- DBS, OCBC and UOB ended 2019 with solid balance sheets and financial positions but their capacity to withstand the business challenges presented by COVID-19 will be tested in 2020

- The profitability of the three Singapore banks are at risk as the loan books are projected to contract and deteriorate

- The banks have set up relief solutions to support clients’ credit health

The country’s biggest banks – namely DBS, OCBC and UOB – reported stable results for 2019. However, the building momentum in financial performance is expected to take a slight break this year as the sector is being threatened by the COVID-19 pandemic which began at the end of 2019 and have magnified globally during the first quarter of 2020. As of now, the outbreak has not shown signs of deceleration, thus putting Singaporean banks in a vulnerable state if it continues until the second half of the year.

Assets increased by around 4% to 5% year on year, with evident expansion and diversification of their loan books, mainly driven by borrowings in building and construction, housing and general commerce. Deposits also grew at a range of 3% to 6%, with UOB capturing the largest growth among the players. While the financial position of the three banks remained healthy in 2019 as evident in the sustained growth in their balance sheets, the widening COVID-19 crisis will most likely cause contraction in the loan books of banks.

Profitability will also be put under pressure. In 2019, the total income of the three banks have all shown double-digit growths, while profit before tax has shown a modest uptake with DBS outpacing the two banks. The banks were able to deliver earnings as supported by an upward trend in lending activities mostly in the corporate sectors as well as increasing fee incomes from wealth management and investment banking activities. These are reflected in the increase in their return on assets, which are at 1.08% to 1.26%, and well maintained net interest margins of 1.77% to 1.89%. Cost to income ratios were kept moderate at around 43% to 45%. However, this difficult period is expected to weigh on the income and profitability of the banks, and may add substantial costs especially as China and Hong Kong are significant sources of business for the Singapore banks.

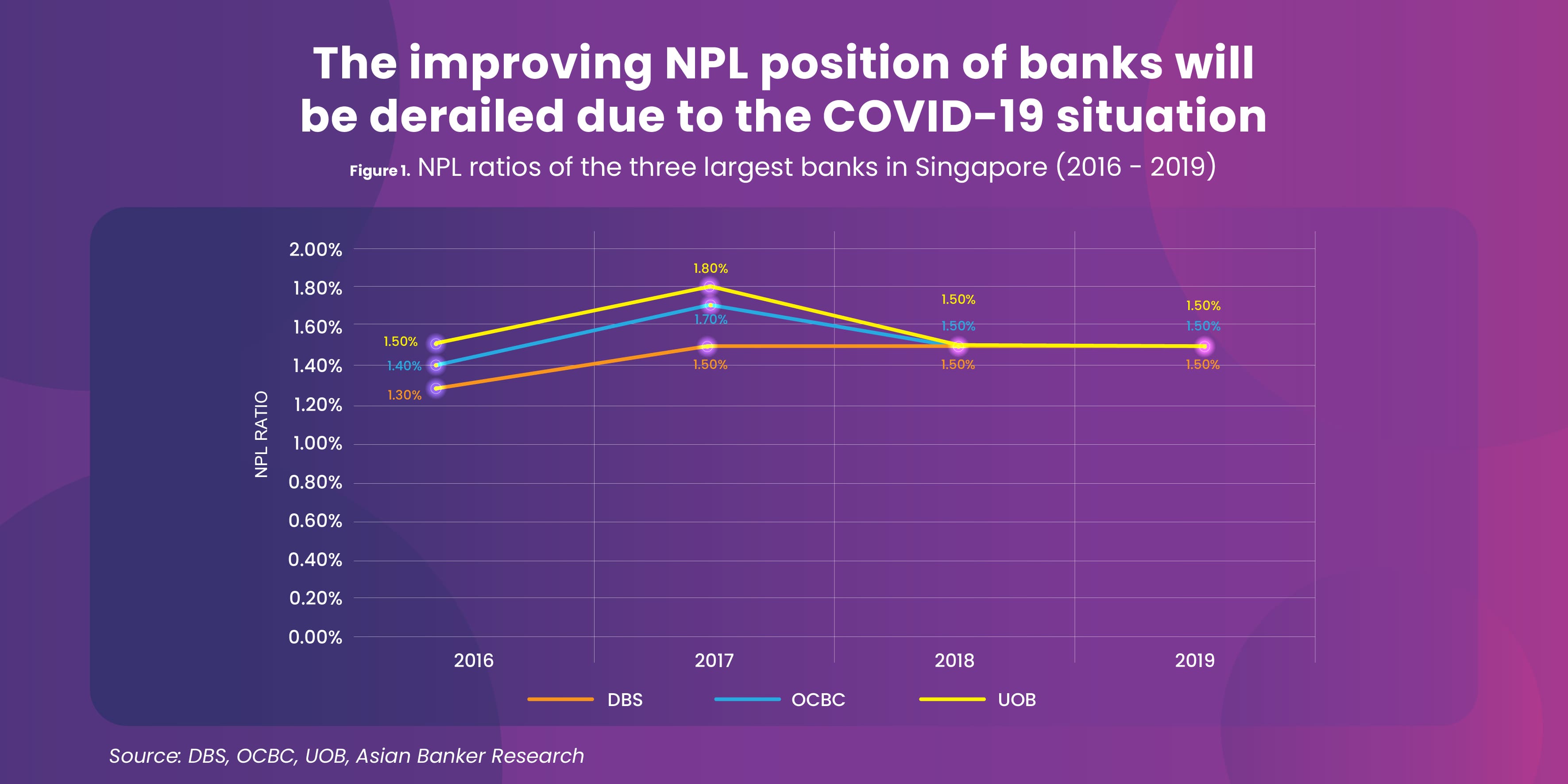

The three banks were able to mitigate asset risks and manage the health of their loan books as non-performing ratios were maintained at 1.5% in 2019 from the previous year. However, as COVID-19 directly impacts various industries as well as countries such as China, banks with significant loan exposure to these sectors and nations can lead to a deterioration in debt quality in the next months. Thus, a greater stress on asset quality is anticipated.

Nevertheless, banks have already started to put measures in place to reduce risks and help customers in these challenging situations. The banks have also announced relief and restructuring packages to assist affected customers and small and medium-sized enterprises.

The banks ended 2019 with strong capitalisation that is well above the minimum requirement. They were able achieve Common Equity Tier 1 (CET1) capital adequacy ratios of 14.1% to 14.9%, with OCBC generating the highest ratio among the three. The high capitalisation of the banks and cautionary measures currently being implemented can help cushion and lessen the negative impact of the potential shocks and further uncertainties in 2020.

.png)

.webp)