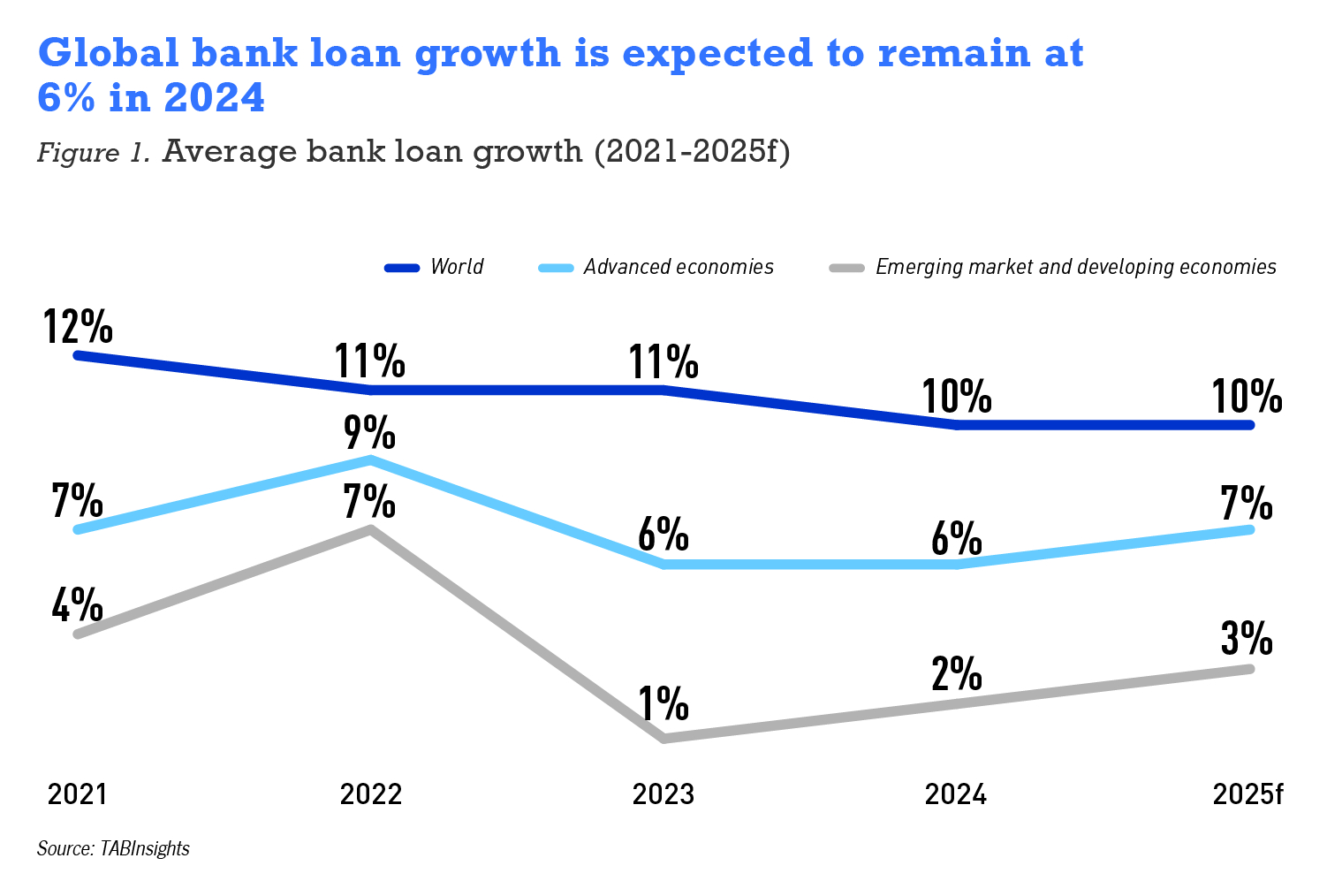

The global average bank loan growth rate declined from 9% in 2022 to 6% in 2023. This was due to adjusting demand in response to lower growth expectations and heightened interest rates, along with banks enforcing stricter lending standards. This trend, identified in a study of 12 key advanced economies and 12 key emerging market and developing economies, was primarily driven by advanced economies. All 12 advanced economies experienced a deceleration in bank loan growth, with the average rate dropping from 7% in 2022 to 1% in 2023. In contrast, emerging market and developing economies maintained a steady average bank loan growth rate of 11%.

In the light of a less favorable economic outlook and high borrowing costs, global bank loan growth is anticipated to linger at 6% in 2024, with advanced economies projected at 2% and emerging market and developing economies at 10%. Despite the anticipated overall weak loan growth in 2024, some economies, including Indonesia, Korea, Malaysia, Qatar, Singapore, Taiwan, and Vietnam, are expected to witness an improvement.

