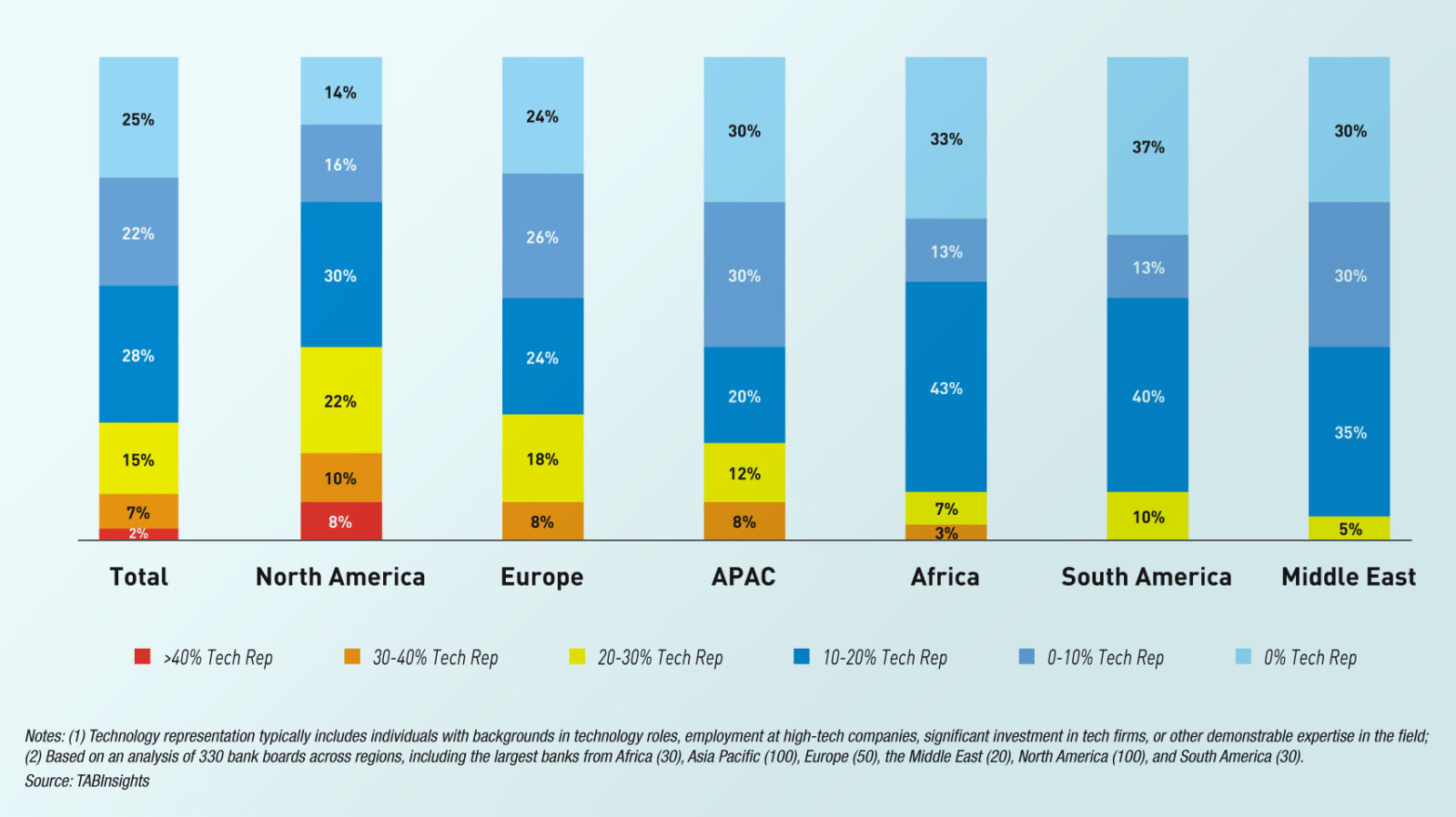

.png)

- Digital banking has progressed at different paces in different markets in Asia Pacific, becoming more widespread in developed economies

- However, due to security concerns, many consumers do not prefer to engage in digital banking

- Banks have to act quickly to enhance the security of their digital banking channels and to improve the customers' digital experience

Digital banking has become incredibly important channels for banks, as an increasing number of customers prefer using digital devices to conduct banking activities due to the simplicity and convenience.

