Most Asia Pacific markets experienced a slight deceleration in small and medium-sized enterprises (SMEs) loan growth in 2023, mainly due to heightened interest rates and increased caution by banks. However, the overall regional average SME loan growth slightly accelerated, driven by a surge in SME loans in Australia. China maintained robust SME loan growth, while Thailand saw a contraction. Looking ahead, anticipated interest-rate cuts in most markets, and continuous policies supporting SME lending are expected to fuel further growth.

Meanwhile, ongoing concerns persist about SME loan quality amid an unfavourable economic environment. The SME non-performing loan (NPL) ratio increased in South Korea, Indonesia, and Malaysia, while remaining high in Thailand.

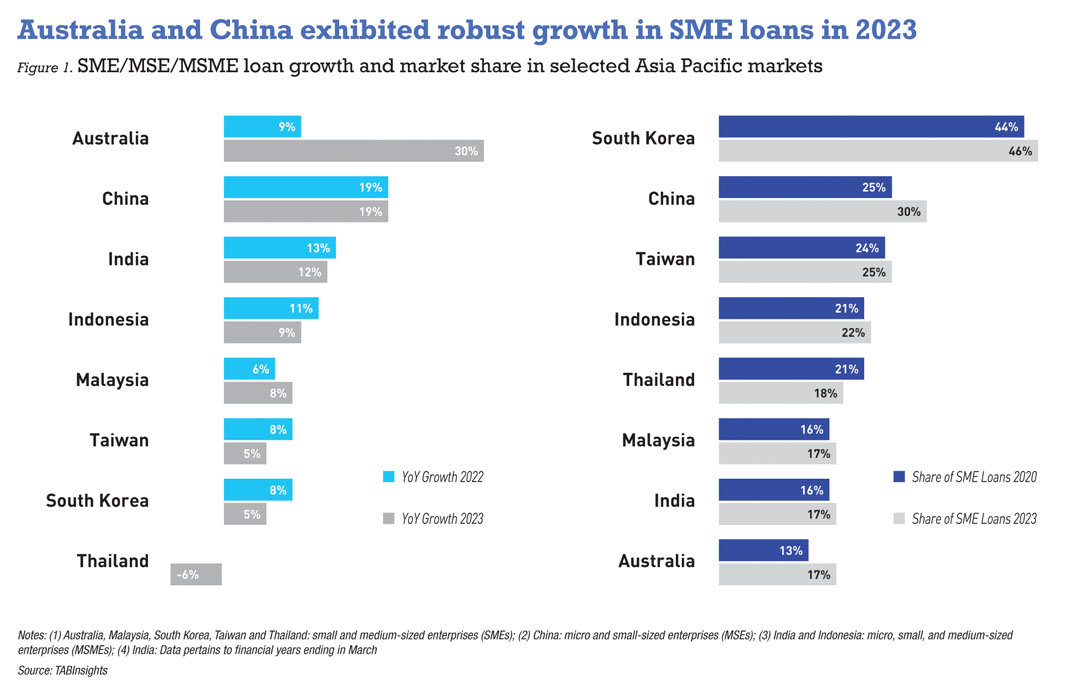

Australia and China posted strong SME, MSE loan growth

SME lending in Australia surged by 30% to reach AUD 621 billion ($423 billion) in 2023, fuelled by robust demand for financing among SMEs and active bank support. The surge helped SMEs tackle challenges from interest-rate hikes, inflation, and rising costs. Lending to medium-sized enterprises, constituting 70% of SME lending, saw a significant 36% boost, while lending to small businesses experienced 18% increase. The share of SME lending in total lending in Australia increased from 14% in 2022 to 17% in 2023, though it remains relatively low.

In 2023, China witnessed a 19% surge in micro and small enterprise (MSE) loans within the banking sector, totalling RMB 71 trillion ($10 trillion). The proportion of MSE loans relative to total bank loans increased gradually from 25% in 2020 to 30% in 2023. This growth is attributed to China’s supportive policies for MSEs, with a particular focus on inclusive MSE loans. In this category, where a single bank’s credit line to a qualified borrower does not exceed RMB 10 million ($1.6 million), there was an even more robust increase of 23% in 2023. Inclusive MSE loans constituted 41% of total MSE lending in 2023, up from 32% in 2019, highlighting China’s commitment to greater financial inclusion.

