Datafiles

Jun 16

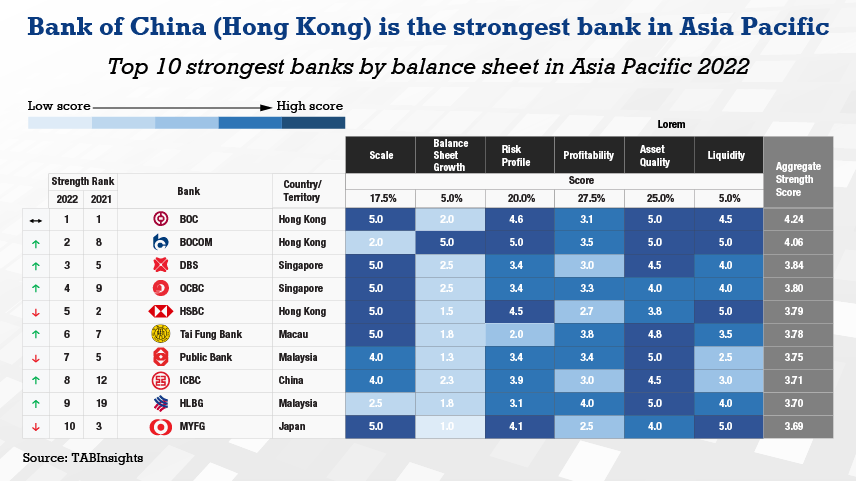

The COVID-19 pandemic has exerted substantial impact on the profitability of banks in Asia Pacific, although most are better positioned to weather this crisis than during the global financial crisis