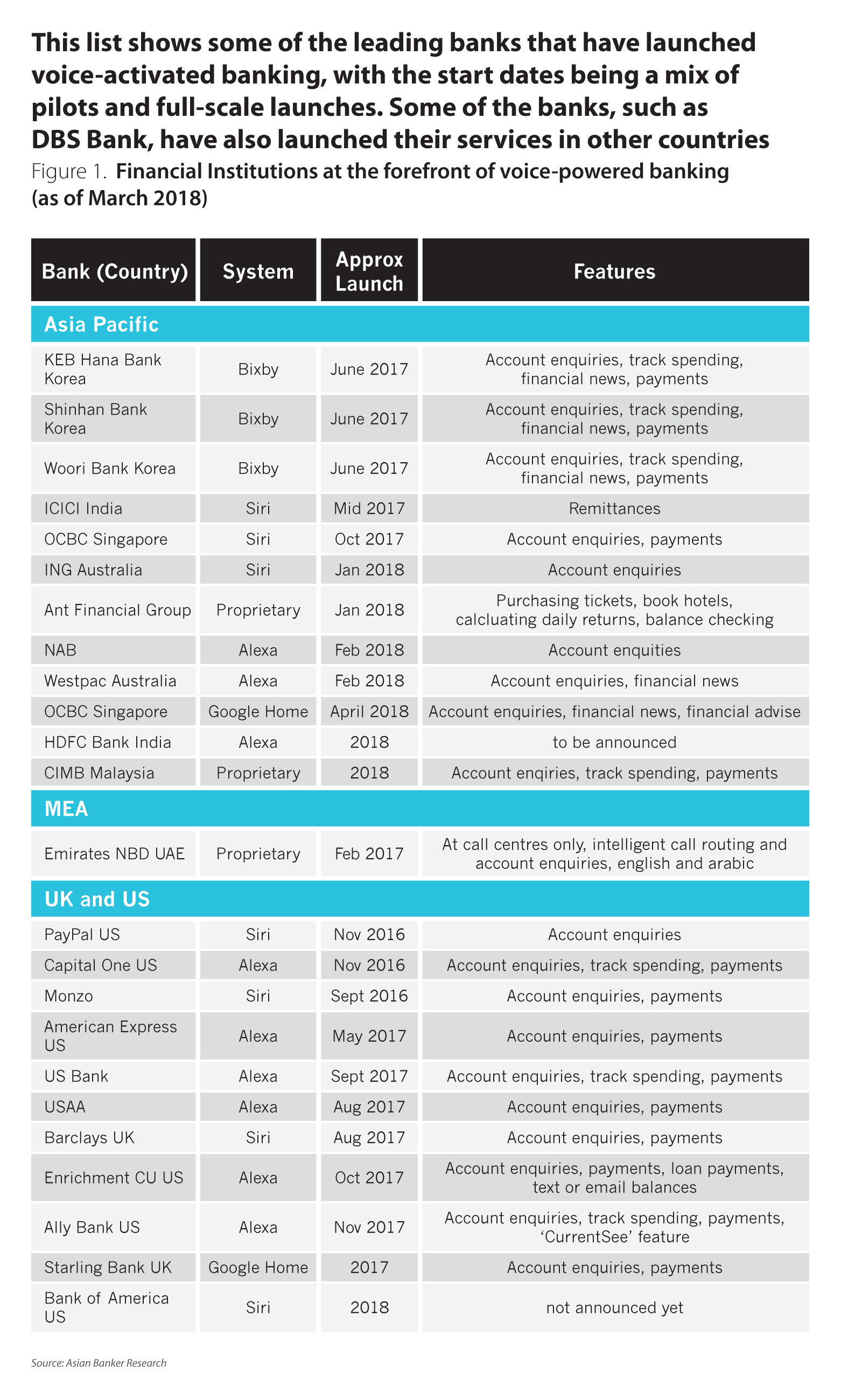

- Banks have launched voice-activated consumer banking as early as 2014, which has slowly taken off around the world

- Voice-enabled assistants have been a part of consumers’ everyday lives with users becoming more accustomed to using voice commands for simple tasks such as getting directions or placing a call

- Banks must ensure they have the network and data infrastructure to support such solutions

2018 has been described as the “year of voice-activated banking”, with more consumers using Alexa and other voice services for daily banking. Artificial intelligence (AI) and machine learning will soon enable more sophisticated voice-led services. While Alexa is in the lead, services such as Siri are growing quickly as well.

