.png)

- Chinese banks well positioned themselves on this year’s The Asian Banker Strongest Banks By Balance Sheet ranking with weighted average score stood at 3.40 out of 5.0, just behind that of Hong Kong banks (3.97) and Singapore banks (3.67).

- The result is mainly driven by strong performance of provincial banks, out of top 10 ranked Chinese banks, 5 are city commercial or rural commercial banks.

- Overall, state owned and joint stock banks still dominate with higher score for most of the dimensions on the score card we use to evaluate the strength of the banks.

In this year’s The Asian Banker Strongest Banks By Balance Sheet evaluation, Chinese banks well positioned themselves on the ranking with weighted average score stood at 3.40 out of 5.0, just behind that of Hong Kong banks (3.97) and Singapore banks (3.67). China Construction Bank (CCB) remained the strongest bank in China with highest score in capital adequacy, loan loss reserve and cost to income ratio, which demonstrated the resilience of its operation while maintaining a low cost. Following CCB, Industrial and Commercial Bank of China (ICBC) and Agricultural Bank of China (ABC), with same scoring, ranked second and the third position went to Bank of China (BOC).

Out of top 10 ranked Chinese banks, 5 are city commercial or rural commercial banks, in which, Bank of Ningbo was the most improved one with its overall ranking at 23rd, up from 87th in last year’s ranking. Bank of Chengde was up from last year’s 56th to this year’s 43rd. Besides, it was the first time for Bank of Nanjing and Guangdong Huaxing Bank to become top 10 and Dongguan Rural Commercial Bank was the only rural commercial bank on the list.

Figure 1: City commercial and rural commercial banks accounted for half of the top 10 strongest banks in China

Source: TAB Research

Our ranking for Strongest Banks in China are by provinces and bank categories, including strongest state owned banks, strongest joint-stock bank, strongest city commercial bank, strongest rural commercial bank, and strongest foreign banks in China.

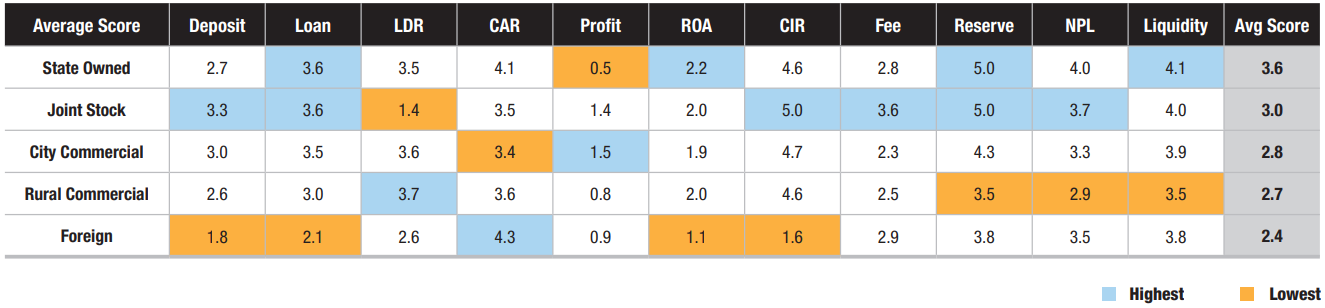

Figure 2: State owned and joint stock banks still dominate with higher score for most of the dimensions on the score card

Source: TAB Research

On average, state owned banks achieved highest strength scoring (3.6) with the highest score in return on assets, loan loss reserve, NPL and liquidity ratio although they suffered from low profitability. Joint stock banks achieved an average score of 3.0 and demonstrated strong performance in generating fee income while maintaining the low cost, they were also achieved high score in loan loss reserve which indicated prudence of business operation. Although city commercial banks achieved the highest score in profitability, their fee income score were the lowest, which implied that their business model were more asset and liability driven, this can also be told by their relatively low scoring in return on assets and liquidity ratio. Overall, we are concerned about rural commercial banks’ loan performance given they had the lowest scoring in loan loss reserve, non-performing loan and liquidity ratio among all categories of Chinese banks. Foreign banks in China has long been suffering to achieve economic scale and to acquire low cost of fund, which are reflected on the scoring with the lowest score in deposit, loan, and cost to income ratio.

Overall, state owned and joint stock banks still dominate this year’s strength ranking with higher score for most of the dimensions on the score card we use to evaluate the strength of the banks.

.png)

.webp)