Banks have invested substantially in digital capabilities and have been aggressively improving the adoption and usage of lower-cost digital channels to deepen customer relationships and to enhance customer’s banking experience. Digital banking will continue to grow steadily in the Asia Pacific region, driven by favourable demographics, broader access to digital devices, and improving network connectivity.

Across the region, digital banking has progressed at different paces in different markets. In developed markets, digital banking is more widespread. Australia and South Korea lead the region in digital banking activities. Australian banks are early adopters of internet banking and mobile banking, and they have continuously developed user-friendly mobile banking applications to meet the increasingly demanding customers’ digital needs. The digital banking penetration in emerging markets such as India, Indonesia and the Philippines is relatively lower. However, these markets have seen stronger increase in digital banking over the past few years. The increasing need for digital banking in these markets is mainly driven by high mobile penetration, low access to banking services and a highly dispersed geography. The unbanked and underbanked customers have begun to be served through their mobile devices.

Customers have been continuously migrating routine transactions from traditional channels to digital channels. Therefore, many banks are paring down branches and reducing headcount in response to the increase in the digital banking transactions. For example, the number of bank branches in South Korea dropped to 7,103 branches in 2016 from 7,278 branches in the previous year. Australian banks also cut their branch networks by 2% to 5,537 branches as of June 2016. However, physical branches are still in demand and they will retain an important role for the foreseeable future. Although customers use digital banking more often, they are not abandoning physical channels.

Concerns over the security of digital banking services are the main reason why consumers do not engage in digital banking. Meanwhile, cybersecurity issues are also a concern of those who use digital banking services. Banks are working to improve the security of digital banking services and also simplify the authentication processes to make them user friendly. Banks and customers have started to embrace biometric authentication technology, as it combines security and convenience. In addition, biometric security also helps to minimises the risk of forgetting login details. Going forward, more banks will adopt biometrics to validate customers, especially fingerprint-based biometrics.

Despite steady growth in the use of digital banking, most consumers are not ready to bank exclusively via digital. A few digital-only banks have been launched in the region, which is not a competitive threat to traditional banks for now. Digital-only banking is most popular in developing markets with large underserved consumers and relatively thin branch network, such as India, Indonesia and Vietnam. In the future, digital-only banks have the potential to exert an influence on the banking sector.

Mobile banking to overtake internet banking

In most developed markets, internet banking has reached near-saturation levels and banks have been focusing more on mobile banking in recent years. An increasing number of consumers have shifted most of their transactions to mobile banking, and thus some banks have seen a decrease in the use of internet banking. In emerging markets, both internet and mobile banking are increasing remarkably. However, the growth of mobile banking is more impressive. Many new digital banking users will choose smartphone as the device to conduct banking activities in these markets. Currently, more banking transactions are still conducted via computers than mobile devices in most markets.

However, mobile banking is rising at a much faster pace. In some markets, mobile banking has already overtaken internet banking in terms of transaction volume and number of subscribers. Going forward, the trend will accelerate. Mobile banking is set to become the dominant banking channel for customers to interact with their banks.

Banks are facing rising customer expectations and falling customer loyalty. It is easier than ever for customers to switch banks. User experience is vital in improving customer satisfaction and customer retention. Mobile banking channel must be enhanced for banks to remain competitive. Banks can try to deliver comprehensive mobile banking services, such as deposits, withdrawals and lending. In addition, banks should make use of advanced data analytics technologies to offer customers targeted banking products and services that are aimed at specific user needs and experience.

