Datafiles

Jun 20

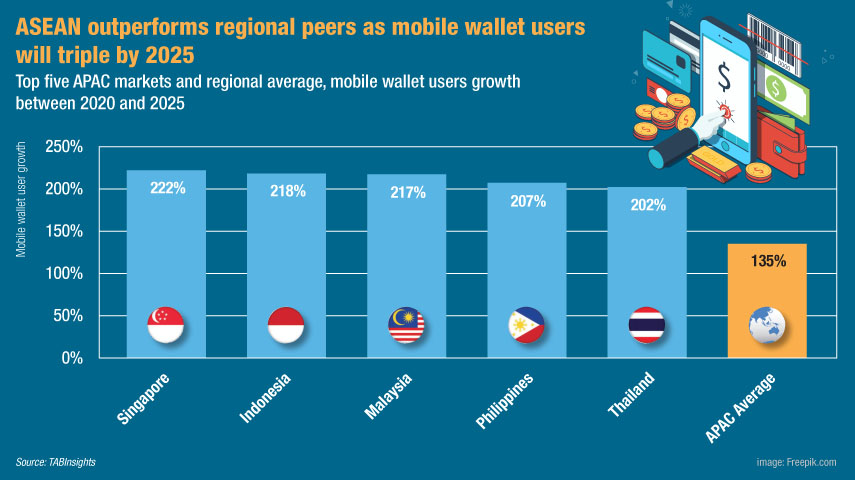

Technological disruption is reshaping the payment landscape, creating a tight mobile wallet business environment. Banks must reshape their strategies that will help enhance their competitiveness in this market.

.jpg)