- Mobile wallets are becoming the norm for day-to-day transactions as evolving consumer behaviour forces the payments industry to switch to cashless solutions

- The use of biometrics and two-factor authentication enhances the safety features of mobile wallets

- Regulatory initiatives of the mobile wallet industry will lead to greater standardisation and interoperability

With the developments in contactless payment processes and new technologies emerging daily, mobile wallets are revolutionising transactions on a global scale. Less than 30 years ago, the ubiquity of mobile phones was unimaginable, let alone the idea of transferring money using a smartphone. Today, the use of a mobile phone for money transfer is not only accepted but is becoming the new normal. The market is getting crowded but with notable leaders in respective markets, such as AliPay and WeChat Pay in China, PayTM in India, OVO, ShopeePay, LinkAja and GoPay in Indonesia, LINE Pay in Japan and Taiwan, Kakao Pay in South Korea, and GrabPay in Malaysia and Singapore.

The earliest forms of digital payment systems can be traced back to Coca-Cola in 1997, whereby the soft drink giant created a digital payment processing system where customers could pay for their soft drink from a vending machine via a text message on their cellphone. Since then, these wallets have spread to other areas, and new brands have entered the game, resulting in a highly dynamic market.

Merchants adapt to mobile wallets as they become consumers’ preference

Mobile payments have gained popularity in recent years owing to technologies and creative marketing strategies. In 2019, mobile wallets overtook credit cards to become the most widely used payment type globally. In 2020, the COVID-19 pandemic became another accelerant of the continued digitisation of the global payments landscape. The pandemic has merely been an accelerant of the digital payments revolution that has been underway for years. Mobile payments, and more specifically mobile wallets, have been the greatest driver of this revolution on a global basis.

In developed markets such as North America and Western Europe, where debit and credit card penetration significantly exceeds the rest of the world, mobile wallets have a higher rate of using payment card and contactless mobile device hardware including near-field communication (NFC) chips. Card-based wallets are using contactless NFC payments with physical payment terminals that typically also accept card payments. These card-based wallets are increasingly adding express checkout functionality to merchants, so that consumers can easily access their payment and personal details stored on their mobile phones.

Digital and stored-value wallets can be funded directly from a bank account, or by other methods, including cash, bulk disbursements, or peer-to-peer payments. Stored-value mobile wallets rely on a multitude of cash-in-cash-out methods that enable consumers to digitise and transmit cash, and convert digital cash back into bank notes when needed. Stored-value wallets largely use QR codes at the POS, as they have far greater ubiquity than NFC chips and enable merchants to accept payments with just a QR code and a mobile device. Stored-value wallets are also being used online, using QR codes and integrated checkout processes that enable consumers to complete purchases on their mobile device.

Fundamentally, merchants, especially those that are globally dispersed, need to understand that mobile payment acceptance is not about accepting one type of mobile wallet or another but ensuring that consumers in every market will have the required selection on payment types to monetise transactions.

