The financial industry is demonstrating growth in most sectors, with the exception of real estate and construction that had begun to come out of the woods in 2022.

The opening of most countries has fueled strong growth in the food and beverage, retail, hospitality and tourism sectors; North Asian countries including mainland China, Hong Kong, Japan and Taiwan opened up towards the end of 2022.

Small and medium-sized enterprises (SMEs) have survived the last three years and seeing positive cash flow again. Still, challenges persist and depending on the sector, businesses continue to be affected by escalating raw-material prices and persistent supply chain bottlenecks. Most markets also tapered off relief programmes for SMEs in 2022 but the banking industry expects that this will not pose a concern in 2023.

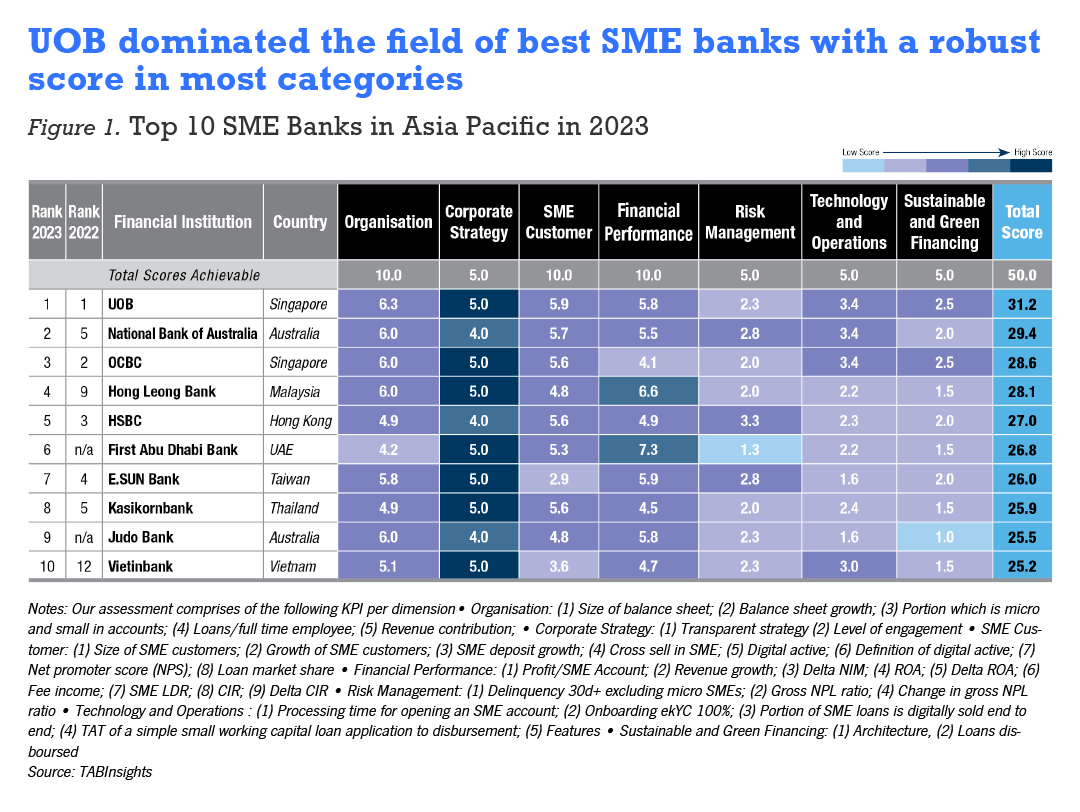

The leading top 10 players for SME banking in Asia Pacific (APAC) have demonstrated that they are flexible enough to respond to crisis events, and also understand each vertical’s key operational challenges, strategic growth and focus areas, planned local and overseas investments, and accordingly tailor business-centric solutions around them.

In 2022, UOB significantly expanded its digital business banking platform, now available in 10 markets, and introduced automated trade solutions that have increased electronic-trade applications by 48% year-on-year (YoY).

Small businesses can benefit from BizSmart, a comprehensive suite of financial and non-financial services that help to reduce costs, grow and manage operations as well as digitalise their business.

UOB has also formed more than 20 industry partnerships to provide beyond-banking solutions across seven categories, including HR, payroll, and digital marketing. Its Infinity and BizMart platforms enjoyed rapid regional adoption in 2022.

The bank delivered another year of robust and consistent financial results, outperforming its peers in net income per customer, cost management and fee income contribution.

UOB’s commitment to building regional and global connectivity with its clients, providing flexible assistance throughout the full lifecycle journey, and offering relevant digital solutions has enabled it to dominate the field once again for the Best SME Bank in APAC.

Banks here that focus on SMEs have accelerated the digitalisation and automation of their operations and processes, creating capacities and economies of scale across the entire value chain from digital onboarding to trade automations.

Digitalisation and data also enable banks to sharpen the segment play. The innovative use of transactional and non-transactional data delivers far better personalised services, engagement, and credit underwriting.

Open banking and collaboration with fintechs allow banks to open growth opportunities in previously inaccessible micro and ultra-micro segments.

Micro, small and medium-sized enterprises (MSME) have been an underserved market due to the perception that they are high-risk with low growth potential, mainly due to the lack of visibility of their actual financial footprint. While banks have made some effort to play a more meaningful role in serving MSMEs, their operating model often hampers efforts to serve those segments more economically.

At the same time, a torrent of alternative lenders and platform players have entered this market and are rapidly evolving into a one-stop portal offering cash management, financing and payments services.

While still far from becoming a threat, competition from big tech and peer-to-peer (P2P) SME lending platforms is putting pressure on banks to create more flexible ways of financing, faster underwriting and new customer-centric engagement models that can better support SMEs.

National Australia Bank has been scaling digital small-ticket SME lending of up to $250,000 for business customers since 2016 and built fully-on-cloud components. This allows businesses access to unsecured finance for term loans, overdrafts, equipment loans and broker-assisted customers.

By using a variety of natural language processing and machine learning (NLP/ML) algorithms to drive loan decisions, the turnaround time for application, decisioning and funding takes only 20 minutes. The proportion of small-business lending accounts generated with this platform exceeded approximately 45% in 2022.

SMEs increasingly expect a fully integrated product and service platform from which to access financial solutions and services to run their business, reduce operating cost, and expand regionally and beyond.

Leading players amongst the top 10 SME banks focus on creating an integrated platform for cash management, supply chain financing and payments to enable its client to cross-border connect with each other in a more efficient and secure way.

For example, UOB’s SME franchise is connecting businesses to opportunities across more than 10 markets. Supported by more than 500 offices in APAC, the bank aims to become the ONE Bank for businesses in ASEAN, where clients can talk to just one bank for all its cross-border needs.

Banks are also ramping up their sustainable finance and advisory framework to develop the knowledge and skills in lending practices to thrive in the green-financing market. While natural risk vectors amplified by climate change will have consequences on how enterprises will conduct their businesses, national de-carbonisation policies and the rise in carbon tax regimes will put pressure on larger listed companies which in turn, given their extensive supply chains, will land at the doorstep of SMEs.

To address this, leading banks such as UOB in Singapore and E.Sun Bank in Taiwan have launched simple and effective programs to help SMEs embark on their sustainability journey.

Click here to see the full Best SME Banks Ranking 2023

.png)

.webp)