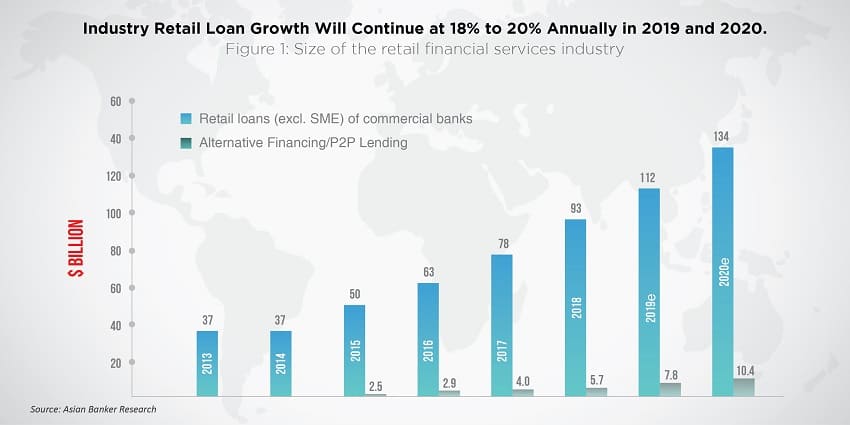

- Industry retail loan growth will continue at 18% to 20% annually in 2019 and 2020 with alternative lending and P2P will contribute 7% to 8% to total consumer loans by 2020

- Consumer finance is the key business driver but provisions in some banks have doubled since 2016