China

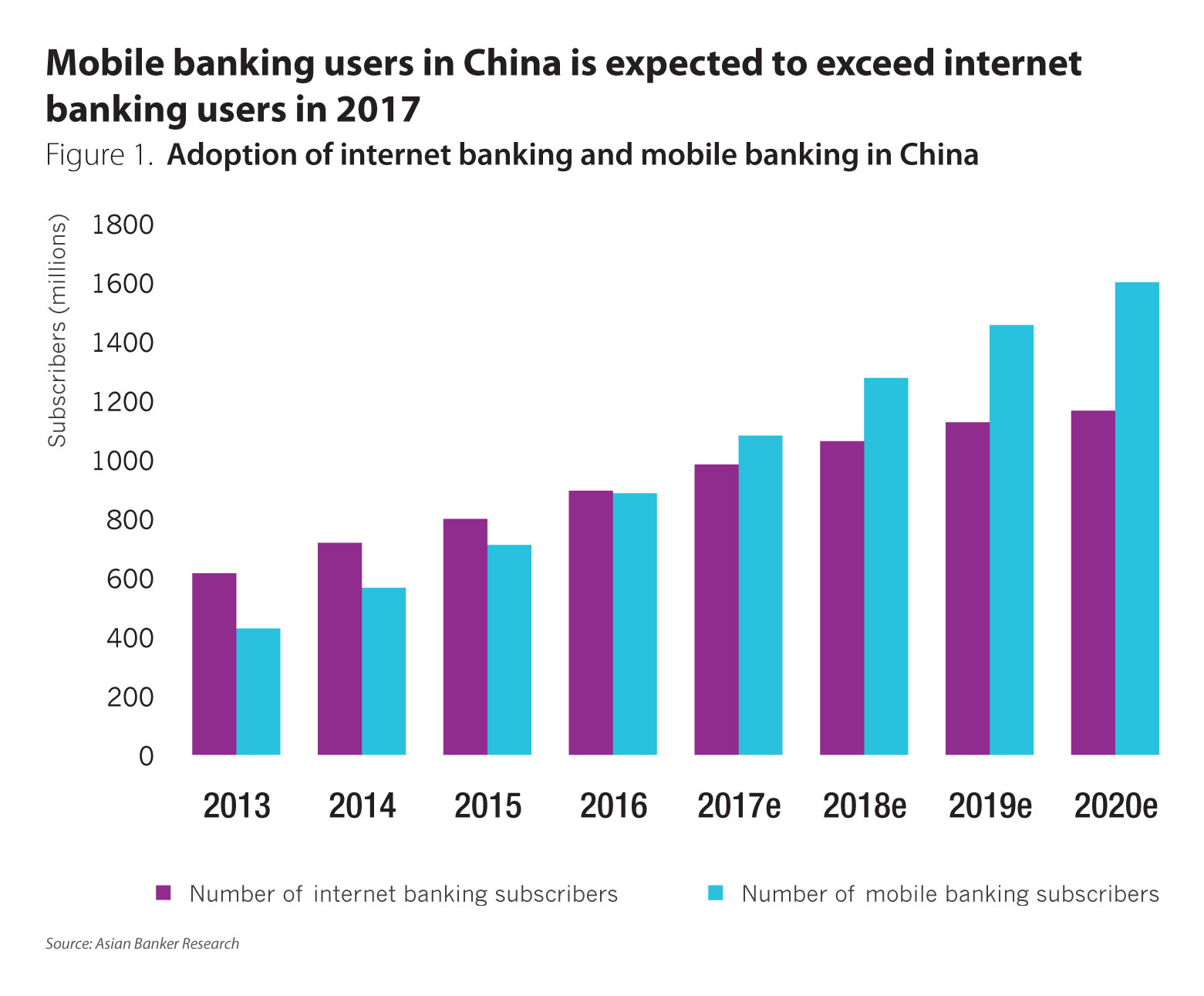

There are approximately 900 million mobile banking subscribers in China, and we expect that the number of mobile banking subscribers will exceed the number of internet banking subscribers in 2017 (Figure 1). Industry and Commercial Bank of China (ICBC) has the largest mobile banking user base, followed by China Construction Bank (CCB) and Agricultural Bank of China (ABC). Joint-stock commercial banks have seen faster growth in mobile banking users. The number of mobile banking subscribers in China Minsheng Bank Corporation (CMBC) and China Merchant Bank (CMB) surged by 65% and 39% annually between 2013 and 2016, respectively.

