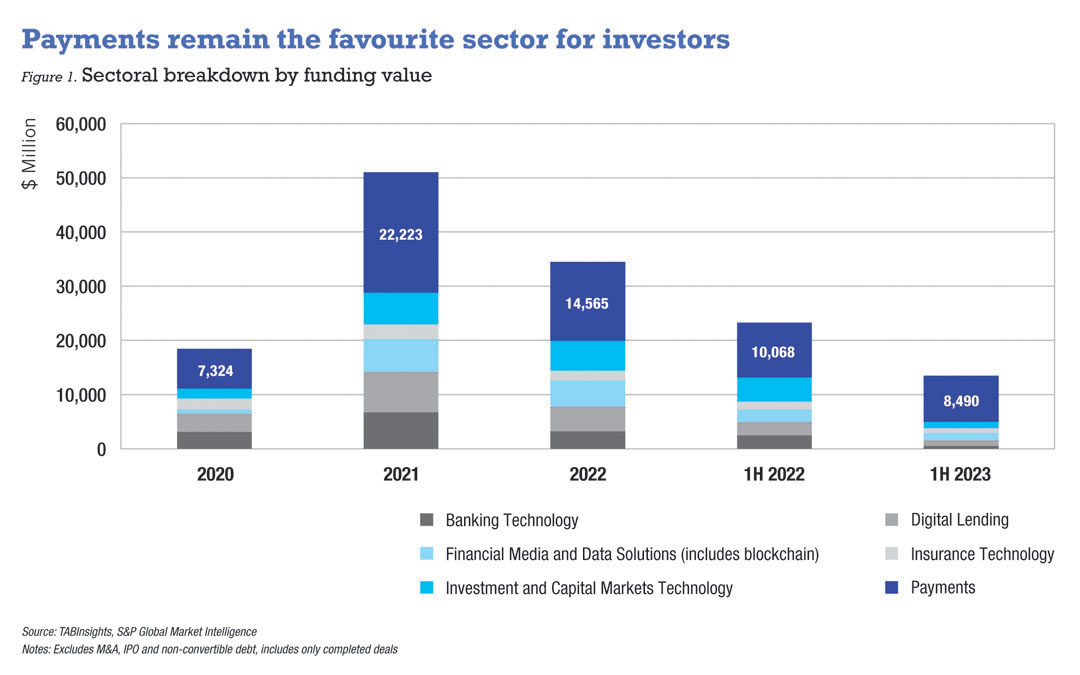

Global venture capital (VC) investments in fintech dropped by 32% in 2022 to $34 billion from an unprecedented high of $51 billion in 2021. The decline in investment becomes more prominent in the first half of 2023 with a 42% decline in funding by value and a 50% drop in the number of deals year-on-year (YoY), according to a TABInsights analysis of S&P Global data. The total global funding raised till June 2023 was $13.5 billion, 74% of which went to the US and Canada. If it was not for the mega funding deal by Stripe amounting to $6.8 billion, the funding drop this year would have been even more prominent.

Payment sector gets a higher share of funding in 2023

With the growth in digital payment volumes and popularity, the payment sector has remained a favourite for investors, contributing to over 44% in 2021 and 42% in 2022 of the total funds raised. In 2023, this rose to 63% especially due to the large funding raised by Stripe. The sector contributed to 36% of the number of deals in 2022 and 33% in 2023. Other sectors that claimed investor interests are financial media, data solutions and blockchain that account for 10% of the total funds raised, and 9% of the investment and capital market.

US remains the top destination for fintech investment

The US continues to be the favourite investment destination. However, in 2022 because of several mega-deals in Europe such as FNZ ($1.4 billion), Checkout ($1 billion) and Klarna ($800 million), the total funding value in Europe was higher, despite the number of deals being higher in the US and Canada. Meanwhile, contribution to Asia Pacific (APAC) was close to 20% of the funds raised in 2022. In the first half of 2023, 74% of funding has gone to the US, with the share to APAC dropping to 12% and Europe to 10%.

Significant funding from investors has flown to late-stage and mature companies. In 2022, mega deals in APAC include Singapore-based cryptocurrency payment company MoonPay ($642 million), digital-asset company Amber Group ($300 million), and South Korea’s Viva Republica that operates super-app Toss ($402 million).

In 2023, besides the Stripe deal worth $6.8 billion, custody and brokerage company Clear Street raised $435 million, and market intelligence and search platform Alphasense raised $325 million in the US. In APAC, notable deals include Singapore-based buy-now-pay-later and lending company Kredivo ($270 million).

APAC fintech funding nosedives in 2023

Fintech funding to APAC had risen to $9.2 billion in 2021, and dropped by 26% to $6.8 billion in 2022. The first half of 2023 witnessed a steeper decline to $1.6 billion, a drop of 57% in value and 48% in deals, YoY.

Asia offers the advantages of a younger workforce and population, a rapidly-growing digital economy and payments arena, and potential for financial inclusion. The payment sector has been the favourite sector for investment in APAC, however, 2023 saw higher funds flow into the digital lending sector. China, once among the most popular destinations for funding, continues to see a significant drop in VC investment amidst higher risk perception and clampdown on tech companies. India led the investment flow in Asia for the last two years, with 28% of the total funding for Asia in 2022 flowing into the country. The first half of 2023 witnessed several larger deals in Singapore, surpassing investment flow to India. Meanwhile, South Korea emerged as the only country in Asia that increased the total fintech funding in the first half of 2023 YoY.

Valuations get a reality check

Geopolitical uncertainties, soaring inflation, high-interest rates and economic downturn are some of the key macroeconomic considerations that lower the risk appetite. The bursting of the fintech-funding bubble is a wake-up call for the industry, accentuating the need for more financially sustainable businesses and a reality check on the highly inflated valuations. Meanwhile, the industry is realising that the valuation must be justifiable.

Several highly-valued fintech had a hard landing when listed on capital markets and now quote well below their IPO prices, including companies such as Opendoor technologies, Affirm, Coinbase, Paytm, and Grab. Unlisted leading fintechs like Klarna, Revolut and N26 saw a drop in their valuations as they raised additional funding from VC.

This also drives home the fact that long-term success requires a strong business model supported by a robust team and effective execution, and the ability to scale with speed and grow into a financially thriving and profitable business. Investors’ risk appetite has been dented; they seem to prioritise profitability and cash flow and support stronger and mature companies with more reasonable valuations.

.png)

.webp)