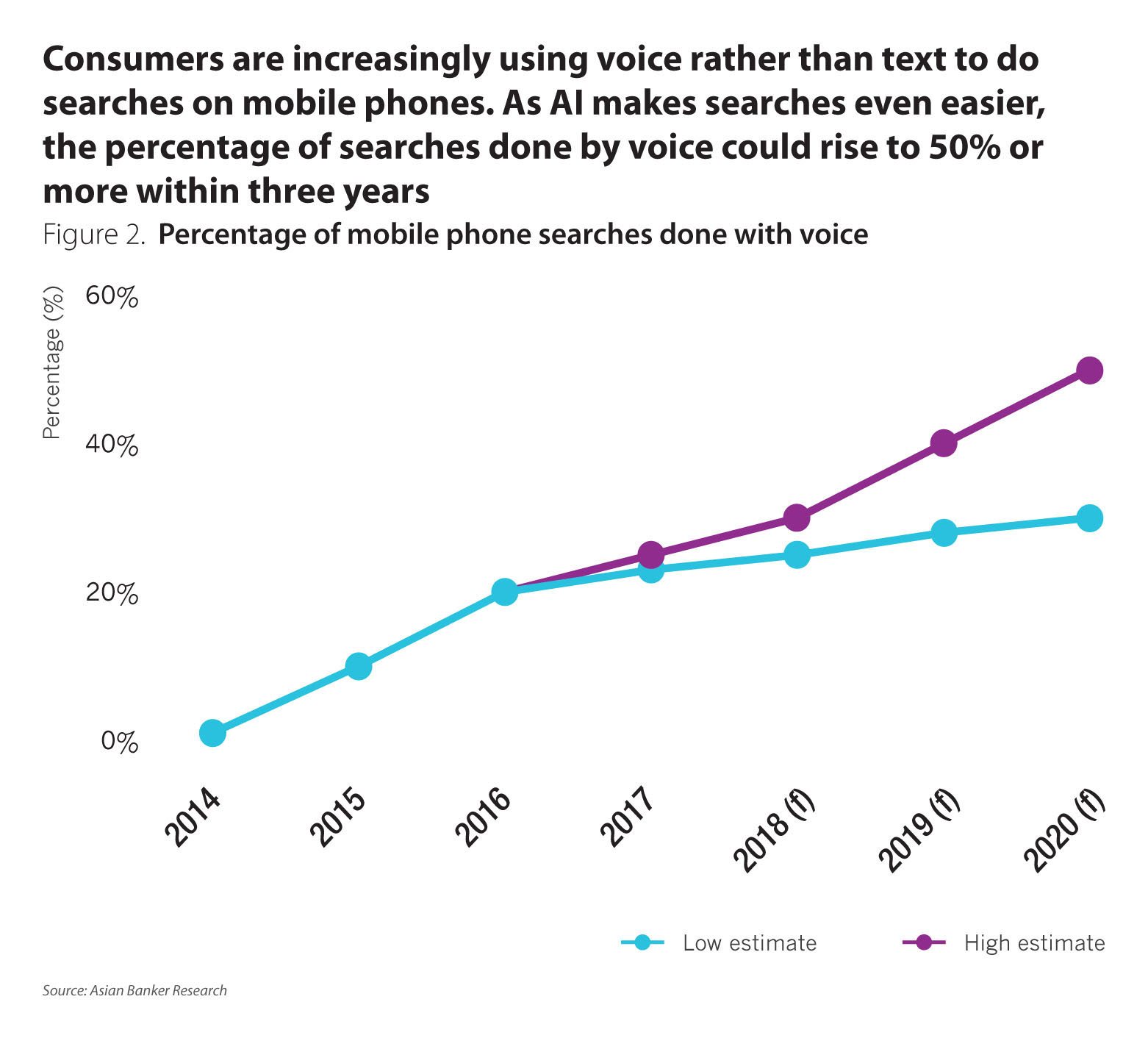

Consumers already use voice for 20% of their Google searches now and are likely to use it for 50% within a few years, so they are starting to expect banking by voice too. While a growing number of banks are offering voice activated services, they will need to enhance the current versions with artificial intelligence and more to deliver the value consumers want.

Voice-led banking gains momentum

Banks have launched voice-activated consumer banking as early as 2014. And since then, voice banking has slowly taken off around the world (Figure 1).

One of the first was ING Netherlands, which used Nuance’s voice-recognition software to launch Inge and allow customers to use voice commands for their banking. Consumers could ask where the nearest branch was, for example, or pay someone in their contact list.

Capital One went further in 2016 when it launched a service using Amazon’s Alexa and it is still among the most advanced, with services including credit card payments, account balances and getting a snapshot of spending. USAA, Ally Bank, US Bank and others followed in 2017 and launched services using Alexa.