Digital banking is witnessing phenomenal growth in rural China. Latest official data shows that internet banking subscribers went up by 20.5% to 429 million in 2016, and mobile banking subscribers increased at a faster pace of 35% to 373 million. The volume and value of mobile banking transaction jumped by 62% and 71% in 2016, respectively. Going forward, the growth in internet banking will decelerate, as the development of new players such as third-party online payment service providers poses challenges to commercial banks.

South Korea

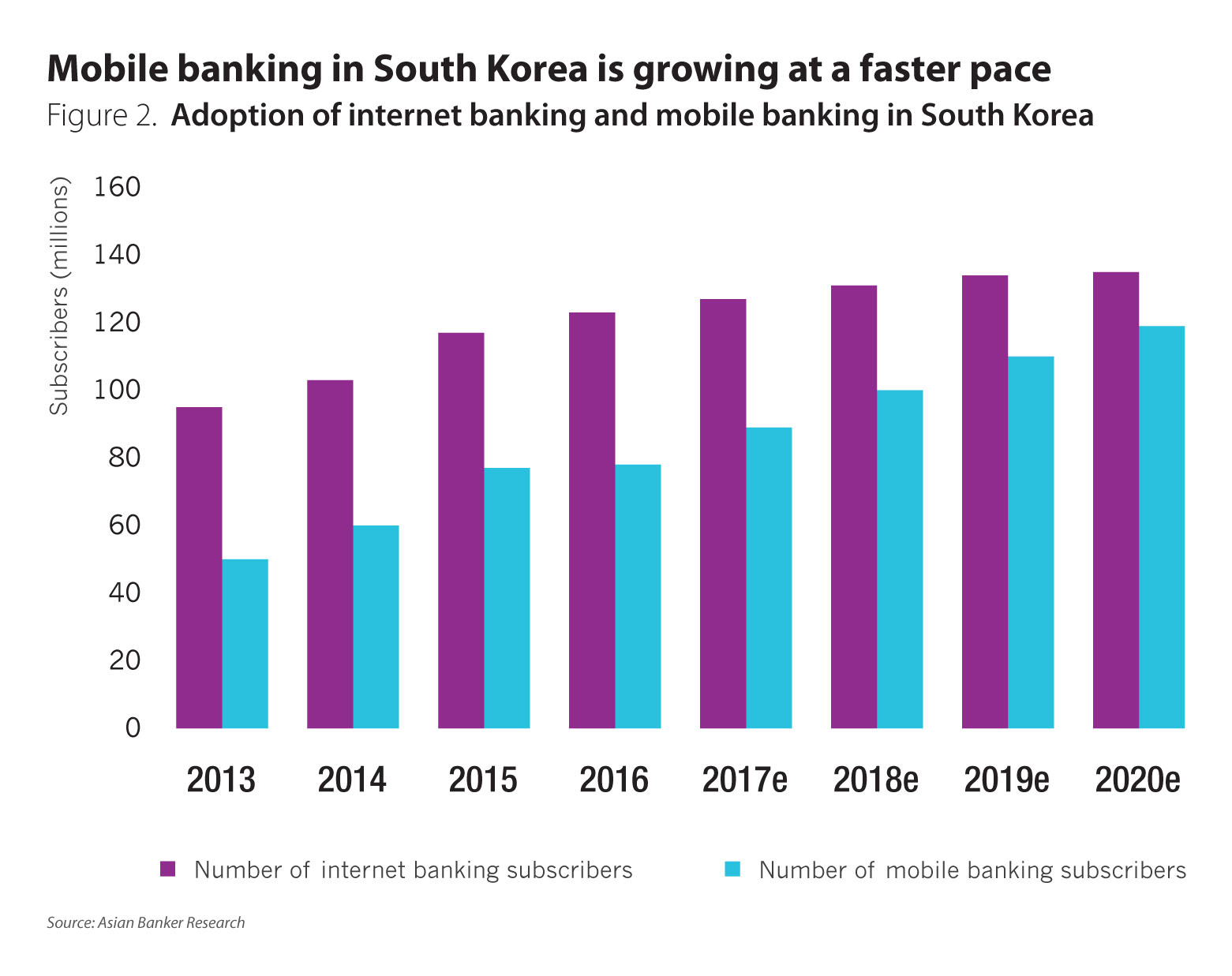

Online banking transactions are rapidly shifting from internet banking to smartphone-based mobile banking in South Korea. The country has recorded a compound annual growth rate (CAGR) of 16.2% in the number of subscribers to mobile banking services between 2013 and 2016, compared to 8.7% for internet banking services (Figure 2). Meanwhile, the number of subscribers to smartphone-based mobile banking grew at a faster 26.2% per year during the same period of time and accounted for 95% of total number of subscribers to mobile banking in 2016, up from 74% in 2013. Both value and volume of mobile banking transactions have risen faster than that of internet banking during the past few years.

South Korean banks have been closing down their branches to save costs. As a result, many older customers find it difficult to manage their finance. Concerns over security issues, a lack of digital skills, and complex identification process are the key barriers to the adoption of digital banking services. In addition, South Korean banks have launched a number of different mobile banking applications, making it hard for older customers to figure out which application they should install. Therefore, banks have tried to provide services that are tailored to their older customers’ needs. For example, Shinhan Bank and KB Kookmin Bank released a mobile banking application with bigger fonts and simpler interface for them.