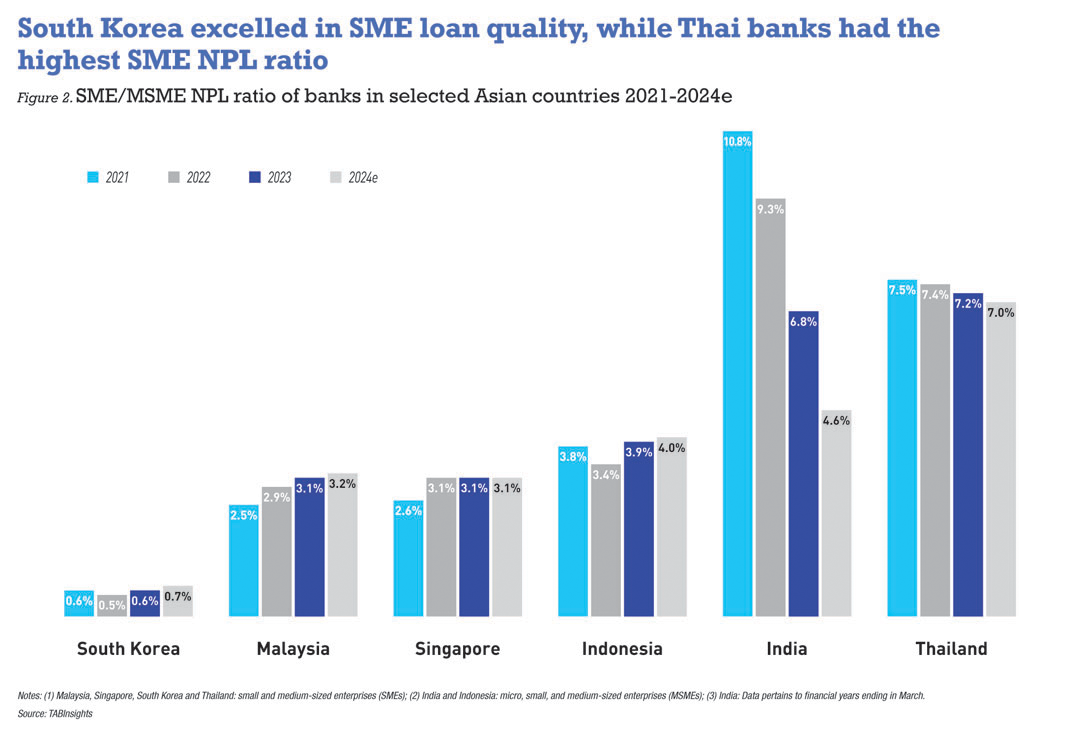

South Korea had strong SME loan quality despite rising NPLs

While South Korean banks observed a gradual deceleration in SME loan growth from 12% in 2020 to 5% in 2023, the proportion of SME loans to total bank loans in South Korea steadily rose from 44% in 2020 to 46% in 2023. This is more than double the share of SME loans in markets such as Australia, India, Indonesia, Malaysia, and Thailand.

South Korea has strong SME asset quality, but the SME NPL ratio increased slightly from 0.5% in 2022 to 0.6% in 2023, influenced by slower economic growth and higher interest rates. SMEs faced challenges with increased interest rates, raising funding costs and negatively impacting financial positions.

South Korean banks committed KRW 2 trillion ($1.5 billion) to aid small businesses, responding to regulatory pressure. Critics have argued that banks benefitted from higher interest rates, impacting vulnerable borrowers during the cost-of-living crisis amid inflation. Banks will refund 90% of interest paid in excess of 4% to eligible businesses, or up to KRW 200 million ($150,000) for one year.

SME NPL ratio stayed high in Thailand, India saw a significant improvement

The outstanding SME loans in Thailand contracted by 6% in 2023, mainly due to gradual repayments. Access to capital is crucial for SMEs facing higher costs and limited liquidity. However, many SMEs struggle to access bank loans, as the SMEs’ NPL ratio has remained high at 7%. Thai banks have been setting aside more provisions against loan losses.

Thailand has introduced a debt suspension and relief initiative for SMEs, aligning with the government’s commitment to address challenges. The Thai Credit Guarantee Corporation has endorsed two measures, including an 18-month debt suspension for SMEs affected by the COVID-19 pandemic from 1 January 2024 to 30 June 2025, and a 15% reduction in principal from 1 January to 30 June 2024.

Indian banks observed a substantial improvement in the quality of MSME loans, although the NPL ratio remains relatively high. The ratio decreased from 9.3% in March 2022 to 6.8% in March 2023 and further dropped to 4.7% in September 2023. Despite the expiration of the Emergency Credit Line Guarantee Scheme in March 2023, MSME loan growth remained robust throughout 2023, buoyed by heightened demand for MSME loans.

.png)

.webp)