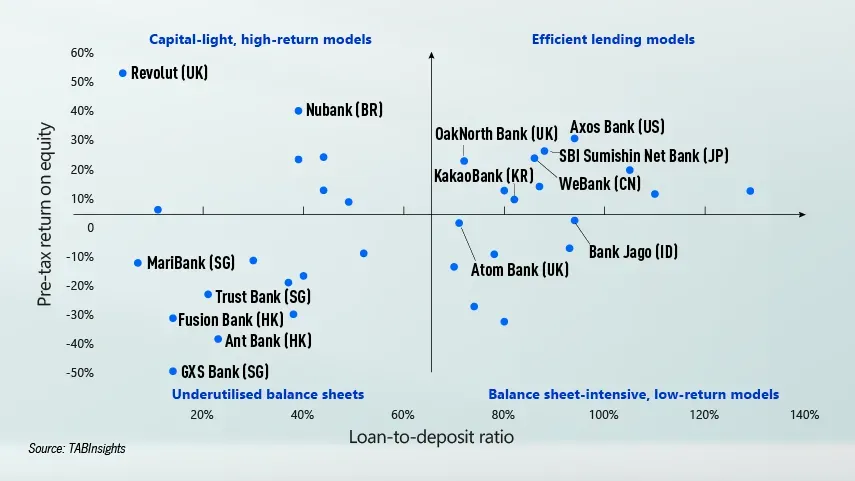

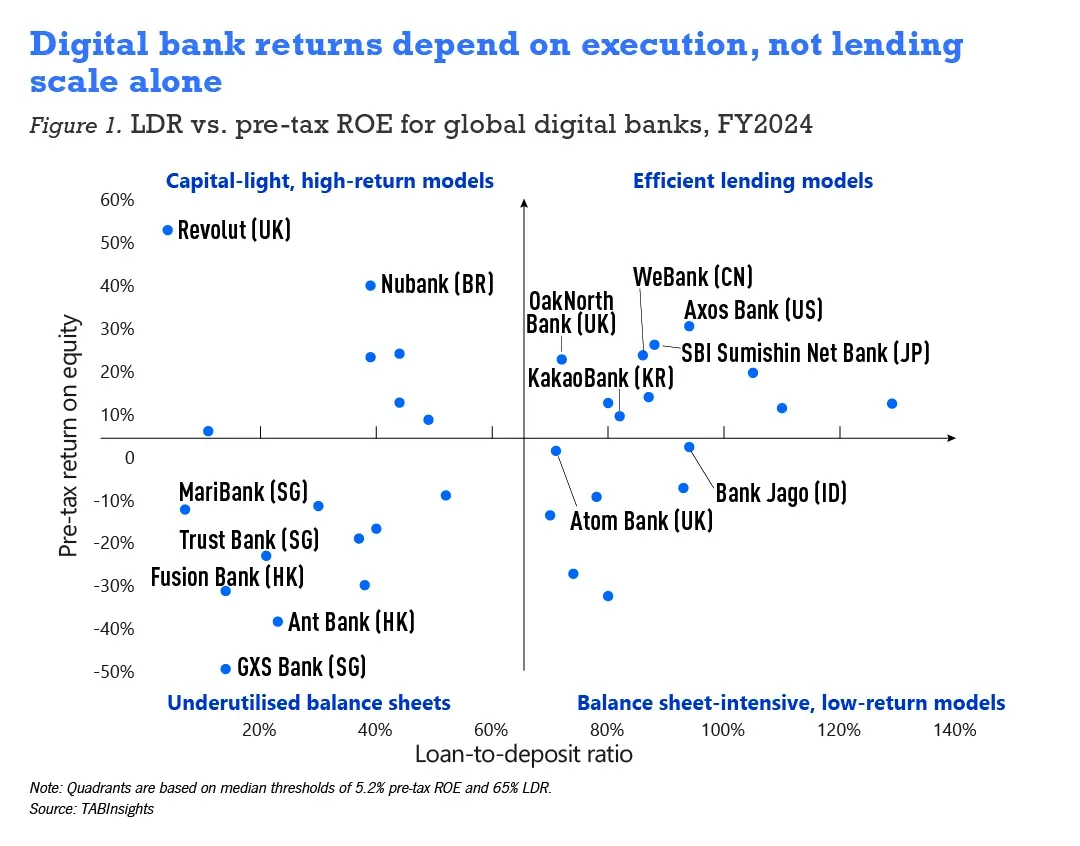

The relationship between lending scale and profitability in digital banks is not linear. Analysis of 100 digital banks across major markets shows that high loan growth does not guarantee returns, and low lending does not necessarily indicate underperformance. Outcomes depend on execution, business model and monetisation strategy rather than balance sheet size alone.

Using median thresholds of 65% loan-to-deposit ratio (LDR) and 5.2% pre-tax return on equity (ROE), digital banks fall into four distinct groups.

Banks with low LDR and low ROE are typically early-stage or structurally constrained. Many are still building credit pipelines and risk frameworks. MariBank, GXS Bank and Trust Bank reported LDRs below 25% in 2024, while Fusion Bank and Ant Bank remain below 30%. Limited lending and high operating costs continue to weigh on profitability.

High LDR alone does not translate into strong returns. Bank Jago reported an LDR of 94% but generated only 2.1% pre-tax ROE, while Atom Bank achieved profitability with pre-tax ROE of 1.2%. These banks have built lending scale, but returns remain constrained by underwriting, pricing and cost structure.

The strongest performers combine high LDR with disciplined execution. Axos Bank, OakNorth Bank, SBI Sumishin Net Bank and KakaoBank convert lending into sustained returns through focused customer segments, pricing discipline and cost control. In this segment, average pre-tax ROE reaches 13.7% with LDR close to 100%.

A second group of top performers achieves high returns without relying on lending intensity. Revolut and Nubank deliver strong pre-tax ROE with LDR below 65% by monetising payments, subscriptions and ecosystem activity. Their performance shows that diversified, fee-based models can outperform balance sheet-led strategies.

The divergence across these groups highlights two viable paths to profitability: disciplined scaling of lending or effective monetisation of customer activity. Banks that grow lending without execution discipline fall between these models and struggle to generate returns.

For digital banks still building their franchises, the trade-off is clear. Pushing LDR without strong underwriting and cost control risks weak returns, while delaying lending expansion requires alternative revenue models. Execution, not lending growth alone, determines outcomes.

View the full World's Top Digital Banks rankings here.

Download the full Databook of the World's Top 100 Digital Banks.

.png)

.webp)