Banks in Australia largely waited until 2018 to get into the game and then piled in quickly. National Australia Bank (NAB) enabled customers to request their account balance or details about deposits, for instance, by asking Alexa. Jonathan Davey, executive general manager, NAB, said “this is NAB’s first step. In the future, we certainly see this experience turning into one where you can pay bills, make funds transfers or even purchase items.” Westpac similarly announced in January 2018 that customers would be able to access services with Alexa.

There are other options as well. Barclays used Siri, for example, to launch its voice banking in August 2017 and enable customers to pay existing payees or mobile contacts without opening the banking app or inputting passwords.

Some banks have taken a different tack and developed their own applications. Bank of America, for instance, launched its own digital assistant, “Erica”. In Europe, Santander allows UK customers to use its app to make payments by voice. And Commonwealth Bank of Australia (CBA) launched “Ceba”, a chatbot which recognises about 60,000 different ways customers can ask for 200 banking tasks, from activating cards to making payments.

Why voice-led banking is growing

The reasons for the rapid growth in voice-led banking are easy to see. Voice-enabled assistants ranging from Amazon’s Alexa and Apple’s Siri to Baidu’s Xiaoyu and Alibaba’s Genie are becoming part of consumers’ everyday lives, so consumers have become accustomed to using voice commands for simple tasks such as getting directions or placing a call. Google estimates that more than 20% of searches happen by voice already and, as the graph below indicates, some observers expect consumers to use voice for more than half of their searches by 2020 (Figure 2).

As the quality of voice-activated services expands, consumers are doing far more with voice commands. They’re already listening for recommendations instead of reading them and using voice instead of a buy button, for example, as well checking account balances and payment due dates without logging in to internet banking. The result is that voice-based services are affecting consumers’ purchase decisions, making them extremely powerful.

What banks are trying to achieve

A majority of bankers agree that voice will be the most important channel for their business after mobile, and they are looking at 2018 as a pivotal year.

“We believe that conversational user interface is a new paradigm to connect to banking products and services,” said ZorGorelov, chief executive officer (CEO), conversational AI provider Kasisto.

Using natural language for automating routine support tasks, for instance, means that voice-led services have the potential to replace much of the work of bank call centres and drive down costs as well as to speed up calls. Banks can also use voice to offer new services such as accessing budgeting, managing loan payments, tracking goals for saving and participating in workshops.

While voice-led banking offers benefits, bankers are still looking for insights into how people will use it in the future. Whereas people use laptops for complex interactions and smartphones for quicker interactions, voice-based service patterns are still evolving.

Technology development is critical

To put voice-led banking in place, banks need to develop greater capabilities – or risk falling behind. Bank tactics so far have included buying solutions, partnering, acquiring a service provider, or internally developing their own software.

The prevalence of personal and home assistant software on smartphones mean that banks can often find cheaper and better options by using Alexa or Siri than developing their own solution. For now, Alexa is in the lead, due in part to the popularity of Echo and other Amazon devices. Amazon has also opened its APIs, enhanced the skills of its devices, and provided developer tools.

Likewise, Siri is starting to gain a foothold, with early users including PayPal, Venmo and Square. UK challenger bank Monzo, German direct bank N26, and the Royal Bank of Canada also offer payments with Siri.

Google Home is evolving as well and introduced increased sophistication when it launched analysis of voice harmonics, which allows it to recognise five different voices on one device.

Companies with AI-powered speech recognition that don’t yet have their own devices, such as Nuance and Personetics, are jumping into the game as partners too. Nuance powers voice-led banking in apps at banks including USAA and Santander, while Personetics powers Ally Assist.

Taking a different tack, TD Bank acquired AI start-up Layer 6 AI and is collaborating with the Vector Institute for Artificial Intelligence to develop next-generation AI technologies. TD also signed an agreement with Kasisto to integrate its platform into TD's mobile app and collaborated with Amazon to introduce voice banking using Alexa.

USAA similarly bought an AI platform, Clinc, to provide human-like conversations. Clinc can extract context and intent from natural language rather than just converting speech to text and finding answers from preprogrammed responses, so the experience feels more like an intelligent human interaction, while some banks are doing the development internally. NAB Labs, for instance, developed the bank’s solution by itself.

Regardless of how they develop their solution, artificial intelligence will become essential for banks to increase revenue, lower costs, reduce risk, deliver better experiences, and gain a competitive edge. Machine learning is also critical for enabling voice assistants to learn from every customer interaction, relate it to the current context and provide relevant advice.

