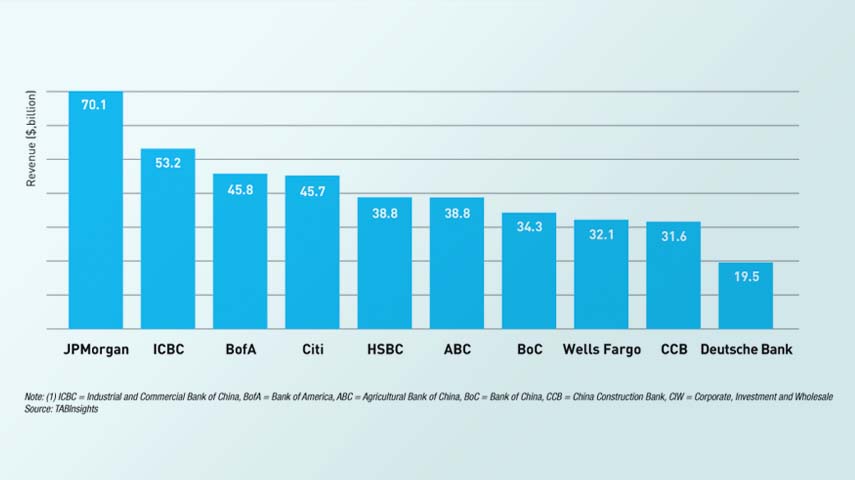

JPMorgan Chase, Industrial and Commercial Bank of China (ICBC) and Bank of America (BofA) recorded the highest revenue in corporate, investment and wholesale (CIW) banking in the financial year (FY) 2024, according to the TABInsights World’s Top 50 Corporate, Investment and Wholesale Banks Ranking 2025. The top 10 also includes Citi, HSBC, Agricultural Bank of China (ABC), Bank of China (BoC), Wells Fargo, China Construction Bank (CCB) and Deutsche Bank.

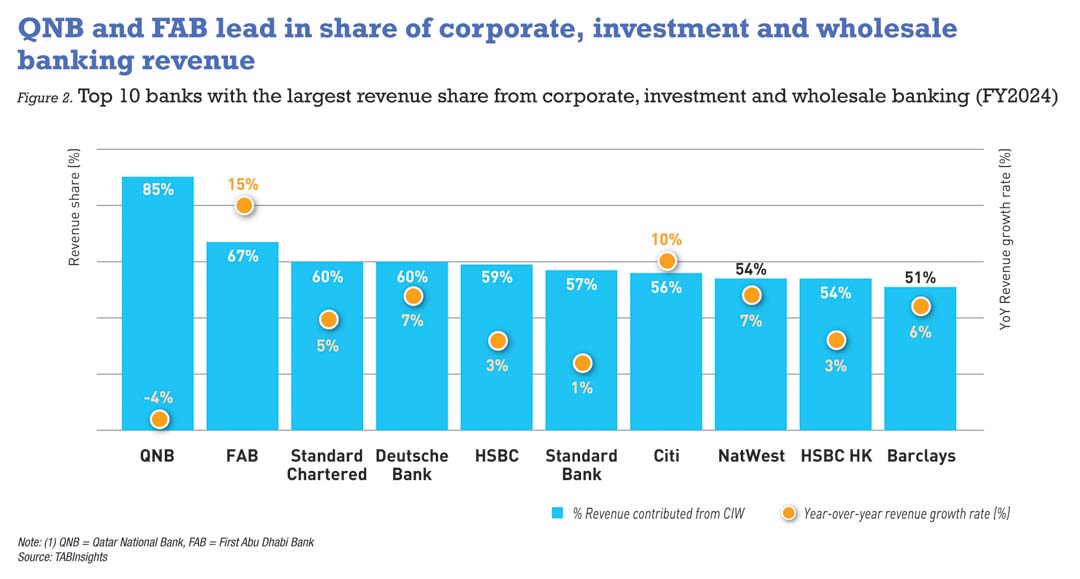

Qatar National Bank (QNB) tops the list of banks with the highest proportion of CIW banking revenue, with 85% of its total revenue generated from CIW activities. It is followed by First Abu Dhabi Bank (FAB) at 67%, while Standard Chartered and Deutsche Bank each record 60%. HSBC, Citi and NatWest also rank among the top 10.