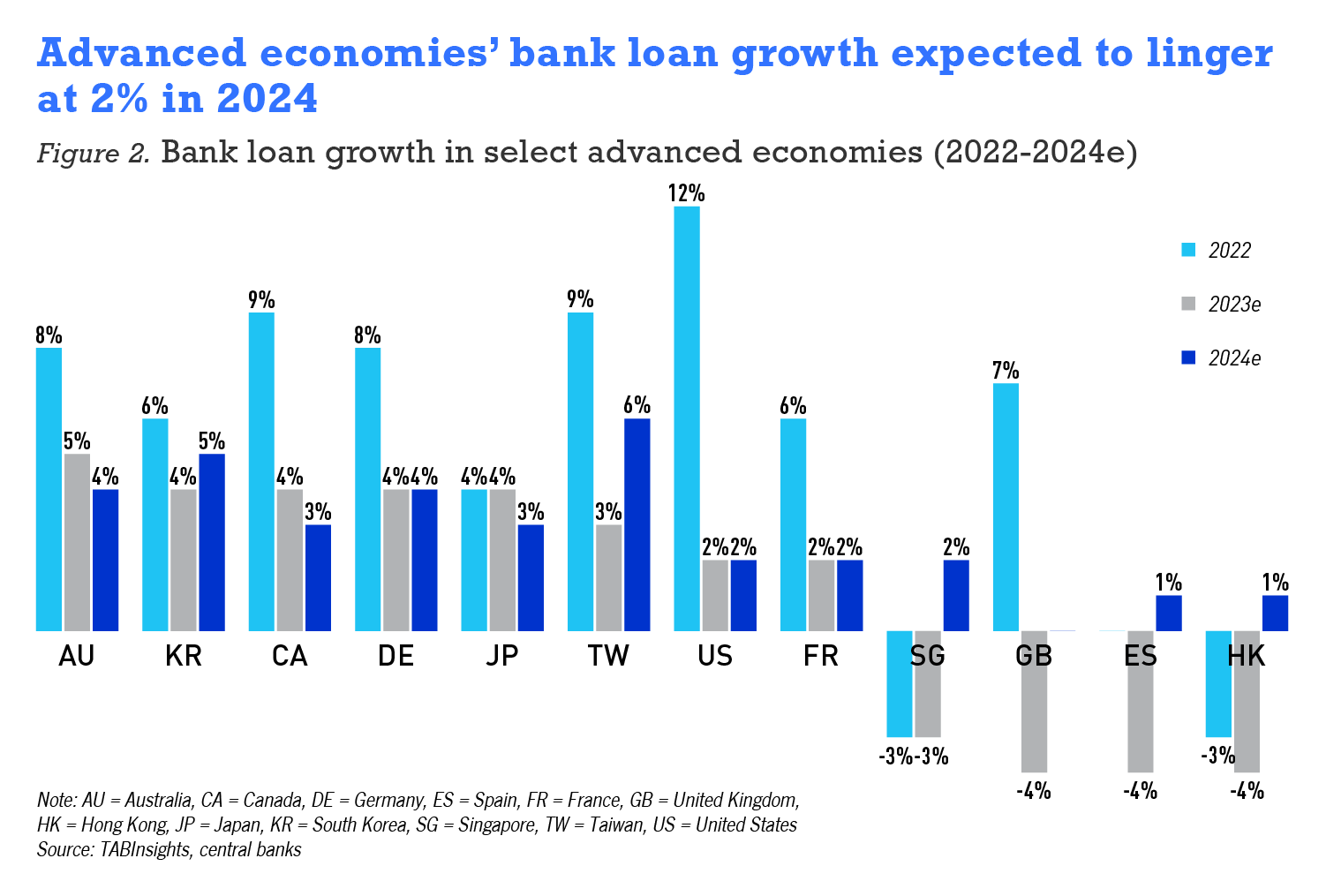

UK and US saw the most significant deceleration

Among the 12 advanced economies, the UK and the US experienced the most substantial deceleration in bank loan growth. This contraction was primarily attributed to weakened loan demand amid higher borrowing costs. Concurrently, banks tightened lending standards over concerns about credit quality, funding costs, and liquidity positions. Additionally, economies like Taiwan, Canada, and France also saw a considerable slowdown in bank loan growth.

In the US, the growth rate of bank loans decelerated from 12% in 2022 to 2.3% in 2023, driven by a slowdown across all loan categories. Real estate loans, constituting 45% of total bank loans in the US, grew by 3.3% in 2023, compared to 12% in 2022. Commercial and industrial loans of US banks declined by 1.1% in 2023, in contrast to a growth rate of 14% in 2022. Consumer loans grew by 3.8% in 2023, compared to 11% in 2022. In 2024, bank loan growth in the US is projected to remain weak, as tight credit standards and weak demand are expected to persist, and US banks are anticipated to preserve liquidity conditions with restrained loan growth.