Mobile wallet transactions have overtaken cash transactions

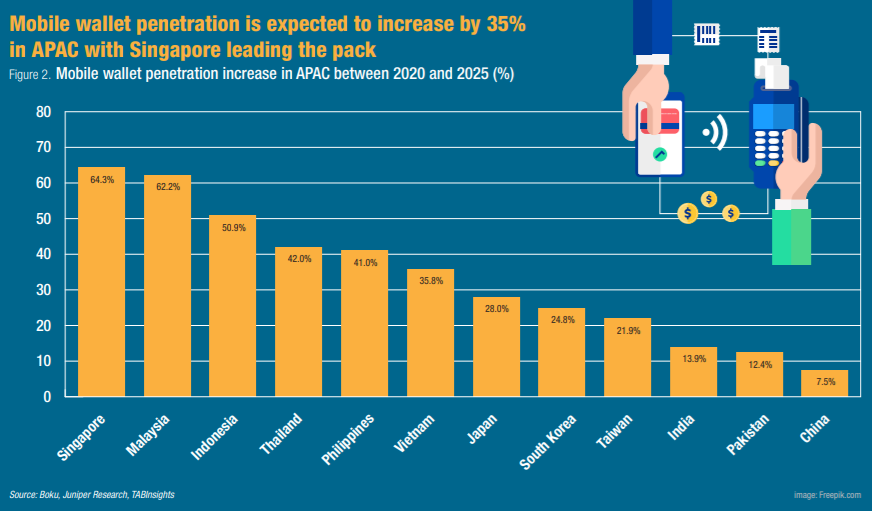

As of 2020, the population of the Asia Pacific region had surpassed 3.5 billion, which comprised around 48% of the world’s total population. Mobile wallets usage is projected to increase from 42.1% (1.8 billion users) of APAC’s total population in 2020 to 58.6% (2.6 billion users) in 2025, according to Boku. Meanwhile, the transaction volume is forecast to increase from 377 billion in 2020 to 636 billion in 2025, and transaction value is forecast to increase from $4.1 trillion in 2020 to $7 trillion in 2025.

Japan has a mobile wallet penetration of 70.6% as of 2020 and an expected mobile wallet penetration of 98.6% in 2025. The Japanese market looks set to exceed 123 million users by 2025 – a number that is unlikely to stop growing anytime soon. Powered by the Tokyo Olympics that took place in late July to early August 2021, Japan has been encouraging more cashless payments to become more tourist-friendly. This has seen the widespread deployment of contactless point-of-sale (POS) terminals and the promotion of mobile wallets within the country.

As a result of the increasing popularity of smartphones, the high unbanked rates in emerging markets, the rise of e-commerce, security, flexibility and convenience, it is no surprise that people have been increasingly turning to mobile wallets.

Wong Loke Hwee, Boku’s vice president and general manager, APAC, said, “In emerging markets, especially in Asia, credit card penetration is very low; it is less than 10% in many countries, so credit cards are not really serving consumers. Moreover, mobile wallets are already the most popular payment method in Asia.”

Across APAC, mobile wallets made up more than 40% of transactions at the POS in 2020, compared with 19.2% for cash. Furthermore, mobile wallets give consumers the ability to transact online (like credit cards), with the flexibility and ubiquity of cash.

Jon Prideaux, CEO of Boku, said, “We’ve seen a fundamental shift of consumer purchasing power from west to east, from established to emerging markets, and from credit cards to mobile payments. For merchants to capitalise on the massive potential of mobile-first consumers, they need to accept the payment methods they have and prefer, which are increasingly behind glass screens, not rectangular pieces of plastic. Now that mobile payments have overtaken credit cards globally, merchant acceptance has moved from a competitive advantage to a strategic imperative.”

In China, South Korea and Japan, mobile wallet penetration has reached majority of the population. AliPay in China has 1.2 billion users, while mobile wallet penetration in China reached 83.6% in 2020. Kakao Pay in South Korea has 15.5 million users, while mobile wallet penetration in South Korea reached 73.2%. LINE Pay in Japan reached 33.9 million users, while mobile wallet penetration in Japan reached 70.6% in 2020.

Meanwhile, in Malaysia, Singapore, Indonesia and India, mobile wallet penetration is still less than half of the population. GrabPay in Malaysia and Singapore has 4.5 million users, while mobile wallet penetration in Malaysia and Singapore reached 31.7% and 30.4% respectively. OVO in Indonesia reached 24.2 million users, while mobile wallet penetration in Indonesia reached 25.6% in 2020. Finally, PayTM in India has 55.5 million users, while mobile wallet penetration in India reached 15.7% in 2020.

According to ACI Worldwide Research, the share of adults that have a mobile wallet and have used it has reached 84% in China in 2020, 81% in Indonesia, 48% in Japan, 83% in Malaysia, 68% in the Philippines, 61% in South Korea, 71% in Singapore, 62% in Taiwan and 84% in Thailand.