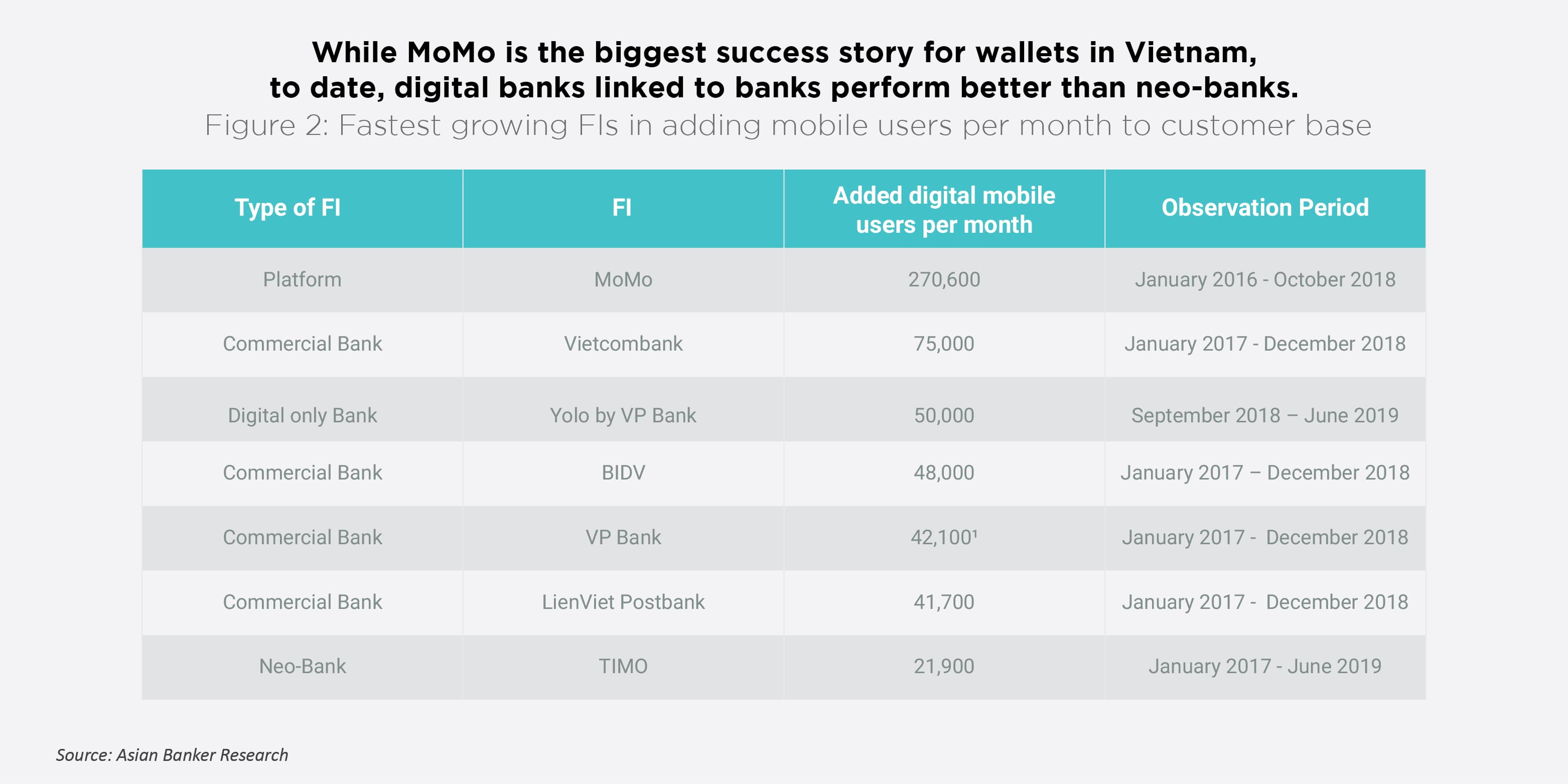

- While digital banking adoption is rapidly growing, the biggest challenge faced by financial institutions is the level of interaction with the customers

Banks in Vietnam have realigned their business towards retail financial services like no other country in the Asia Pacific has in the last eight years. The average contribution of retail income to total bank income by the top three retail banks increased from 17% in 2010 to over 50% in 2018. Banks are currently in the process of conceptualising and laying out their digital transformation blueprints.

The retail financial services market for commercial banks is expected to grow to $134 billion by 2020 and alternative financing estimated to grow from $5.7 billion in 2018 and double to $11 billion by 2020.

Consumer Finance

Key retail asset driver and the largest portfolio segment, however, is consumer finance and short term micro loans for purchasing digital devices and household appliances like mobile phone, laptop, washing machines, refrigerators, AC, TV, microwaves, and others. The sector has attracted a spate of foreign players, in particular, Koreans. LOTTE Finance officially launched in June 2018 and Shinhan Card opened Shinhan Vietnam in Ho Chi Minh City as a 100% foreign-owned consumer finance firm after having been allowed to acquire 100% of Prudential Vietnam Finance.

FE Credit, the finance arm of VP Bank is the largest consumer finance company with $2.3 billion in its loan portfolio, contributing 45% to group profit as of end 2018. FE Credit’s key products are cash loans and sales finance (two-wheeler and consumer durables loans) and credit cards. The company had over 3.8 million active accounts in 2018. The company understood early on to focus on micro-segments and tailor consumer finance around such loans for hospital workers, as well as to determine the difference between nominal and actual income allowing FE neither to overserve nor to underserve this segment. FE also took efforts to better understand the customer journey, which often begins with internet or mobile research on behalf of the client while local relationships between hospital staff and the branches in that area were supporting client relationships. The company is also collaborating with partnerships to create a sufficient ecosystem for customers as well as to attract and approach more potential customers.

Provisions however more than doubled between 2016 and 2018 and profit growth was negative in 2018 for the first time. In August 2018, as the first in the market, FE launched a 100% digital lending process via its mobile app where technologies such as optical character recognition, interactive voice response and machine learning facial recognition are applied and customers will just have to wait for the financed device to be delivered at their door.