In the UK, total bank loans saw a year-on-year (YoY) decline of 3.6% in November 2023, in stark contrast to the 7.1% expansion observed in 2022. Loans to the private sector witnessed a YoY decrease of 1%, while loans to non-residents fell by 5.7%. Bank loan growth in the UK is expected to improve in 2024 but remain weak due to a sluggish domestic economy. The Financial Policy Committee noted that the full impact of higher interest rates is yet to unfold, presenting ongoing challenges for households, businesses, and governments.

Bank loans contracted in Hong Kong, Singapore, Spain, and UK

In addition to the UK, several other advanced economies also experienced a decline in bank loans in 2023, including Hong Kong, Singapore and Spain. Bank loans in all these three economies dropped in both 2022 and 2023.

In Hong Kong, total bank loans declined by 4.4% YoY in November 2023, following a 3% decline in 2022. Loans for use outside Hong Kong, constituting 25% of total loans, plummeted by 11.4% YoY in November 2023. This drop was driven by weakened demand from mainland China, influenced by lower borrowing costs in mainland China. Meanwhile, loans for use in Hong Kong dropped by 0.8% YoY in November 2023, attributed to reduced financing for development and property investment amid a correction in the property market.

Singapore experienced a 2.6% decline in total bank loans in 2022, followed by a 3% YoY drop in November 2023. This decline was influenced by decreases in both loans to residents and loans to non-residents. Bank loan growth in both economies is expected to experience a slight improvement in 2024, but loan demand is anticipated to be restrained.

On the other hand, Australia, South Korea, Canada, and Germany demonstrated stronger bank loan growth compared to other advanced economies, ranging from 4% to 5%.

In Australia, bank loan growth slowed from 7.5% in 2022 to 4.9% YoY in September 2023, with expectations of a further decline to 4% in 2024 due to a strict monetary policy and economic downturn, while mortgage competition persists.