Key success factors for voice-activated banking at leading banks include:

- Help customers ask the right questions by guiding them in the bank’s marketing to ask specific questions which Alexa can answer, such as “what is my balance” or “what are my latest transactions”

- Always provide customers with an answer – while they will provide clarification of a request, they are less far less likely to accept an error message

- Start with simpler features, such as balances or branch location, then, similar to how Amazon notifies users of new functions for Alexa devices, regularly notify customers of new voice functionality

- Realise that even though Initial voice launches are simplistic, financial conversations are actually several questions deep - think of the platform as driven by conversation rather than interactions

- Rather than tying Alexa to a single device such as an Echo, which would limit how customers can interact, use anytime-anywhere engagement on a multitude of Alexa-powered devices

- Make it easier for customers to perform tasks or access information by recognising their voice

Unless they develop what their customers need and quickly integrate voice services into consumers lives’, KPMG noted, retail banks could become largely invisible to consumers. Customers already trust tech companies such as Amazon more than their primary bank.

Bumps in the road

In most markets, regulators have placed few barriers in the way of voice-led banking. Banks in the US, China, and Singapore, for example, offer voice-activated banking that consumers use to make payments and perform other transactions. Samsung’s Bixby is becoming so integrated with South Korean banks that consumers there could soon stop needing dongles.

Europe is, however, a different story. Alexa is reportedly not allowed to handle transactions there and Amazon has not enabled transfers or information on accounts. While Amazon has not said why Europe is different, observers speculate that it could be due to Payment Service Directive 2 (PSD2). Moreover, banking security standards from bodies such as the European Banking Authority and FFIEC require multi-factor authentication for transactions, which usually means dongles or passwords. While banks could integrate voice biometrics into two-factor authentication frameworks, requiring another method such as a password seems unlikely to change soon and could hinder the adoption of voice-led banking.

Other observers believe Amazon could be setting up its own voice banking system and wants to make sure that it provides the best system.

Case Studies

Westpac (Australia)

“Voice-based interactions give us a more personal interaction with our customers and one that is seamless,” Travis Tyler, general manager, Westpac Consumer Digital said. “It allows them to fit us into their lifestyle and bank with us when convenient.” Westpac works with a range of partners to deliver new products and services to more than 4.5 million digitally active customers. “Alexa has had great success overseas, particularly in the US,” Tyler said, “so it is exciting to be working with Amazon to develop this technology.”

The Westpac Banking Skill is a cloud-based feature available through voice technology, Tyler explained. The Westpac Digital Labs team worked hard to ensure the services are safe. “When customers set up the Westpac Banking Skill, they are also prompted to set up a 4-digit passcode, which they provide before Alexa responds to questions about their Westpac accounts. Further levels of security will need to be enabled as additional features become available,” Tyler stated.

Westpac Live customers can use voice banking to check their account balance, recent transactions and reward points, and to listen to the Westpac daily financial news. “I see it (Alexa) having broad appeal relevant to all ages due to its simplicity and ease of use. Millennials will be interested as they are fast adopters of new technology, but we also think there will be interest from a wide range of our customers, including those who want to use voice-activated tasks to help with their everyday lives."

BBVA

Two or three aspects will drive the availability of voice-assisted banking, said Derek White, global head of customer and client solutions at BBVA. One is the availability of APIs, as services such as Alexa depend on them. The greater barrier to adoption, he said, will be customer behaviour and customers trusting a new form of interaction with their money. “The critical thing to remember is people have invested up to 30% to their week to earning their money. They want to make sure the interaction is safe and secure, and they’re not going to lose it. Trust needs to be built in a new medium.”

Consumers will increasingly be able to do more by voice. At this time, consumers can move money within the bank and to parties they have already established. Acquiring new products and services are a possibility in the future. But it’s still relatively early, White said, so voice-assisted banking is not bringing down volumes in the call centre yet. What it is doing, though, is adding to the number of interactions in a positive way. “People are happy with the experience.” And in a surprising twist, the BBVA chatbot in Turkey has even received marriage proposals by voice.

The implications for banks

While more and more banks are rolling out voice-led banking, services are in many ways still in their infancy. While there is clearly a cost for developing voice-activated banking, it can also reduce the need for people in branches and contact centres, which can reduce staffing expenses and increase customer satisfaction. The more that customers get used to voice-activated channels and use them, the more banks can invest in improving digital channels.

Banks will need to ensure they have the network and data infrastructure to support such solutions, though, because customers might stop using the new technology if they encounter a bad experience. Experts also note that early-mover advantage is particularly important with AI, since its effectiveness grows exponentially with the volume of data it gathers.

Although the focus has been largely on delivering more services, banks also need to focus on security. Some banks are starting to work on biometric identification, for instance, which offers the additional assurance customers need. They can also offer services that enrich customers’ lives, such as educational videos on topics such as financial literacy.

The future of banking, then, is about engaging with customers in the digital ways they expect and delivering the services they demand. Voice-activated banking can be expected to soar well above 50% before long, with consumers transacting by voice at home, at work and even in their cars. The key to success will be supporting customers by multi-channel services, especially including voice, wherever they may be.

.png)

.webp)