The asset quality of Australian banks showed steady improvement in 2014, along with a reduction in banks’ domestic impaired assets, particularly in commercial property loans as a result of a strong recovery in commercial property prices. The decline in banks’ impaired business assets has led to an improved risk profile of their business loan portfolios, with the share of major banks’ probability of default in corporate exposures decreasing over the four years leading up to June 2014.

2014 saw a resurgence in domestic lending. Housing credit expanded at an annualised rate of around 7% over the six months leading to July 2014, while investor credit strengthened by nearly 10%. Business credit growth also picked up, accompanied by stronger price competition in some loan markets. Banks need to exercise caution in risk management and financial stability so as not to adversely affect lending standards in the face of revenue pressures. They also need to be careful in their property valuations as the risk of extending loans at constant loan-to-valuations ratios rises when property prices rise, as in the current climate.

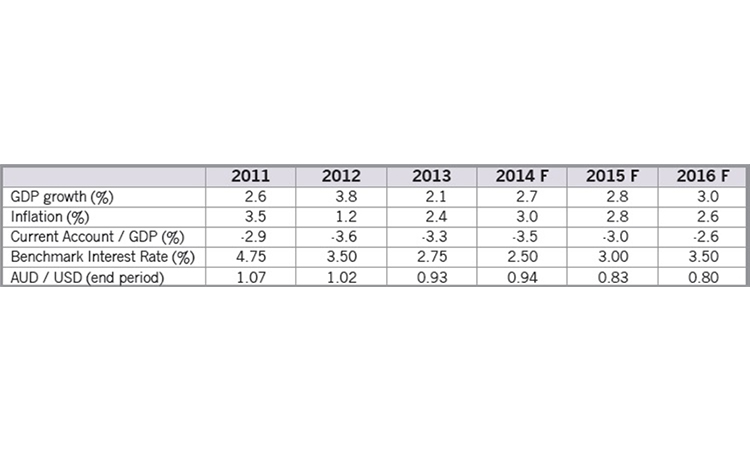

Fig 1. Australia Outlook 2015

Source: Asian Banker Research

In the residential mortgage market, competition to win over new borrowers has intensified. Lenders have been more generous with discounts, and according to industry sources, have extended better rates than advertised, aimed at broadening their borrower base. Banks are also offering other incentives, such as fee waivers and upfront cash bonuses. However, according to market reports, banks’ non-price lending standards have remained steady in recent quarters. Australian Prudential Regulation Authority data on the composition of bank housing loan approvals also suggests that the overall risk profile of new housing lending has not increased.

An important question for both macroeconomic and financial stability is whether the banking industry is conservative enough to withstand the current combination of low interest rates, strong housing price growth and higher household indebtedness as compared to previous decades. These factors may lead to a build-up in loan concentrations and correlated risks within the banking industry as suggested by lending growth variations across geographical markets and individual lenders. The Reserve Bank of Australia’s assessment of the current situation is that the risk from the current strength in the housing market is more likely impact to future household spending than lenders’ balance sheets. However, the direct risks to banks will rise if current rates of growth in investor lending and housing prices persist or increase further.

On the liability side of Australian banks’ balance sheets, global capital market conditions have improved since the financial crisis. Australian banks have increased their net bond issuance as conditions in wholesale funding markets improve. About $56.3 billion in bonds was issued in the first half of 2014, an increase of around $11.4 billion over the previous six months and approximately $8.2 billion more than their bond maturities. Banks have currently issued about 40% of their regulatory limit for covered bonds, which is only a small share of total bond issuance, leaving ample scope to increase covered bond issuance if unsecured bond market conditions deteriorate.

Improved wholesale funding market conditions have also led to some easing in deposit market competition. Banks report that there has been a decline in short-term deposits from financial institutions and large corporations. This is consistent with the upcoming Liquidity Coverage Ratio (LCR) requirement, which treats these deposits less favourably. Relative to wholesale market rates, retail deposit rates have fallen in recent quarters. Banks are likely to make adjustments on pricing and terms of their deposit products due to the commencement of LCR requirement in January 2015.

The profit growth of Australian banks in recent years can be attributed to the continued improvement in banks’ overall asset performance. Major banks’ aggregate charge for bad and doubtful debts fell by 17% in their latest half yearly results and it is expected to further decline to a historical low for financial year 2014 as a whole. Overall profit for major banks was over $11.4 billion, an increase of 13% as compared to the previous year.

In recent years, the return on equity (ROE) of major banks in Australia has been well above those recorded by large banks in other developed countries. In financial year 2014, Australian major banks’ ROE is projected to be 15%, similar to the averages recorded in the previous three years, reflecting strong asset performance. Another factor for this is their low cost-to-income ratios (CIR). Since the mid 1990s, the CIR for major banks have fallen by 20%, reaching 44% in financial year 2013. However, there is a question as to how much further major banks’ costs can be contained in the future without their risk management capabilities being affected. Looking ahead, equity analysts are predicting a moderation in major banks’ profit growth to 9% in 2015 and 5% in 2016. This is partly because bad and doubtful debt charges are low and therefore unlikely to provide the impetus for profit growth that they have in recent years. In addition, due to competition in lending markets, interest margins are likely to compress further.

.png)

.webp)