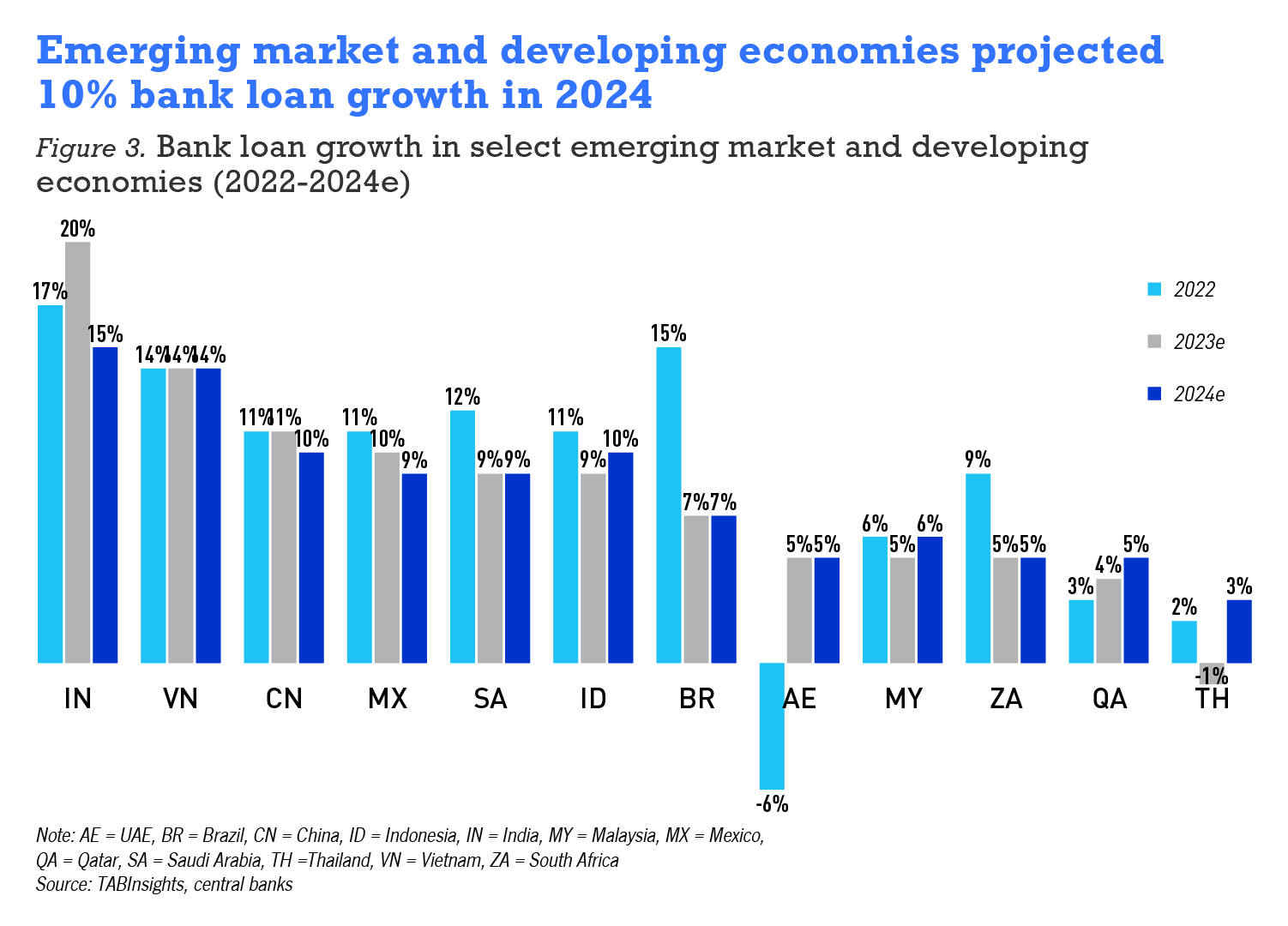

India saw strongest loan growth, China and Vietnam maintained double-digit growth

While eight of the 12 emerging market and developing economies saw a deceleration in bank loan growth, China and India, the two largest emerging markets, maintained double-digit loan growth.

India stood out with the strongest bank loan growth, accelerating to 20% YoY in September 2023 from 16.8% YoY in 2022. The heightened demand for loans was driven by the normalisation of economic activity post the COVID-19 pandemic. In November 2023, the Reserve Bank of India tightened norms for unsecured loans as they were growing nearly twice as fast as total lending, requiring lenders to set aside higher capital buffers. However, India’s loan growth is poised to remain robust in 2024, supported by consistent and strong loan demand.

China also maintained a strong pace of bank loan growth at 11% YoY in September 2023, supported by accommodative central bank policies aimed at shoring up a fragile economic recovery. The encouragement of banks in November 2023 to support the private sector, particularly real estate, is expected to contribute to China’s loan growth hovering around 10% in 2024.

In Vietnam, credit growth remained robust at 13.5% in 2023, though it represented a slight deceleration from the 14.2% credit growth observed in 2022. Banks introduced attractive loan packages to boost credit demand following multiple deposit interest rate reductions. This figure fell slightly below the State Bank of Vietnam’s initial target range of around 14% to 15% for 2023.

In Mexico, Saudi Arabia, and Indonesia, robust growth in total loans ranging from 9% to 10% was observed, although there was a moderation in bank loan growth in these markets.

On the other hand, the United Arab Emirates experienced a remarkable turnaround, with bank loan growth reaching 5.1% YoY in October 2023, compared to a negative 5.9% YoY in 2022, attributed to a thriving domestic economy and buoyant oil prices.

In contrast, Thai banks faced the slowest loan growth among these emerging markets and developing economies, with total loans declining by 0.9% YoY in November 2023. This was attributed to gradual business loan repayments, along with the banks’ prudent portfolio management.

Additionally, economies like Brazil and South Africa also witnessed a moderation in bank loan growth in 2023. In Brazil, loan growth significantly decelerated from 16.1% YoY in 2021 and 14.7% YoY in 2022 to 7.2% in November 2023, influenced by restrictive monetary policies and an increase in credit default rates.

Some economies anticipate improvement despite weak growth

While the overall global bank loan growth is expected to remain subdued, some economies anticipate improvement in 2024. Advanced economies such as Hong Kong, Singapore, and the UK are projected to experience a slight increase in overall bank loan growth to 2% in 2024, driven by improvements in economies that had negative bank loan growth in 2023. Additionally, Taiwan and Korea are also expected to witness higher loan growth. Taiwanese banks are forecasted to achieve 5% loan growth in 2024, up from 3% in 2023, fueled by improved domestic economic growth prospects. Korea’s bank loan growth is expected to improve from 4.4% YoY in October 2023 to 5.4% in 2024.

In emerging market and developing economies, the overall bank loan growth is anticipated to moderate slightly to 10% in 2024, with improvements expected in countries like Indonesia, Malaysia, Qatar, and Vietnam. In 2024, Bank Indonesia plans to boost bank lending by infusing liquidity into the banking sector. The Malaysian banking sector is poised for improved loan growth, driven by solid domestic demand, a robust labour market, and government initiatives such as the New Industrial Master Plan 2030. The State Bank of Vietnam has set a credit growth target of 15% for Vietnam’s banking system in 2024, with the business environment expected to become more favourable in the coming years.

.png)

.webp)