- Overall Double 11 sales increased despite economic hurdles, with emerging e-commerce entrants outpacing Alibaba and JD.com in sales growth

- Pinduoduo's distinctive model and strategic evolution boosted market influence, with an estimated 19% YoY GMV growth in 2023

- Chinese e-commerce firms adopted cost-effective strategies to attract value-conscious consumers

The competition in China's e-commerce market has intensified in recent years, with emerging players such as Pinduoduo, Douyin, and Kuaishou challenging the dominance of traditional e-commerce giants Alibaba and JD.com. These emerging platforms leverage innovative, entertainment-blended retail models. Pinduoduo combines group-buying and social media, while Douyin and Kuaishou promote products through content creation and influencer partnerships rather than direct advertising.

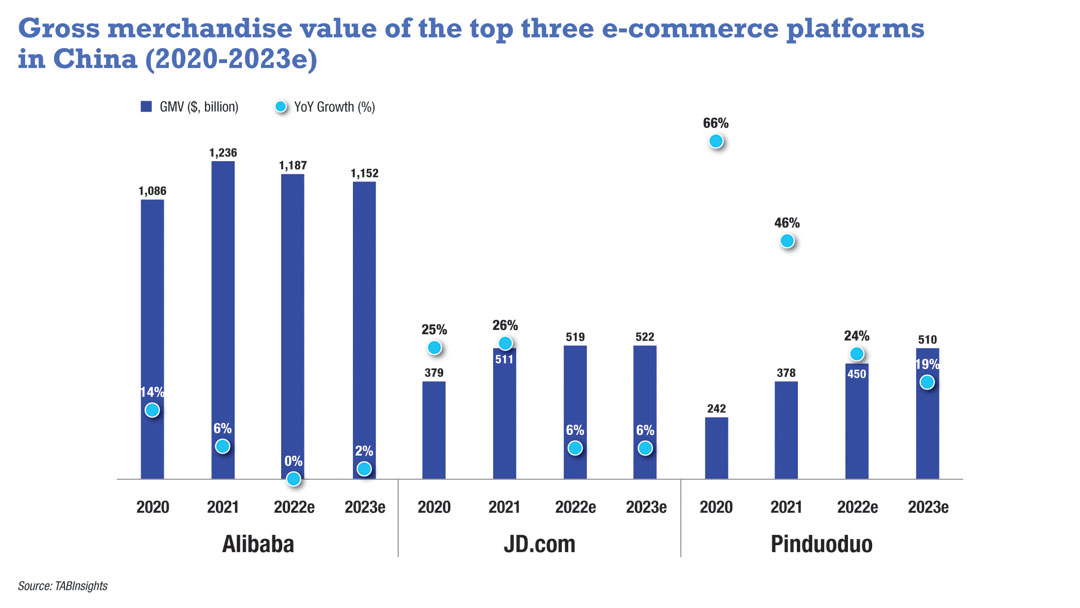

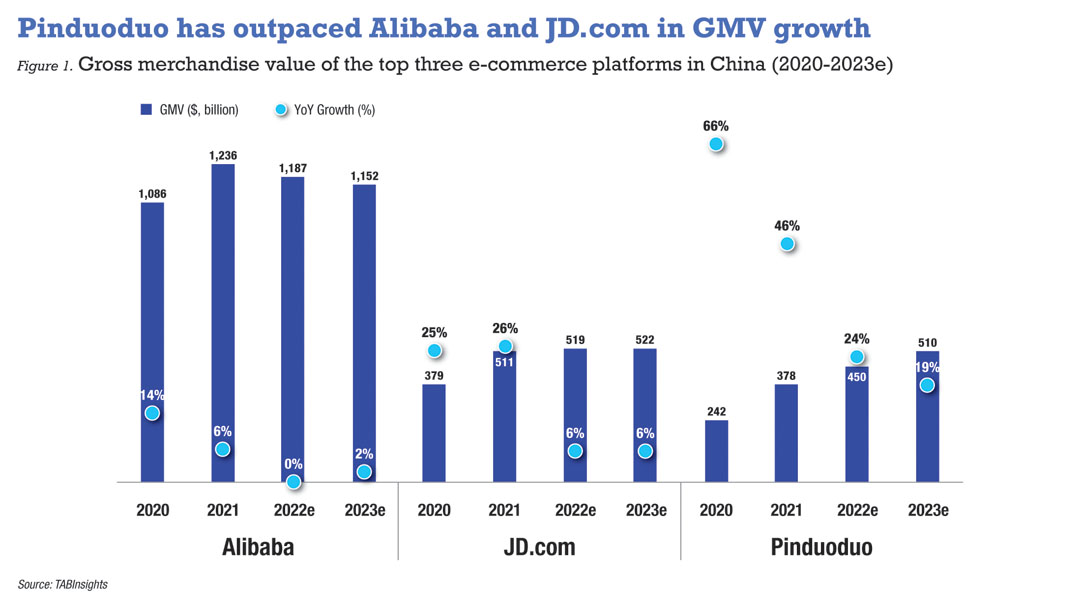

Pinduoduo, despite its growth trailing behind Douyin and Kuaishou, stands out as the third-largest e-commerce platform in terms of gross merchandise value (GMV), with around $450 billion in 2022 and $510 billion in 2023. Its inventive marketing strategies include incentives like discounts and cashback for user invitations. Shifting from early subsidies, it now emphasises product quality and brand-building after securing a substantial user base.