Traditionally in Vietnam, a customer must first sign up for an installment plan online and provide basic personal information on the retailer's commercial site. A confirmation by the financer’s sales staff via phone will follow, after which, the customer is required to go to the retailer’s stores to complete the application by providing the required documents. Then the customer will just have to wait for final underwriting decision to receive the goods. With FE Credit, customers are directed to the FE Credit application page where they can fill in and complete the application by themselves then wait for underwriting decision. By deploying a Robo lending platform, it cuts down the whole lending process from 4-5 days to 5-10 minutes. In 2019, the company launched its e-signature for both online and offline processes and started its consumer finance loans on mobile application. It has also intensified its fraud detection schemes to strengthen verification stages.

Mortgages

While there is no official data on the industry mortgage volume either, the market has been growing outstanding balances from $11 billion (VND 262 trillion) in 2013 to $24 billion (VND 557 trillion) in 2018, adding $2.6 billion annually. Mortgages currently contribute 26% to total retail loans. The market is maturing among developers, buyers and investors compared to several years ago. There is also an indirect mortgage market model emerging with greater access to credit fuelled by property developers. Supply gluts will probably become evident only in high-density areas. Large inventories were launched in Hanoi and Ho Chi Minh City in 2015-2018. Housing demand and supply are currently balanced but the key will be to see whether mortgages for home ownership will tilt in the future towards investment. Now home loan purchase for ownership, renovation/refurbishment loans and loans against the property make up the biggest portion in banks portfolio. Banks have also developed the ability to price longer-term/fixed credit interest.

Car Loan Market

The car loan industry is firmly in the hands of dealers with most banks who only engage indirectly with this business. Banks do not consider automobile lending a strategic portfolio and most stay away to increase their book due to the current risk profile and low margins Truong Hai Auto (THACO) currently holds one the largest market share in Vietnam’s automobile market in recent years. In tying up with particular car dealers, banks have to offer specific packages tailored to the dealers’ customer segments and are required to offer up to 96 months of tenure and loan to value ratios of 85% for the most popular car brands, such as Japanese and Korean cars in order to obtain a tie in.

Digital transformation in the retail financial services sector

Between 2017 to 2018, banks enhanced existing functionalities with add-on criteria improving the user experience, including the implementation of new mobile and internet banking platforms with a service-oriented architecture and improved security based on multi-factor authentication. Most app offerings on banks’ mobile platforms are still undifferentiated and cover essential payments and financial services information. Out of six key categories, which a mobile platform offers – including payments, ease of use, security empowerment, financial fitness, customer service, and account opening payments – payments and ease of use are the most developed ones for Vietnamese banks. While personal financial management and spending categorisation through data aggregation, viewing accounts of other financial institutions (FIs), setting of spending limits and restrict payments to certain types of retailers or locations, loan repayments, financial investments, full current account opening, cheque imaging or in-app messaging with live representatives have not yet emerged. Banks have begun to adopt the strategy of all-in-one application to attract more users, ranging for instance, from house-maid service to human resources solutions. A few players stood out from the crowd.

Vietcombank refreshed its app in 2017 and was able to double its user numbers to 2.6 million as of end 2018, becoming one of the most used mobile banking applications. Since August 2018, Vietcombank deployed another application on its platform VCBPAY, to offer better payment utilities to customers such as booking and paying for airline tickets, movie or hotel tickets within the app and to send gifts to friends, send money request to friends and to temporarily lock and unlock cards, register/cancel online payment via cards. Log in to the mobile app is via fingerprint and facial recognition.

YOLO by VP Bank is the first digital bank operating on the Amazon Web Services cloud, allowing them to grow rapidly in both quality and quantity of users. Between its launch in September 2018 and June 2019, YOLO reached more than 500,000 registered users, though it is not quite clear what portion of it is new to bank customers. It offers online insurance packages without requiring a medical examination. In particular, users can schedule a home check-up through YOLO's partner system and ask doctors about medical issues through the ViCare community in-app. New bank customers can register to open a virtual prepaid card (non-KYC account) with just their email and phone numbers with free insurance and no annual fee and can upgrade to a full know your customer (KYC) current account with lending options. The platform also offers recharge, bill payment and money transfers. Other features include split bill, auto-pay, future pay, international tuition payments, QR payments, transfer and loyalty points and cashback accounts.