Malaysia

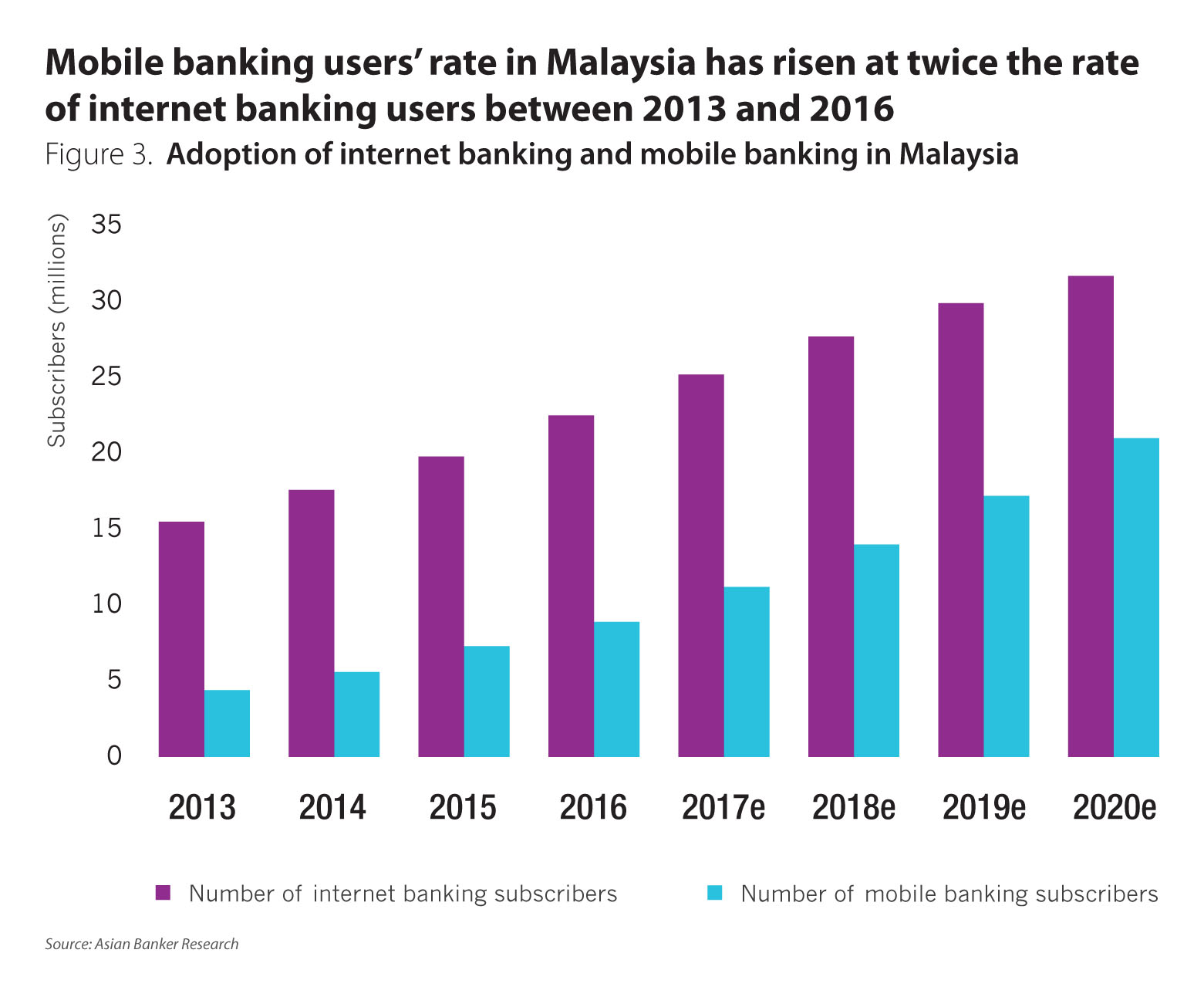

Banking transactions were predominantly done through internet banking channel in Malaysia. During the past three years, the number of mobile banking users has risen 27% per year, and the number of internet banking users have increased at a stable rate of 13% (Figure 3). Apart from faster growth in the number of users, mobile banking has overtaken internet banking in 2016 in terms of transaction volume, as consumers increasingly prefer mobile devices. Mobile banking transaction volume expanded at a CAGR of 74% between 2013 and 2016, compared to 30% for internet banking. The value of internet banking went up by merely 3% per year during the same period of time, much slower than 38% for mobile banking.

Digital banking transactions accounted for 94% of CIMB’s total banking transactions in 2016. CIMB said that they are at the first stage in their five-year journey to enhance customer experience. The bank is planning to add functionalities to its chat-based mobile banking application, called CIMB EVA (enhanced virtual assistant). This two-way messaging application between customers and the bank was launched in late 2016 for customers to manage their daily banking transactions. In addition, the bank will make further investment in data and processes to provide contextual banking services to fulfil their customers’ diverse needs.