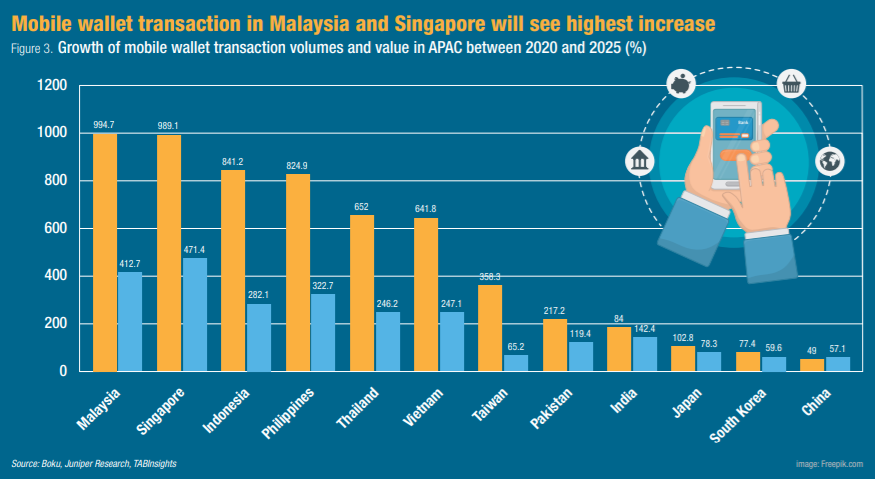

In Malaysia, three mobile wallets are battling for the more than 20 million consumers that are expected to adopt mobile payments over the next five years. GrabPay has taken the lead due to being in the market longer than competitors, as well as having a super-app functionality and greater merchant adoption. Touch ‘N Go, originally used for paying road tolls, has been gaining on GrabPay, owing in part to investment from Ant Financial. Boost, the “pure-play” Malaysian wallet has also grown rapidly and will continue to challenge other market players over the coming years.

Malaysia is a market on the verge of a mobile payments explosion, with a projected increase in mobile wallet transaction volume of 995% between 2020 and 2025, the highest in APAC. Despite its advantages, GrabPay is being challenged by Touch ‘N Go and Boost, and market share may vary in the coming years. For merchants, this market represents a significant growth opportunity, so accepting several payment types will be critical. Malaysia is a rapidly growing market for mobile payments, and it will close the gap on fellow Southeast Asian countries over the next five years.