While rates in financial inclusion and mobile payments adoption are multiplying, the biggest challenge faced by FIs is the level of interaction with the customer. Active rates for wallets and mobile banking usage ranges on average between 20%-30% measured on a three-month cycle, indicating that for most players, active rates are still below the one million users. In particular, banks hope to connect to the ecosystem of external services to increase engagement. In this context most e-wallets focusing on payments are loss-making entities, while banks continue to be the biggest economic beneficiaries. Stand-alone neo-banks such as Timo have not made any impact, partially due to the absence of a comprehensive electronic know-your-client (e-KYC) framework though we believe the regulator appears to be open to e-KYC and digital verification. Looking deeper into Vietnam’s digital banking models, some digital banks are not really digital for they digitalise the user interface but still use the core technology systems of traditional banking.

Technology and infrastructure investment by commercial banks

Going forward, the period from 2019 to 2022, banks will pursue the launch of full digital banking blueprints making more structural changes at the back office such as institutionalising an independent digital banking centre which will centralise all departments in regards to digital alignment and operations. The focus will also be on cloud-based initiatives, updating the management information system (MIS) architecture, upgrading enterprise content management and customer relationship management systems as a foundation for seamless multi-channel customer interactions and sales. Banks we have spoken to are keen to upgrade component projects such as loan origination system for business customer, loan origination system for retail, customer relationship management (CRM) and enterprise content management. These projects play an essential role in the process of customer service, customer information management and digital data.

Banks have not yet offered a fully straight through current account opening process via mobile devices, but leading banks are already testing and are going to deploy likely by end of 2019/2020. Banks have also streamlined their account opening processes at the branch which continues to be heavily manual. While most banks are currently investing in digital transformation of customer-facing systems, much of the supporting back-office legacy systems lack the flexibility to enable its front-of-house operations to meet customer expectations going forward. ACB became one of the first banks in Vietnam to set up a robust cloud-based enterprise resource planning to improve the customer experience whereby core banking is shifted in conjunction with the construction and investment of the multi-channel management system. By moving key areas including finance, procurement and project expense management to the cloud, ACB was able to improve productivity and controls. The bank also began digitising the front line, equipping relationship managers with its cloud-powered mobile CRM app.