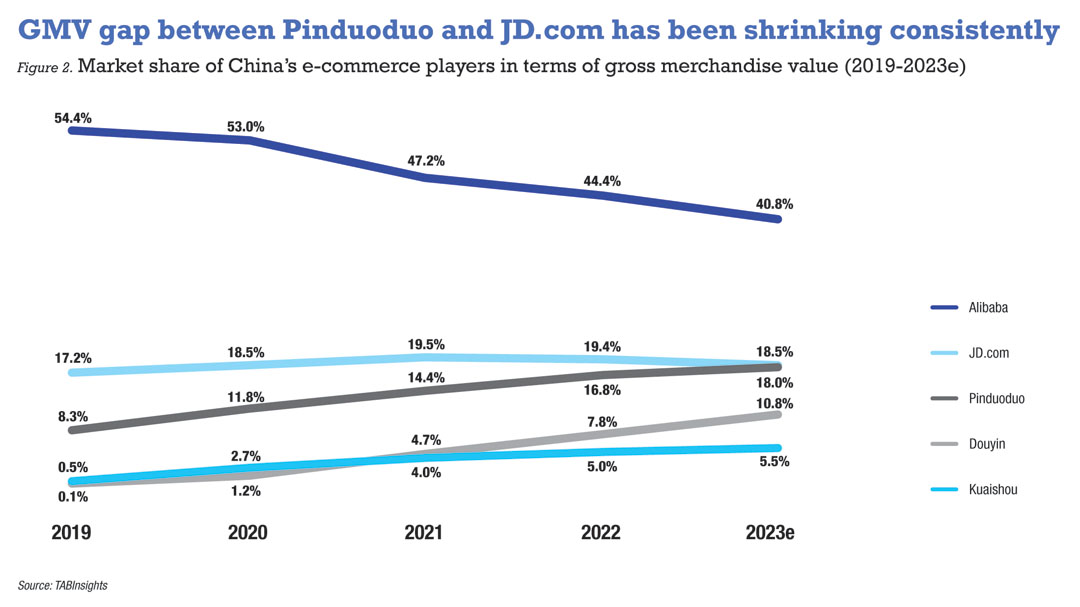

While Alibaba remains the largest e-commerce platform in China, it has experienced a decline in market share within the industry. JD.com, a significant e-commerce platform known for its focus on direct selling and proprietary logistics infrastructure, also saw a slight decrease in its GMV market share in 2022.

Sales rose despite economic challenges and changing consumer behavior

During this year's Double 11 shopping event, sales and order volumes saw an upswing despite economic challenges and shifts in consumer behaviors in China, reaching around $155 billion in GMV.

The 0.2% dip in China’s consumer price index for October 2023, subsequent to a stagnant reading in September, indicates an unstable recovery and restrained domestic consumption. Additionally, consumers show diminishing enthusiasm for the Double 11 shopping festival, now in its 15th year, amid a crowded promotional calendar and the popularity of shopping on livestreaming channels.

While exact sales figures were not disclosed by e-commerce platforms, Alibaba highlighted positive year-on-year (YoY) growth in GMV, order volume, and participating merchants on its Tmall and Taobao platforms. Similarly, JD.com noted record highs in transaction volume, order volume, and user engagement during this shopping season. Alibaba’s GMV is estimated to have increased by roughly 2% during the event, while JD.com is expected to report 4% growth in GMV. The relatively newer players such as Pinduoduo, Douyin, and Kuaishou are estimated to have experienced significantly higher Double 11 GMV growth compared to Alibaba and JD.com.

Pinduoduo propelled by unique business model and strategic transformation

Established in 2015, Pinduoduo has fortified its market position through a focus on consumer experience and the integration of digital customer interaction. Fueled by the customer-to-manufacturer (C2M) model and the infusion of social elements into the shopping experience, the platform has seen substantial growth, increasing annual active buyers from 244.8 million in 2017 to 881.9 million in Q12022.

Pinduoduo’s GMV surged significantly from RMB 1 trillion ($146 billion) in 2019 to roughly RMB 3 trillion ($453 billion) in 2022, exhibiting a compound annual growth rate of 45%. In 2022, Pinduoduo secured a 17% market share, trailing slightly behind JD.com's 19%. Despite facing controversies such as counterfeit products and data privacy concerns, Pinduoduo continues its robust growth. The GMV gap between Pinduoduo and JD.com is steadily narrowing, positioning Pinduoduo to surpass JD.com as the second-largest e-commerce player by GMV in 2024.

Since initiating its strategic transformation in 2021, Pinduoduo has consistently prioritised research and development (R&D) investment. In 2022, the company's R&D team saw steady 15% growth, comprising about half of the total workforce. In May 2023, Pinduoduo announced the establishment of a "10 billion ecology" special project, designed to direct resources toward high-quality merchants and goods. This initiative aims to foster the quality growth of small and medium-sized enterprises, enhance overall service efficiency, and elevate the standard of platform merchants.

E-commerce players employed low-price strategies to entice value-seeking consumers

Adapting to evolving consumer behavior amid economic uncertainty, Chinese e-commerce platforms strategically offer significant discounts and subsidies to attract shoppers. JD.com launched a substantial RMB 10 billion ($1.4 billion) subsidy campaign in March 2023, highlighting its commitment to a low-price strategy. This initiative extends subsidies to suppliers for more competitive pricing, aligning with the evolving consumer preference for value-driven purchases.

Major players like Alibaba and JD.com streamlined promotions, focusing on direct price cuts to entice cost-conscious consumers. Alibaba led the charge by pressuring merchants to slash prices, aiming to present 80 million products at their lowest prices during the festival’s launch in late October. JD.com introduced a 30-day best-price guarantee for over 800 million products, vowing to reimburse the price difference if shoppers find cheaper alternatives elsewhere.

.png)

.webp)