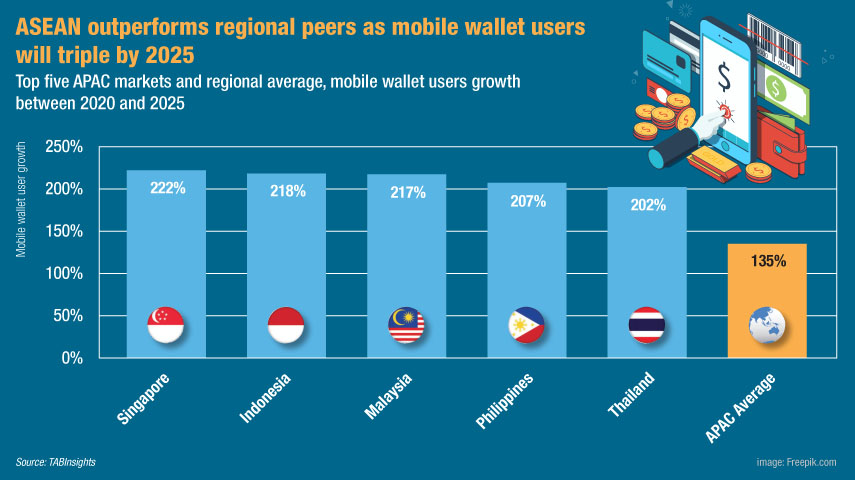

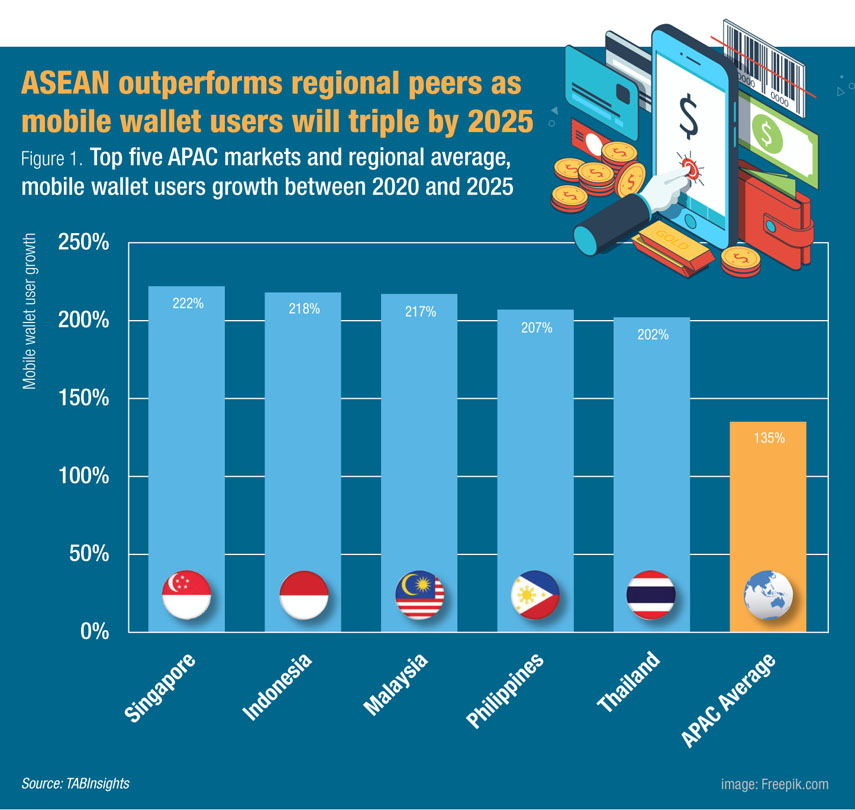

Malaysia’s growth is closely followed by Singapore, with transaction volume expected to increase 989% between 2020 and 2025. Singapore has a highly competitive mobile payments ecosystem, especially for a country with just 5.7 million residents. GrabPay, the regional super-app, which is headquartered in Singapore, has over 35% market share, and benefits from a host of financial services they provide. Favepay, known for its rewards programme and ability to seamlessly integrate existing card payments, has been gaining on GrabPay. DBS PayLah!, Singtel Dash and EZ-Link all benefit from the stickiness they have as the state-owned bank, telco and transit systems for Singapore respectively.

Singapore is a small and somewhat fragmented mobile wallet market but is still of interest to many merchants as its residents are wealthier and more international than other countries in Southeast Asia. Singapore’s mobile payments market will continue to expand owing to consumers being heavy users of e-commerce and mobile payments. Singapore is moving quickly towards a cashless future, as nearly 95% of the population are projected to be using mobile wallets by 2025.

Indonesia is a mobile payments market defined by extreme competition, with five mobile wallets battling for market share. Competition is particularly fierce due to the rapidly growing market opportunity, with infusions of foreign venture capital funding aggressive promotional campaigns. ShopeePay, a relatively new entrant to the market has become the second most widely used wallet in Indonesia because of its offers of high rebates and other promotions to consumers.

On average, consumers in Indonesia are using 3.16 mobile wallets, as they seek to maximize benefits from each one. With a young, mobile-only population, mobile wallets are heavily used for online purchases. Indonesia is one of the fastest-growing markets in the world for mobile payments, with a projected 841% growth in mobile wallet transaction volume between 2020 and 2025, but is one of the more challenging markets for merchant acceptance, due to fragmentation and rapidly changing consumer preferences. Indonesia is another country rapidly making the transition from cash-centricity to digital payments.

Mobile wallet’s ease of access encourages higher spend

Businesses that launch mobile wallets today are seeing the benefits of customers who spend more when they can easily access their payment methods and quickly complete the payment process. The US, which recorded the most smartphones purchased in the first quarter of 2021, saw an average of 7% more spending at outlets that allow contactless payment.

Furthermore, customers using mobile wallets tend to be loyal customers. The speed and convenience of mobile payments encourages people to reuse the same payment method. Loyalty is also boosted when customers are able to easily share details of their payment method with peers. For example, Starbucks has partnered with Facebook Messenger to allow customers to easily send a stored-value barcode bought at Starbucks or selected from the company’s loyalty programme through the app, to be used by other users.

Businesses will also benefit from the growing number of people using mobile wallets as their primary payment option. In countries such as Nigeria, where approximately 23% of people use mobile wallets as their primary payment method, many consumers are willing to pay a higher price for a more convenient payment method. As a result, companies that set up mobile wallets stand to benefit from the loyalty and convenience that comes along with this type of purchasing behaviour.

Moreover, mobile wallets are protected by biometric authentication such as fingerprint scanning, iris recognition, facial recognition and two-factor authentication that ensure transactions are coming from the authorised person. There are no account numbers, thus reducing the risk of remote hacking (spyware/malware).