JPMorgan, ICBC and BofA lead in revenue

Serving clients in nearly 160 countries, JPMorgan reinforced its leadership in CIW banking by generating $70.1 billion in revenue from the segment in 2024. This position is supported by its extensive global network, ongoing investment in technology, regulatory expertise and targeted acquisitions. Its CIW banking revenue rose by 9% in 2024, following a compound annual growth rate (CAGR) of 3.2% from 2020 to 2023.

ICBC follows closely, with CIW revenue reaching $53.2 billion in 2024, reflecting a modest 0.1% increase after a 1.8% contraction in 2023. The other three major Chinese banks also reported moderate revenue growth trends. ABC posted a 2.7% increase in 2024, partially offsetting a 2.2% decline in 2023. BoC saw its CIW revenue fall by 5.9% in 2024, following strong growth of 17.3% the previous year. CCB experienced an 8.4% decline in 2023, followed by a further 4.6% drop in 2024. The bank’s modest pre-tax return on assets (ROA) of 0.6% underscores the need for performance enhancement in its CIW banking segment.

BofA, on the other hand, posted stronger CIW revenue growth of 9.8% in 2023 and 3.3% in 2024, reaching $45.8 billion in 2024. However, it operates with a high cost-to-income ratio (CIR) of 56.3%, suggesting room for improved cost control despite its global footprint spanning 38 countries. Citi also saw strong CIW growth, with its growth rate accelerating from 0.2% in 2023 to 10.2% in 2024.

Among the top 10 banks with the highest CIW revenue, Citi reported the highest CIR at 61.9%, indicating the need to better manage operating expenses and improve resource utilisation. In contrast, Chinese peers such as CCB and ICBC, with a CIR of 39.4% and 25.7% respectively, demonstrate more efficient cost structures, reflecting both scale advantages and tighter cost discipline.

CIW drives revenue for QNB, FAB and key European banks

Half of the top 10 banks with the largest revenue shares from CIW banking are European institutions, with Standard Chartered, Deutsche Bank and HSBC standing out as key players. Standard Chartered, Deutsche Bank and HSBC each derive a similar share of revenue from CIW activities at 60%, 60% and 59%, respectively. These banks stand out for their broad range of CIW banking products – an advantage in both product variety and client engagement. This comprehensive offering positions them as prominent players in the global CIW banking market.

QNB and FAB from the Middle East reported the highest CIW revenue shares among the top 10 banks. Based on domestic operations, CIW accounts for 85% of QNB’s revenue, while FAB derives 67% in 2024. Their positioning as international trade hubs, alongside government-backed initiatives to promote digital payments, investments in technology and economic diversification has been instrumental in driving this growth. FAB recorded CIW revenue growth of 14.8% in 2024, with a CAGR of 17.8% from 2020 to 2023.

In comparison, American banks such as JPMorgan and BofA derive a smaller portion of their revenue from CIW at 39.5% and 44.7%, respectively. Asian banks show varying degrees of CIW revenue contribution, with several institutions working to expand their CIW portfolios and strengthen their presence in this segment.

Asian banks closing the gap with American giants

Asian banks are steadily making strides, gradually closing the gap with their American counterparts. While JPMorgan and BofA remain dominant in the sector, the growing influence of Chinese and other Asian banks indicates a shift in the global banking landscape.

Twelve banks globally had CIW banking assets exceeding $1 trillion as of FY2024, with ICBC, CCB, ABC and BoC ranking as the four largest, highlighting their scale and Asia’s growing influence in global CIW banking. ICBC, with 48.6% of its revenue derived from CIW activities, remains a key player. Despite slow growth in CIW revenue, it delivered a solid pre-tax ROA of 1.3% from these operations.

Other Asian banks are also gaining momentum. A standout performer is United Overseas Bank, which has shown robust growth with 47.1% of its revenue derived from CIW. The bank also maintained a strong pre-tax ROA of 1.8%, positioning itself as a rising force capable of narrowing the gap with leading American giants. Additionally, institutions such as Mizuho Bank are capitalising on Japan’s prominent role in global trade to strengthen their positions. HSBC Hong Kong, with CIW revenue of $18.4 billion, further boosts the growing influence of Asian players.

With solid performance and strategic positioning, these banks are well-placed to narrow the gap with American financial institutions in the coming years. As Asia’s economic influence continues to expand and the region becomes increasingly central to global trade, Asian banks are poised to shape the future of global CIW banking.

.png)

.webp)