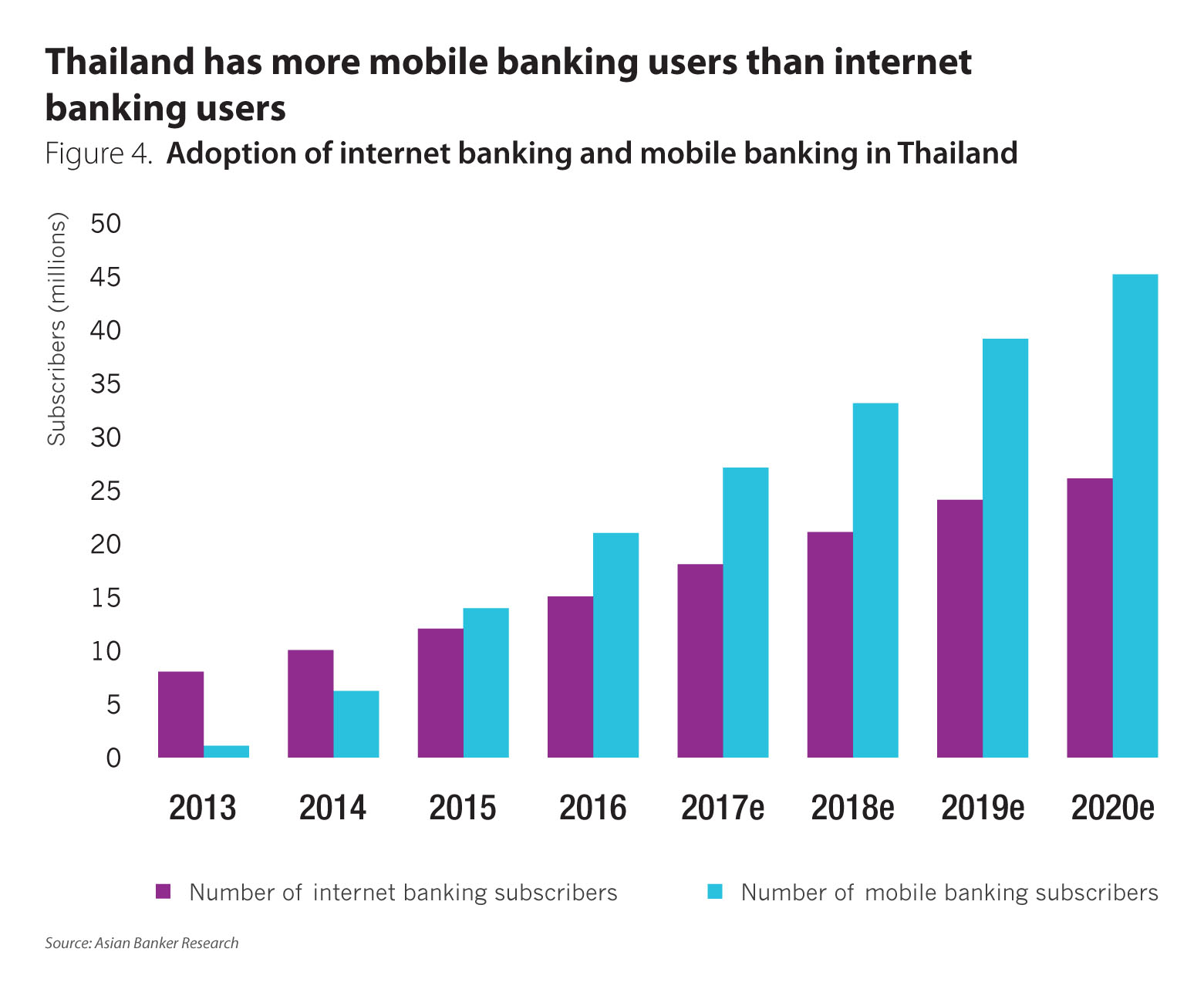

Thailand

Mobile banking transactions in Thailand have surpassed internet banking transactions in terms of volume during the first half of 2015, driven by the rising mobile penetration and various mobile applications Thai banks developed. The number of mobile banking users in Thailand also exceeded the number of internet banking users in the third quarter of 2015 (Figure 4). The country has seen a substantial jump in the number of mobile banking users, with 1.2 million in 2013 to 20.9 million in 2016. Meanwhile, the volume of mobile banking transactions registered a CAGR of 117% during the past three years to reach 585 million at the end of 2016, which was 2.4 times the volume of internet banking transactions. Mobile banking transaction value surged by a massive 87% per year between 2013 and 2016, compared to 12% for internet banking.

Thai banks are boosting investments in digital banking to maintain their competitiveness. Kasikornbank, the country’s leader in mobile banking in terms of both users and transactions, will spend $142.33 million annually to develop information technology to sustain its leading position in digital banking. The bank has also set up a subsidiary, Kasikorn Business-Technology Group, in April 2016 to work with financial technology (fintech) firms and start-ups both locally and internationally to explore technological advances.

It aims to grow the number of mobile banking users by 42% to 7.1 million and increase the ratio of digital banking transactions from 60% to 65% in 2017. The volume of the bank’s digital banking transactions is anticipated to reach 7.9 billion by 2020 and the value of digital banking transactions is projected to grow tenfold to $853 billion (THB30 trillion) by 2020.

Accelerating the move towards lower-cost digital banking

In the Asia Pacific region, consumers have been rapidly adopting digital banking despite cybersecurity concerns. Going forward, the move towards lower-cost digital banking will accelerate. In the meanwhile, mobile banking is expected to overtake internet banking in more markets in the coming years. With increased customer expectations and tougher competition, banks need to act quickly to enhance the security of digital banking channels and improve their customers’ digital experience.

.png)