Regulators protect consumers while promoting innovation

Mobile wallets are becoming more popular in emerging markets with digital opportunities and a large unbanked population, because traditional banks do not meet their needs. Governments and central banks are working together to regulate mobile wallets to protect consumers while promoting innovation. The Philippines, for example, is pushing for increased security through know-your-customer regulations and other means. Meanwhile, Singapore regulators want to support innovation by encouraging digital wallet providers that offer greater value than less-established players.

Mobile wallets are replacing the traditional bank accounts

Emerging markets witness the highest unbanked population. As of 2020, the unbanked population reached 24% in Latin America, 17% in Central and Eastern Europe, 27% in the Indian subcontinent and 39% in the Middle East and Africa, according to Boku. While the unbanked rates in these regions remain high, smartphone penetration now outpaces bank accounts, enabling more consumers to access sophisticated digital financial services.

The Malaysian government announced a plan to boost the mobile wallet sector that involves investing MYR 40 million ($9.6 million) to incorporate three mobile wallet companies. Meanwhile, China is more concerned about regulating this system to ensure online safety of consumers.

Mobile wallets are also being promoted by central banks in Europe. The Swiss National Bank is creating a “unified payments area” that includes the entire scope of mobile money activity. EMVCo has published a set of standard rules for QR code payments, which has been adopted by several countries. The standards facilitate the worldwide interoperability and acceptance of secure payment transactions. As of March 2020, following the mandate from State Bank of Pakistan, all QR payment providers must adopt the EMVCo QR payment standards. In February 2020, Hightech Payment Systems rolled out a QR-based National Payment System in Saudi Arabia in partnership with Saudi Central Bank.

Wong said, “Governments and central banks have a role to play in standardisation and interoperability and helping the ecosystem continue to thrive. Central banks are leading the initiatives to standardise mobile payment QR codes used at the POS such as PayNow in Singapore, QRIS in Indonesia, as well as rolling out real-time payment schemes such as PromptPay in Thailand.”

Developing customer trust and building partnerships in a competitive market

Developing payment platforms with enhanced security should be at the forefront for businesses to build trust and confidence with customers. According to eMarketer, fraud rates are rising, creating a sense of unease among consumers who are not sure if they can trust their payment method provider. Extra security measure such as fingerprint recognition ensures that customers are secure while making payments in stores.

Businesses and merchants have been partnering with mobile payment systems and networks to increase their customer base while accepting mobile payments, hence facilitating the payment journey. Mobile payment networks can eliminate the barriers of entry set by merchants for mobile payment, leveraging on the lower cost and leaner integration model.

Fourteen mobile payment systems including BAMCARD, Bankart, Blik, Borica, iDeal, SIBS and SWISH joined the European Mobile Payment Systems Association, uniting more than 70 million mobile payment users, more than one million merchant acceptance points, and hundreds of European banks, handling several billion transactions per year. Mobile payment platforms such as AliPay, WeChat Pay, GOPAY, GrabPay, Paytm, and LINE Pay have joined M1ST’s mobile payment network. The mobile payment network allows standardisation in payments, maximising merchant acceptance, accepting regulated payments and eliminating the difficulty of mobile payment acceptance so that merchants can accept mobile payments quicker.

Businesses that launch mobile wallets can communicate with their customers in innovative ways given the interconnected ecosystem. By connecting the mobile wallet to social media platforms such as Facebook, businesses can send coupons or updates directly to customer’s smartphones. This can encourage customers to use the same payment method repeatedly.

Leslie Choo, managing director, Asia, ACI Worldwide, said, “This vision for a region-wide, seamless and interoperable payments ecosystem is within reach, and leading countries in the region are becoming more unified on their technology strategies and the expert vendor partners that can deliver it.”

Regulatory development and partnerships will drive mobile wallet growth

APAC is a rapidly growing e-commerce market, with an emerging middle class. It is very attractive for merchants. At the same time, the market has significant wallet fragmentation, with different regulations and laws for different countries. While merchants can achieve standardisation and back-office optimisation with a mobile payment network partner, the mobile wallet industry still needs development in terms of regulatory compliance by governments and central banks alike to ensure safety, transparency, operational efficiency, quality and customer trust.

.png)

.webp)