Vietnam’s developing fintech ecosystem

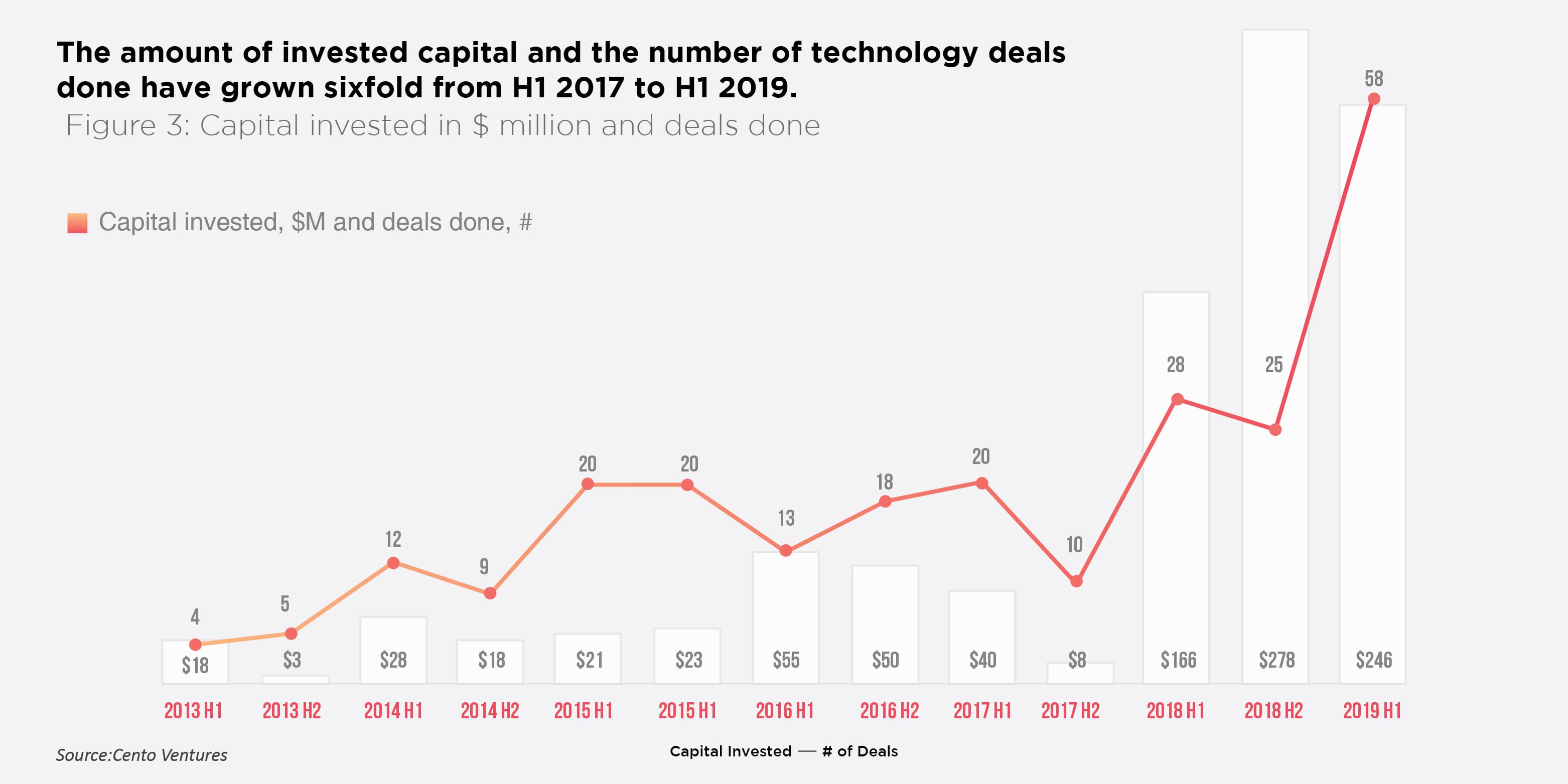

Since 2017, a more connected ecosystem of fintechs and larger financial incumbents are emerging. Viettel and VPBank were the first to funnel capital into the development of start-ups. By 2019 VinGroup and Asanzo have joined the fray with committed capital of at least $14 million, according to Cento Ventures.

More banks launched national hackathons in 2018 to encourage co-creation between staff and tech community to develop a digital solution to solve real banking problems through open banking. The objective is to accelerate an innovative culture within banks, crowdsource for digital solution to address customer pain points and position banks for the future.

The government wants to develop frameworks in specific fintech areas but has yet to address peer-to-peer (P2P) lending and concrete parameters for the national payments framework. The regulator voiced that the P2P lending industry, which generated loans of approximately $5.7 billion in 2018, should be formalised beginning 2019. The regulator will allow a pilot implementation of P2P lending before officially developing a regulatory framework. P2P lending companies would not be allowed to mobilise capital but will only act as intermediaries to connect lenders and borrowers, according to a report by Vietnam News.

It is important to note that since 2017, Vietnam jumped from the second least active startup ecosystem among the six largest ASEAN countries into the third most active, trailing behind only Indonesia and Singapore, taking a share of 17% among six countries in ASEAN, compared to 5% in 2018 and 2% in 2017, according to Cento Ventures.

Vietnam startups raised a total of $246 million in H1 2019 but the investment was highly uneven. The retail and payments/remittance sector took 57% compared to 4% for general financial services, according to Cento Venture. The three largest investments (Tiki, VNPay and VNG) captured 63% of the funding.

.png)

.webp)